Just out of the topic that is being discussed, listened to Prof. Aswath Damodran video on Numbers and Narratives, it was indeed a very fascinating session and was totally Intriguing, brings out a different perspective on how investing should be approached and seen, thanks for the link.

1 Like

- Change in PP&E and other Fixed Assets is CapEx

- Yes

- You can find it in the Balance Sheet as Cash or Bank. You may want to consider liquid investments such as Mutual Funds as well.

1 Like

Can anyone throw some light on how to use stoploss and averaging in fundamental investing

-

No serious investor uses a Stop-loss, as far as I know. At least not in the traditional sense. They make sell decisions based on availability of better opportunities or risk of a huge capital loss. Both of these are linked to a company’s fundamentals and the story they think will play out from those fundamentals.

-

Same thing applies here. You average if you think the company’s fundamentals and story demand a value higher than the price.

1 Like

If you go through this thread from this point onwards, it might help:

1 Like

Hello all my friends.many great investors talk about investment with best quality managements.what are few characterisics of a best quality management?it will be very helpful

I personally use Jack Welch’s 4E model (A modified version of the original 4E):

Some ways to identify these qualities could be:

- Energy/Passion: Listen to interviews by the management. Do they seem passionate about what they do? Are they excited when the discuss plans about the company?

- Energize: Look at employment websites like GlassDoor or Indeed. You can easily understand how the management treats its employees.

- Edge: Very difficult to identify unless you are an insider or an insider. This relates the speed at which managerial decisions are taken. If there are news articles online or if you could get something from the company’s AR, that would be great.

- Execution: Listen to company con calls and read the MD&A of the AR. How does the management respond to problems? Are the motivated to tackle it or do they sort of ignore it until it goes away? Do they provide generic statements as solutions? Execution is the hallmark of a great management.

Some additional things that can be looked at to confirm the quality of the management:

- Higher dividend payouts when there are no capex/acquisition plans in the immediate future (Subjective – Microsoft, Google or Berkshire Hathaway may be some counter examples)

- All the returns ratios (RoE, RoCE, RoA) substantially higher than the industry average

- Independence of the Board (Family members/friends of the CEO part of the board, unqualified members part of the board could be some red flags)

- The presence of a brand or a higher number of patents

- “Skin in the game” or the manager’s own stake in the company and whether it is increasing or decreasing

- Measures taken to counteract difficult scenarios in the industry or the company in specific (For ex: The management of Goodyear India specifically state that they’re more concerned about maintaining Margins, rather than promote Sales and it shows. When Rubber prices fluctuate, Goodyear’s Margins still remain within a closed boundary)

That’s almost everything I consider regularly. Of course, an easier addition to this could be to just read loads and loads of articles and watch videos involving the management team. Once when I held a stake in MCX, I even went as far as to add the CEO in LinkedIn. Since management quality has a lot of human element involved, try to read a lot of books on leadership and management in general.

I hope this helped.

8 Likes

Thank you very much sir

Hii everyone…

Is there any site where we can find the concall transcript of the companies…Many companies do not provide it on their website.

Hi Sumit

Concall details can be found on researchbytes website. https://www.researchbytes.com/

Regards

Uday

1 Like

Stock Adda is a recently created YouTube channel which also uploads Concalls: https://www.youtube.com/channel/UCptHdLy6B3hOngFxBCysAqA

But I’m not sure about the extent of their uploading, whether they cover all the con calls etc

5 Likes

Hello Members,

I have a question: How does one know the timings and web addresses of companies conference calls during the results season and otherwise ?

For most retail investors, this information is available from BSE as part of company announcements.

Assets are split into two: Fixed Assets and Working Capital. The comprehensive term for both of these is “Capital Employed”.

- So really, the RoCE should be a good metric to judge how much the company generates out if its Assets. However, some Earnings should ideally be capitalised to understand the real picture. For instance, IT companies have a humongous RoCE. But you’ll need to realise that their actual Assets are their employees. So you will need to capitalise Employee Expenditure into Assets, which will bring down their RoCE to comparable levels. Same with R&D expenditure and Pharma companies, for instance. My valuation model includes a tool to do that (But the judgement of what expense to capitalise is entirely yours)

-

You can look at the Working Capital / Sales Ratio to identify companies that lack pricing power. A good WCap/Sales is below 0.20-0.25. The Ratio basically says “20% of the company’s Sales and the resultant Profits may or may not actually materialize”. The best companies have a negative Working Capital.

-

You can also look at Profit Growth / Sales Growth Ratio (Preferably long term averages). I’ve never seen this Ratio mentioned in any textbook or anywhere else, but I use it as a custom Ratio in Screener and it helps. If the company does not have too much debt, a >1-1.5 PGSG Ratio will indicate that the company has a lot of Fixed Assets. While this is fine, it would hurt Companies that are prone to recessionary cycles. During a recession, it is draining to have fixed costs, but lesser profits to pay for them. Variable costs can be avoided during a recession. A high PGSG is good for companies that sell the most basic product in the industry.

-

You can directly look at a company’s Financials to understand what their Assets are actually and how much they are dependent on it. The Sales / Capital Employed Ratio can be considered as a velocity check for Assets. You can compare it with other companies in the same industry to see who makes better use of their Assets. A higher number is better, of course (Usually ranges between 0.5-4). This is probably the answer you’re looking for. But look at it in conjunction with #2 to understand the full picture. If you want to compare outside the industry, include #1 as well.

7 Likes

Thanks a lot for the information Abhishek.

For point 3 is the case right with ratio < or >.I think it should be <.plz clarify if I am wrong

In the absence of too much debt, a high PGSG Ratio indicates a higher Fixed Assets / Total Assets Ratio. You can also directly find out this figure from the company’s Balance Sheet. High Fixed Cost in other words is called Operating Leverage.

Essentially, a high Operating Leverage says that a company has already paid a lot of money for its Assets. It needs to keep making incremental profits or else it would risk making losses compared to what the Assets cost when they were purchased (So, in Present Value terms). As a trade off, if it’s a good Asset, it will stand for a long, long time and generate cash flows for the company.

The trouble arises when the company’s business is not recession proof. Think luxury consumables or durables. During a recession, customers will cut down on luxury expenses. However, the company still needs to make back profits to cover the cost of its Fixed Assets (In PV terms). When it doesn’t, it means that the company invested too much (Imagine a company doing capacity expansion, only to figure out there’s no demand).

So there are two points to note here. One: if the company’s product is not recession proof, it’s better to have a lot of Variable Cost. Fixed Cost is a drain during the down cycle.

Two: in an inflationary world (Like in India), it’s better to have Fixed Costs. Because what a company is essentially doing is paying up front when the cost is lower and getting to charge customers a higher profit, as inflation rises. In a deflationary world (Like in Japan or the UK), it’s better to have Variable Costs. When talking about a particular industry, the price of their major raw material can be considered like this specifically (Whether its prices are inflationary or deflationary).

Of course, too much of anything is bad. So too much of Fixed or Variable cost is bad. There needs to be some kind of balance. Depending on where the company stands with the above checks, there should be a tilt towards increased Fixed or Variable cost.

I personally prefer investing in companies that solve a very basic need. I avoid cyclicals and seasonals altogether. When I say ‘a basic need’, I’m talking about it from the POV of the customer. Even Eicher Motors can fall into this category, since for their customers, a Royal Enfield is not a “luxury”, but a necessity to satisfy their aesthetic needs. So this way, I can safely look for companies with a high PGSG Ratio, because these companies have spent up front and continue charging higher profits as inflation increases, without the fear of their customers restricting their buying of the company’s products.

The PGSG is a very small part of large puzzle. I wouldn’t give too much weight to it, but I’ve also never invested in a company with less than 1 PGSG (Again, long term averages).

1 Like

Hi, i have two questions

-

How we can calculate working capital accurately. In General, we calculate it by simple Current Assets - Current Liability but how we can interpret ‘cash and cash equivalent’ while calculating accurate working capital? what does mean by ‘excess cash’?

-

While summing up ‘Net Fixed asset’ or ‘Net fixed Tangible assets’ do we really need to add ‘Capital Work in Progress’ (CWIP) to get the accurate number of Net Fixed assets?

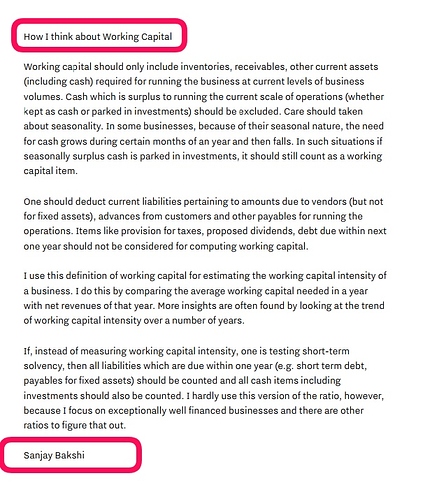

i have attached Prof Sanjay Bakshi write up. but not understand the exact meaning !

The simplest definition of Working Capital is:

Non-cash Current Assets (-) Non-debt Current Liabilities.

Prof. Sanjay Bakshi’s version simply expands on the definition of ‘Cash’ and ‘Debt’:

(Current Assets - Cash - Liquid Investments) - (Current Liabilities - Provision for Taxes - Proposed Dividends - Short Term Debt)

He further adds that he looks at the WCap / Sales Ratio to determine the Working Capital demands of the business. In general, a good WCap/Sales Ratio is below 0.20-0.25. A decreasing trend is a positive and a negative Working Capital is the most ideal scenario.

I hope this is clear.

4 Likes

The fundamental logic to identify the working capital is to understand how much funds is locked for operating the day to day business.

So exclude all items which is not involved in day to day operations like excess cash, provisions - which are just accounting entries, trade creditors for capex ( not a item for day to day operations), prepaid, etc…should be excluded to exactly understand what is the intensity of actual funds getting locked in working capital.

I will also see what is the yoy working capital ratio to sales. Over a period of time this has to reduce, if sales is increasing and this ratio also increasing, it’s a sign of unhealthy financials. Growth is happening but company doesn’t have any bargaining power or outdated Inventory in books.

One more thing I will also see is how much percentage of short term debt as part of Receivables plus inventory minus trade payables. This is more important for me. Over a period of time, the business should have enough cash to manage its WC and not keep taking loans for day to day operations.

2 Likes