This stock has corrected from 225 levels to current levels of 30-32. Investors need to be careful where this kind of price decimation takes place. If not anything else, stocks which fall 85% do not usually go back up. Caveat emptor applies.

7 Likes

While the price erosion is obviously a concern, but that cannot be a reason for stock not to regain previous high. Many front line product companies (Apple, Microsoft, Oracle) have corrected 70-80% in their life time and then regained new highs, having said that I am not comparing their business with Intense.  , what I am trying to mean many micro/macro economic factors impact price.

, what I am trying to mean many micro/macro economic factors impact price.

Even ‘Intense’ corrected from 100 to 10 in past, before it moved above 200 again. But question is whether the fundamental of this company completely broken or numbers are crooked? Don’t think so. It has a excellent product, company definitely was going through tough time for past couple of years, but now seems things are getting sorted out. As Shrihari mentioned that company has maintained revenues of 55 odd crores for 3 years, and lot of it is AMC driven so brings in some certainty to revenues, so downside should be limited. Also company looking to reduce dependency on Telecom, signed up BSFI clients. If they get traction in other regions like north America, that should be super positive. As MSSMurthy mentioned they have given guidance of 65-75 cr rev and 25 cr ebidta, if that could be met I think stock price will be much higher than what it is now.

2 Likes

It is not just business. It is credibility with growth. Even of bz picks up which is hope for last so many years market will not hibe ot credit. Virinchi is a good example doing good for ever and languishing…some time you have to say good bye. There are better fishes to try.

3 Likes

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=f04864b1-2ad1-4f9b-a713-ac7cfbb7e88a

Clarification sought by exchange. Let us wait for reply

Is anyone attended AGM ? Any updates about AGM ?

It has been a while since I or anyone else has posted here. Sometime at the end of July 2019-early August, I sold my Intense stock holdings at an average price of approx. 25-26. I sent a private message to @zoro99, @james_kerala, @vkshetty9, @JackSparrow13 and @Salim_Khan back then, stating the same. (these were individuals who either liked all my messages or reached out to me over pm to get suggestions on what needs to be done with this stock)

After I sold my stock, the price went up to 37, (I was told that I missed out on the rally despite all my hard-work/analysis) however, has now made a new 52 week low. I want to post some of my thoughts on why I sold, for the sake of completion of numerous pages of analyses that I posted here (My intent is not to bias your buy-hold decisions):

If we consider all stocks in our stock market and give them a ‘quality score’, lets say between 0-100, then a stock like Infosys might score a 100 while a stock like Satyam will score a 0. All other stocks will be scored between 0-100, some closer to INFY, while some may be close to Satyam and some in between.

After a lot of analyses on Intense stock, I decided to give it a score of 30. This is when I posted this analysis.

While this stock has had fraudulent activities multiple times (a pump and dump is nothing but a fraud) as presented in my analysis starting here, my rationale was that some weight had to be given to factors like a) good product as seen by Gartner recognition and b) numerous clients with a good reputation c) Promoters insistence of a ‘fantastic’ pipeline of deals, 200 crore revenue pipeline with 40% conversion rate etc. d) Stock price valuation versus revenues/profits.

Further, given that we have no stringent rules/implementation of rules to check pump and dump/fraudulent operations/stock manipulation in our stock market, I expected the stock price to go up once re accumulation was done. In numerous stocks, we have seen draw-downs to shake off ‘weak hands’, and then the stock price goes up. This is what I assumed will happen to Intense tech stock, given all the above factors.

However, based on new data, I had to reconsider my assessment: a) On being asked about the 200 crore pipeline with 40% conversion rate, the promoter forgot about it and insisted that he never made the commitment (read the last conf. call transcript) b) On being asked why timely and accurate information was not given to investors thereby misleading them, the promoter started fumbling (you can listen to the conf. call as the transcript does not capture these details (?) c) Only one review was considered by Gartner to rank the product; this seems strange. However, the product is ranked last amongst all considered. d) The price could not hold above 30 (a technical multiyear support) twice during Jun-Aug 2019.

Hence my decision to sell. I re-evaluated my score on Intense stock and it is closer to 0 now. It has ‘manipulation’ written all over it (repeated pump and dump activities) and I cannot find anything good about it. It is obvious to me who the fraudsters are (who defrauded whom) but may not be the case for many investors. I will also give a score of 0 to stocks like Sankhya Infotech, Cosyn, Lycos etc. ( Cosyn’s pump and dump is very similar to that of Intense tech; plot both the charts and convince yourself)

Can the stock price go up? I think, yes, but only through manipulation(operators buying and selling amongst themselves along with ‘planted’ news). But that is no reason to hold the stock. Why will any retail investor or a fund ever buy this stock? If no one will buy the stock, why will it go up?

12 Likes

From their press release today

The company was able to show strong increment in profitability YoY on the back of operationalization of agreements in subsidiaries in North America and Europe. Given the traction in service delivery these trends are expected to sustain.

1 Like

Hi Shri Hari

What’s your opinion about the Q4 result?

Manipulated?

Again Pump and Dump?

1 Like

Why would serious investors investing their own hard earned money even consider spending time on tracking companies whose cash flows are consistently negative is beyond me… there are much better quality companies available where one would not lose one’s capital to research and spend time on.

7 Likes

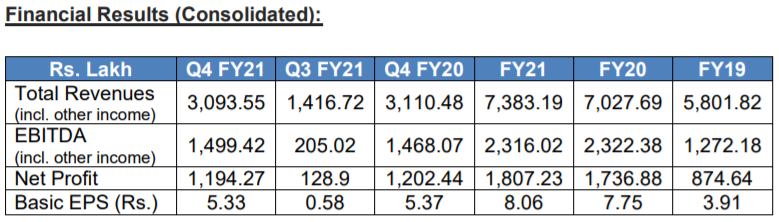

Results are out. Seems good. Consolidated Yoy revenue up by 19.5% and pat up by 35%.

I don’t hold intense tech anymore. But seems like promoters have bought some finally.

Q-o-Q

| Financials | Q4 FY20-21 | Q3 FY20-21 | % Change |

|---|---|---|---|

| Total Income | ₹ 30.93 crs | ₹ 14.16 crs | Up 118.43% |

| Net Profit | ₹ 11.94 crs | ₹ 1.28 crs | Up 832.81% |

| EPS | ₹ 5.32 | ₹ 0.57 | Up 833.33% |

**

• Revenue CAGR at 13% (FY19-FY21)

• EBITDA CAGR at 35% (FY19-FY21)

• PAT CAGR at 44% (FY19-FY21)

• FY21 cons EBIDTA margin 31%, PAT margin 24.5%

• Dividend for 3rd successive year (20%)

Performance Overview from the company (in press release) – New business wins, growing partnerships and improved wallet share amongst existing enterprise customers have translated to consistency in revenues and profitability streams. The Company’s range of offerings including, Digital Business solutions UniServe NXT Digital Onboarding, Digital Engagement, UniServe NXT Digital B2B CX is driving deeper momentum within enterprises. Concurrently there is continuous engagement to enhance citizen services to ensure predictable services revenue.

Robust performance during the fiscal was underlined by improved engagement with system integrators cross-border. With attractive implementations in advanced markets, the pricing model is auto-scaling while retaining higher share of annuity upsides. The company was able to show strong increment in profitability YoY on the back of growing engagement with SIs, involvement in digital citizen services projects and continued customer engagement. Given the rapid application development and service delivery capabilities of UniServe NXT, these trends are expected to rise.

**

Annuity engagements

• Deeper engagement within portfolio customers in telecom, banking and insurance domains for digital transformation of customer-centric business processes

• Long-term managed services contract on track and yielding good returns

• Densification of up-sell/cross-sell opportunities as digitization of customer experience became all-pervasive during the pandemic

• Enriched partnerships with system integrators enabling greater penetration in global markets

Growth engagements

• Mission-critical citizen services for large democracy gaining critical momentum

• New deals in insurance and banking sectors underline market share gains

• Marked foray into utilities vertical through strategic alliance with large private entity

Corporate highlights

• UniServe™ NXT recognized for being a low-code development platform, speeding up design and delivery of business automation

• Intense Technologies secures 4th consecutive ‘Leader’ status in the 2021 Aspire Leaderboard Business Automation grid

• Positioned as a ‘Focused’ vendor in the Overall Leaders for CCM, Communication Composition and Omni-channel orchestration grids in 2021 at a higher ranking compared to 2020

• Recognized as “The Most Admired Companies of the Year 2021” in a special edition feature by The Enterprise World

• Listed in the Gartner Market Guide, 2019 as one of Representative Vendors of the Customer Communications Management

Aspire Assessment of Intense Technologies:

What we like:

- UniServe™ NXT is a low-code/no-code development platform that speeds up the design and delivery of business automation and customer communications solution

- UniServe data virtualization capabilities is a real differentiator, and offers customers more choice in how they ingest and normalize data

- Successfully expanding into campaign management and interactive personalized videos

- Proven expertise in the telco market, particularly in South Asia, but also expanding geographically (especially into Europe) as well as to other vertical industries

- Extensive partnership network with leading system integrators and print business outsourcers

Be aware of:

- While Intense Technologies continues to do very well in Southern Asia and is seeing good traction in Europe, its presence in North America is still emerging

Opinion

UniServe™ NXT offers a comprehensive system comprising a wide range of CCM, BPM, and CXM capabilities. This is underpinned by strong data capabilities and increasingly the use of emerging technologies such as artificial intelligence and machine learning (AI/ML), which aim to reduce friction between business users, IT, and customers. The company’s focus on low-code development, DevOps, and business agility are in line with enterprise demand. While much of that vision has, so far, been realized in its BPM offerings, Intense has an opportunity to expand its offerings into the domain of CCM and, increasingly, CXM. With a large customer base in Asia, a strong partner network, and a growing base in Europe and the United States, the company is setting itself up for further expansion.

**

Aspire Founder & CEO - Kasper Roos Video, along with complete review is on 'Aspire Leaderboard’s website below -

https://www.aspireleaderboard.com/review-of-intense-technologies

**

**

**

As per the current shareholding pattern (Quarter ending: June 2021) - a New Foreign Portfolio Institution taken position in Intense Tech.

McKinley Capital is one of the three business units of McKinley Management, LLC which is a privately held, Alaska, USA-based firm providing world-class investment, research, consulting and advisory services from its offices in Anchorage, Juneau and Chicago.

McKinley Capital funded investment strategy focused on the Middle East, Africa and South Asia region fund is called as “MEASA”.

Wow, This company has a long history.

- I was wandering why this is trading at 11 PE. Reading through this thread gave me the reason.

- Promotors have increased their stake.

- Introduced Project Butterfly where they want to increase their revenue vertically.

- Given their past history, will be watching if they can walk the talk before making any investment.

Thanks to VP for this detailed info on this company.

4 Likes

What do they do??

Intense Technologies provides Customer Communications Management (CCM), Business Process Management (BPM), and Digital Experience Management (DCX)

Top use cases of CCM include driving self-help strategy to promote a company’s mobile application downloads, working with contact center analytics to reduce incoming volumes, driving brand loyalty for an enhanced customer experience, ad-space monetization for cross-selling & brand partner marketing, hyper-personalization for better customer engagement & improve overall customer experience and capturing customer interest & CTR for enhanced lead generation ensuring higher campaign success

Fortune 500s use thier Digital end-to-end CCM solution platform, UniServe NXT which is an award winning platform. It takes care of digital customer onboarding, the customer analytics aspect and the customer billing and metering accuracy.

Then they have the digital communication like your EBBP, your e-bills all of that and the B2B analytics at a high level. We are in the four quadrants of Acquire, Analyze, Engage and Experience; this is the customer life cycle.

Our list of marquee customers includes top five private banks, top five insurance service providers, and the two top telecom service providers (TSPs) of India with over 50% market share in the insurance and telecom sectors in India

What is interesting here?

So they do licensing and then provide AMC as well. Right now 60% to 65% of their business is AMC. AMC business is like a perpetuity business which grows at 15% to 20% every year and the rest of the business is lumpy licensing, where every year they have to find new customers and sell licence

So they should be at least growing by 9% to 12%

This is from one of NEWGEN very old concall

As per Gartner and Forrester peer insight Intense technologies has the best product , better than Adobe, Oracle, Newgen etc check it out on the link below

https://www.gartner.com/reviews/market/customer-communications-management-software

There are various market intillegence report which say the same like spark matrix, aspire leaderboard etc etc

The point is despite newgen having an R&D team of 300+ people and intense entire team size being around 500 they have a better product in the same category + intense has clients from fortune 500 so, at least we know the product is great.

From an old con call of newgen just to understand their CCM %

So What is the problem with intense??

The above cut out is from one of these market intillegence report and you would see many times in the con call as well the promoter says we are weak in sales and marketing. Also I have noticed in various market intillegence quadrants that they are horizontally ahead which shows product capability but vertical they are always behind newgen which shows execution capability.

Why has it been like this and what is different now??

My understanding of a product company is you have a fixed cost, in their case it is 50-55cr (it would be more now this is old data) so as a company you need to have a particular sales to have some flexibility to experiment new things, which they did not have + they had a very bad time because of a BSNL order in past.

Now they being at 2x their cost I think the company is having enough room to take those risk to get new sales.

Are they taking the risk/experimenting then??

One of the reasons for the increase in cost is that they purchase hardware and give it to clients so it is like trading but you can see a 30% growth in employee exp. In a product company you don’t have to grow so much on the employee front.

This is from EPFO, as on august 2023 their strength is 570

My understanding is that this is a 30% margin business, I mean there is no significant expense in 60% of their maintenance business but you can see this year their cost have significantly increased. IT infra up 3x, they are at 20% margin now and these are the cost which would get them sales.

The started PROJECT BUTTERFLY in december 2022 which is like an internal thing

Their sales growth and margins for last 3 qtrs

Recently they have opened a new office

https://twitter.com/in10stech/status/1776262640203084252

Back in 2016 and 2017 they had like 2 sales guys now I am just going to quote them from one of the con call

“”In business development, we have added about 12 resources. In sales, we have added about five new sales. “” Q4FY23

“”In fact, as a matter of fact, even this quarter we added four additional sales personnel with pointed focus around being able to cross-sell, up-sell these new revenue streams that we’ve added. Q2FY24””

The CFO is also a new addition just added about a year back

https://www.linkedin.com/in/nitin-sarda-06260538/?originalSubdomain=in

The point is that there have been multiple actions which have been taken in the last one year or so and we can also see the results, now how long can they achieve this is a key thing to observe.

Other developments/ initiatives/Points

- They are now focusing more on Saas and recently their flagship products has been hosted in AWS in the global marketplace. This would reduce the lumpiness from the licence business which is like a one time revenue but I think they would have to forgo AMC as you won’t charge that on saas. Q3FY24

- They have tied up with Natsoft to be their strategic partner,to take their products and solutions to the market. But from a strategic perspective not a financial investment

- Current cash position and receivable as on dec 2023

So we can safely say that cash + receivable is about 100cr and they are available at 300cr mcap. They would definitely do something with this cash, if they acquire some company which would definitely be in their cards that would be a major trigger

- 20% is from international business and they are trying to get into the US markets now

- “”If you really look at it, from employees, directors and promoters put together, we are around 35.4% as a holding”” quoted from concall.

I am trying to meet the management, if not I would ask questions in the con call, I am attaching the list of questions I have in my mind, would love if anybody can answer them.

So to summarise, 60-65% is an annuity business which is growing at 15%, so worst case a 10% growth business available at 17 times PE and promising for 30% growth. Currently doing about 20% margins being a 30% margin business and also having about 50cr+ cash assuming if they collect receivable then about 100cr and they have a solid product

Technicials

RISK

If you read the above thread then this stock was a pump and dump stock, If not the entire thread I would encourage everybody to read this post

Shrihari has made 8 PARTS so please read all of them, Promoter integrity is questionable in this company

DIsc - invested, small position less than a 1%, will increase once I get more clarity

2 Likes

Thanks for the in depth research on the company. I have also recently started tracking this company. You have mostly covered all the points, but I have a doubt on management.

Ms. Anisha Shastri who is currently whole time director in the company since 5+ yrs, also has a side venture (named “Reasy”) which is not directly connected to the company’s domain but not very far away too.

She also won an award from ET Now for Reasy (in 2021) and has also appeared on the news channels regarding the same.

Now the point is that this is not a sure shot red flag, but this diverted attention in 2 businesses (of somewhat connected domains) raises a question on dedicated focus to expand and grow Intense. I have not seen any related party transactions hence can’t comment on that aspect.

Attaching links and snapshots with more details,

Links - Women Entrepreneur India features Anisha Shastri|Intense Technologies

Disc. - Under study

I would highly recommend not to invest in intense.i have badly burned my fingers.

4 Likes