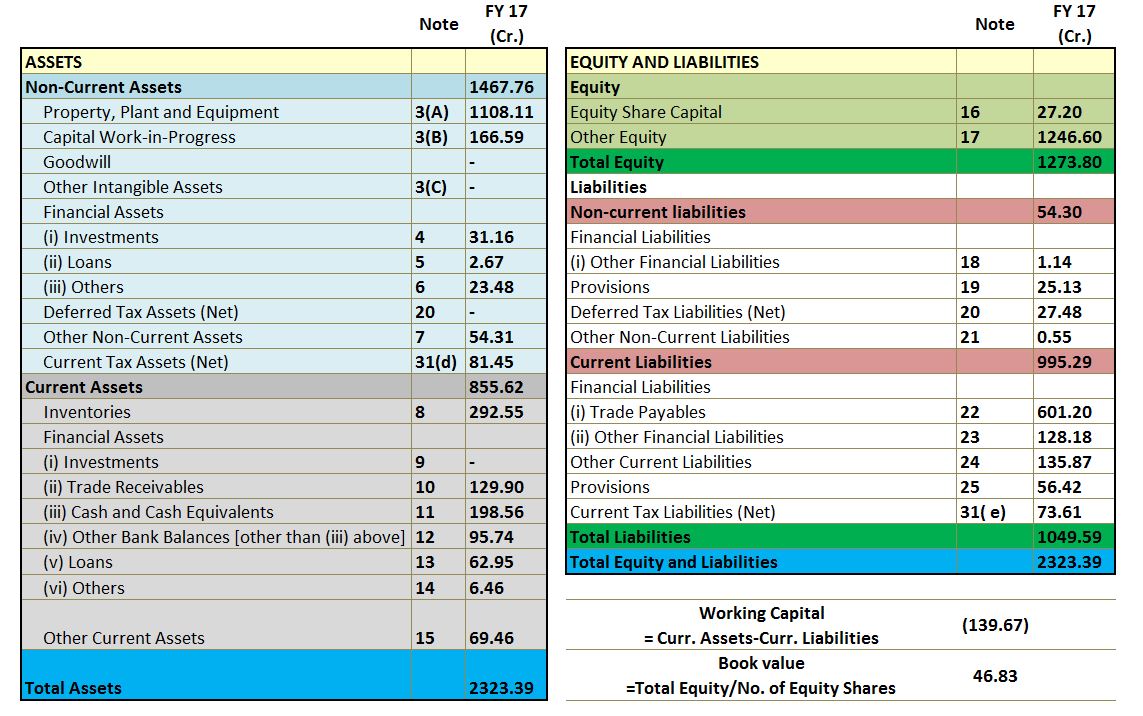

Book Value (BV):

One of the most easily available number besides Price and EPS. Be careful, to take it on face value. Just imagine, you bought a brand new car, which has just reached home and due to some unforeseen emergency you have to sell it off. Will you get the value, which is recorded in your books? NO!

Let’s invert, your old car is used by Salman Khan in one of his movies. Will you get the value, which is recorded in your books? NO….You will get way more than BV due to the X-factor.

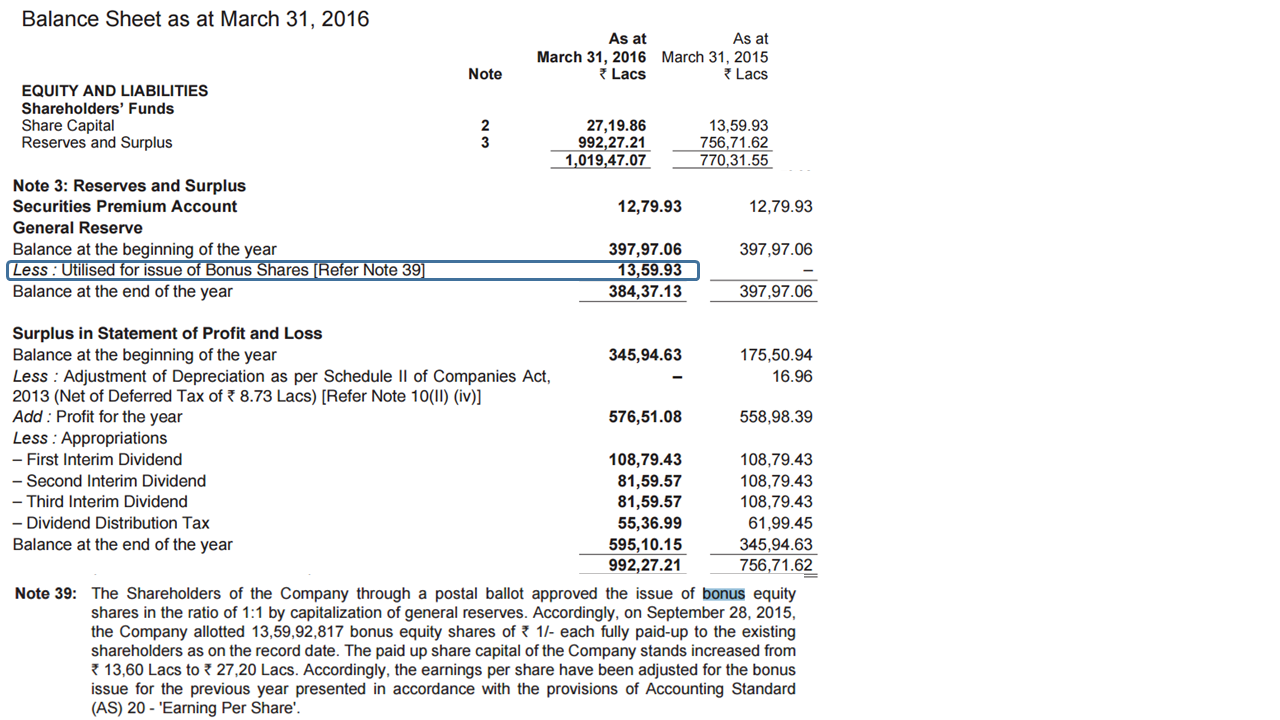

So, BV as a number does not represent the true worth of a company. It might understate or overstate the value.You buy a company on the basis of BV and it’s losing money in operations or accumulating inventory without any demand for the product at snowballing pace without any plans to stop/contain the same. One fine day, BV would vanish. On the other side, BV might contain hidden assets such as Land in Prime location which can be monetized or Brand/Patents etc. which are depreciated, until they disappear from the asset side of the BS or /tax breaks due to previous losses.So, read the AR’s to know –What makes up the BV? More important to do so if you are buying the shares on the basis of BV.

Inventories:

FIFO (First-In-First-Out) or LIFO(Last-In-First-Out) are the two basic accounting methods.

On a lighter note, two other popular methods, really happens to lot of inventories, are GIGO(Garbage-In-Garbage-Out and FISH(First-In-Still-Here).

Too much confusion, what to look for?

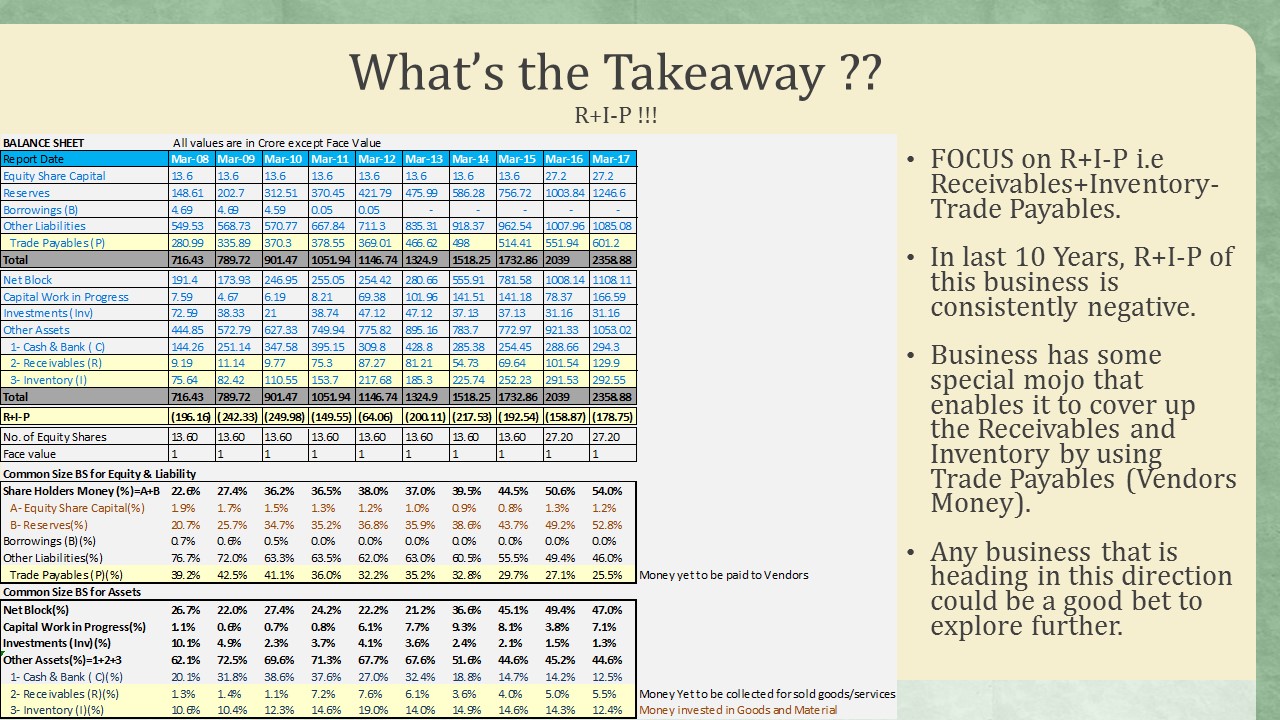

See the trend of inventory w.r.t the sales. Also, See Insight 7.

Insight4: Watch the trend of the Debt factor or Long-Term Debt…See the details of last 10 years, if possible!! Debt reduction over the 10 years is a sign of prosperity. Keep in mind that the Debt factor shows financial strength of a company. Does the company has an overwhelming Pension obligation as these are absolute obligations to pay?

Insight5: Short-term debt can be ignored incase cash on BS or other current assets (inventories, receivables etc.) can cover up for the same.

Insight6: If cash exceeds debt, rest assured that company is not going out of business. Increasing cash relative to debt is a sign of improving BS.

Insight7: It’s a RED FLAG, when inventories grow faster than sales. It’s first sign of turnaround, when inventory start reducing for a depressed company.

The company, used as an example, is financially strong as there is no long term debt in the BS and would not go out of the business due to lack of money.

Question 3: Is the cash real? Where is it kept? Why is it kept?

Question 4: What are the finer details of the debt?

Question 5: What are the components of Book Value?

To answer the above questions, Annual reports/Conference Calls/Investor communication Presentation are needed. Just imagine, AR of last 10 years and each AR contains ~200 of pages. Overwhelming situation and sure shot chance to lose interest in the AR, if one does not know the questions to look for.

Hmm…Too much details, I know.

Let’s take the easy route. Stare at the price of shares you hold at a greater frequency. The stare and frequency might shoot up the Price