Could be this…

Moral of Q4FY17 Results:

States abruptly stopped signing PPAs post SECI Auctions.

1 Like

I would wait for Suzlon results because if this was the sole reason for such bad performance then it should be applicable for Suzlon too.

But really disappointed with results. With such bad performance in past three quarters we see negligible difference on ‘Receivable’ side .

Disc : Invested and Sad

1 Like

With states refusing to sign PPAs, they will probably have to take a haircut, or worse, write off some of the receivables.

And,

Under the new scenario, our conventional order book loses its relevance, since these orders were under an FIT based market regime

Doesn’t look good in the short to medium term.

1 Like

Pfft… what’s the point in having a 45 minute concall in which the first 20 minutes will be spent on reading the Results Presentation line by line?!

-

Mgmt says no financial loss because of states not signing PPAs. 200MW WTGs already manufactured were instead supplied to PSUs with PPAs in place.

-

All the receivables will be cleared out within the next 6 months (We’ve heard that one before, haven’t we?). Don’t expect any write-offs.

-

Q1 and Q2 will be a washout. The projects won in the auction will start getting executed only in Q3 because the PGCI lines and substations will go online only in Q4FY18.

-

Mgmt expects the winning bid price per unit at the next SECI auction to be around 3 rupees.

-

Dodged the question on loss of market share. Obviously.

-

Although I’m not completely sure, some of the regular analysts from the big brokerages were missing (or they didn’t get a chance to ask their question). It won’t be a surprise if brokerages put out a sell rating on Inox wind.

Disclosure: Invested.

4 Likes

As I understand, the significant change is that government has now moved to auction based pricing & has halted signing PPA on old rates.

This has affected Q4. Non-signing of PPA is a temporary thing.

To check whether lower rates has any effect on the margins, I found the below link

This is an excerpt from the same:

Devansh Jain, Director, Inox Wind: Again rather than margins, what I will just give you simple example is what has been happening in the past we have had. We used to have an 80 meter hug height turbine and 93 rotor diameter. In the past three years, the 93 rotor diameter turbine moved to a 113 rotor diameter turbine and the 80 meter hub height has now moved to 120 meter hub height so we have actually increased efficiency or reduced the cost of energy by close to 50% whereas the cost of doing so was not 50% maybe it was 20%.

So, there was an incremental 30% which was available which went towards reduction in tariffs in many states partly, partly went towards better returns for IPPs and partly went towards higher margins going into the future with the 120 meter turbines for us.

Given that, can we expect margins & profitability to pick up in coming year? ( Assuming no more roadblocks )

If so, does it seem a value proposition if somebody wants to enter Inox Winds at this point of time from long term perspective ( more than 3 years ) ?

PE ratio of Inox Wind on moneycontrol is currently at 12.08.

If margins & growth improve from this point, then PE ratio will surely improve.

The price/unit at the next SECI auction will fall further to Rs.3 from the current price of Rs.3.46/unit. So, this will primarily be a high volume-low margin business, which will ensure increased competition to win the orders, affecting pricing discipline in the industry, & hence affecting the margins further. Difficult to see the sector not getting afflicted by Winner’s Curse . Whatever technological edge a competitor might have won’t last long. Others will catch up soon because it’s a question of survival.

It’s a sector completely dependent on Govt. policies. I doubt Mr.Market will give it a high P/E rating even when things are going well.

Disclosure: Invested.

2 Likes

Management of Inox wind have given their views quite clearly about what went wrong and what is likely to dampen the rate of growth in the coming quaters." The old order book has lost is relevance" . This admission by Inox was quiet a shocking one for me i. Although quite apparent in hindsight , i underestimated the extent of disruption that Inox faced from the switch over to Auction based tariffs. Also now we have a clear idea about the timeline required for setting up Grid infrastucture which is going to take untill the end of 2017.

One more big uncertanity over GST rates remains.

Ofcourse the long term story remains intact and there are quiet a few positives for Inox wind.

All things considered , i considered to reduce my positions in Inox and park my funds elsewhere.

Disclaimer : Invested with reduced holdings post results.

2 Likes

I find it difficult to invest in this space anymore. I feel that the worst is over, but INOX has some how not figured it out and Suzlon seems to be racing ahead like a Phoenix from its ashes. I am sold out on my position in Inox Wind and continue to like the other companies like GFL and Inox Leisure. I have full faith in Inox Wind that it will make a come back, but I am in a hurry to make money and this is not helping the cause.

I feel, the Wind sector is not a wealth crating sector.

1 Like

80% of the order book of Suzlon is made up of orders for 120m height turbine with 40% PLF.This turbine was tested for one year and then validated using one year energy generation data. In the meanwhile, Suzlon made changes in the manufacturing set up and now has the capacity to manufacture 1800mw of this model of WTF S111 120m.

On the other hand, inox wind does not have a 120m WTG…it is not listed on its website. In the conference call, the inox mngt talked about a 120m hybrid tower WTG being developed. I think, Inox is yet to do the one year testing and validation of the said 120m WTG and also make changes in its manufacturing set up for the new 120m WTG.

THUS, INOX wind is about 9-12 months behind Suzlon in inyroducing the new 120m WTG which can be used for other than high wind sites. Till that time, the market demand will be captured by Suzlon andcGamesa and Inox will continue to lose its market share.

After listening to the conference call of both Inox and Suzlon…i think Inox not having its own independent R&D is going to suffer in the next 1-2 year. This year Suzlon is unleashing S111 120m…and next year it will be S128 2.4mw…Inox does not have any comparable products.

3 Likes

Is the worse over for Inox Wind?

The worse is not over for Inox. Their falling share prices (52 wk lo/hi 131/253) are not as steep as their falling marketshare (23% to 11%). Most analysts are keeping it under close review with a negative bias. Changes in regulatory environment have resulted in a tight position for all wind energy players. However, it is noteworthy that none of the other two major players (Gamesa & Suzlon) have had as big an impact as Inox.

There are two critical factors that work against Inox in the current competitive landscape:

- Lack of technology to match the LCOEs required in the industry to mitigate the risks of falling prices and eroding margins. Other players already have established R&D bases to leverage from.

- Lack of experience and established relationships is another fallout for the company. If Inox would have managed their relationships better, then their FIT based orders would not have become irrelevant. Suzlon (as claimed) have been executing their FIT orders even after the regulatory changes.

Inox has to up its game and they have to do it quick. They have lost the ability to compete in the short-term. However, without some hard decisions, they may well have to bear worse in future.

The biggest impact of this move was felt on wind power producers like Inox Wind whose order book shrank overnight. With no signing of PPAs, there were no investors willing to buy wind power generators.

Favourable winds blowing? Producers of the renewable power beg to differ

It would take time to build relationships as they progress. And relationships may play a lesser role in acquiring orders going forward as the auction-based system takes precedence over FIT system. However, Inox’s challenges with technology require immediate attention.

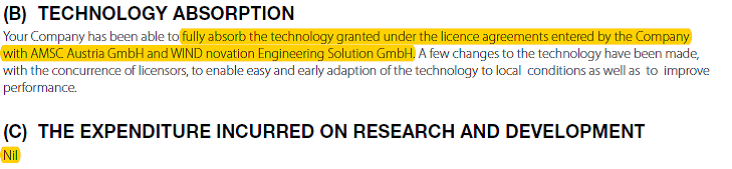

Inox claims that vertically integrated value chain and R&D Focus (Innovation) is its competitive advantage.

(Source: Inox AR 16, Pg. 3)

Research & Development

However, upon digging deeper, I found that:

- The company has not spent a single rupee on In-house R&D

- They have a licensing arrangement with foreign players who have supplied technology to Inox, which they have customized to fit local needs

(Source: Inox AR 16 Pg. 3)

To get a fair comparison, I went to Suzlon’s annual report and found the following:

(Source: Suzlon AR 2016 Pg. 40-41)

Suzlon has continued spending heavily on R&D despite heavy debt and other financial constraints.

What explains the dichotomy? The results and the management commentary indicate that Inox Wind has been aggressive in recognizing order inflows.

Suzlon, which has been in the system for quite some time now (more than two decades), has been more cautious.

According to Kirti Vagadia, group chief financial officer, Suzlon reduced the risk of contract or order failure through risk management practices such as better planning and other processes.

How Suzlon Energy avoided Inox Wind’s predicament | Mint

Vertically Integrated Value Chain

Inox claims to have a ‘vertically integrated value chain. However, the continuous-evolving wind technology has become a primary activity in the value chain which directly contributes to the lowering cost and improving margins. In such a scenario can we truly attribute the benefits of a vertically integrated chain to Inox?

Inox will have to ramp up technology and close the gaps with competitors. Failing which they may not be able to quote competitive prices against other bidders and may risk losing orders. It would be an even bigger risk to bid competitively (just to get orders to save marketshare) against well-equipped competitors (who have pre-bid arrangements with technologically-sound partners). Not only would they lose margins in such a scenario but may even end up adding unviable projects to the order-book.

There are several ways to ramp-up technology:

- Fast tracking In-house R&D - This would incur huge cost, time and effort. At the same time, this is the most sustainable way to survive and grow in the long run. It involves taking short-term pain for long-term gain with bleak chances of revival in FY18 and probably even FY19. Also, a need for capex may push them to take debt which increases leverage in future. Trouble is that even if they are able to catch up with the competitors, building technology as a competitive advantage would be difficult.

- Licensing arrangement – Company can continue to have licensing arrangements with foreign players. This would be a costly affair and they will never be able to become self-dependent.

- Strategic Partnership/JV – Company can get into a partnership with another foreign player to leverage its local market knowledge in return for the foreign partner’s technology. This would be a very feasible solution for Inox. Such a collaboration should take care of its short-term technology needs and give them enough headroom to build inhouse R&D capability. As Suzlon benefitted (purely in terms of technology) from its association with Senvion, Inox may take a leaf out of the same book. Such arrangements however are not long-lasting. Once the foreign partner is well versed with the local geography, it would either ask for a premium for their technology or would part ways and go solo. Within that time frame, Inox should be able to build its technological competence to survive on its own.

- Acquisition – With the backing of a strong Inox Group, Inox Wind can manage the resources to consider buying a wind turbine company (probably a foreign player), which in turn will give it the capabilities in technology and global scope of operations. It is less expected though, as the company must have taken a lesson from Suzlon’s financial trouble following the company’s acquisition spree. Also it might ring bells in the other well-performing subsidiaries of Inox Group too.

Inox will have to take a necessary step towards matching up with its competitors. Going forward the competition will only become more intense and there are serious questions upon Inox’s capabilities. Inox has destroyed shareholder value throughout its short history. The ever falling Inox share price is an excellent example of the notion that probably the market knows more than us and we must always respect the market. One can only hope to see the carnage end. Good luck!

Disclosure: Not invested in Inox Wind. Invested in Suzlon

6 Likes

Well, now I feel like absolutely kicking myself for not exiting fully (instead of only partially) when the stock bounced to 165.

The instant case has been settled. But there is no way of knowing more wouldn’t come.

Either way, the market will react very negatively on monday. Also, an article on Business Standard http://www.business-standard.com/article/companies/inox-wind-faces-insolvency-proceedings-over-non-payment-of-rs-57-lakh-bill-117071401458_1.html starts with

The ongoing insolvency heat has caught on in the renewable energy space with Inox Wind being put under the corporate insolvency resolution process. In a rare instance, a Customs agent, Jeena & Company, has dragged Inox to the National Company Law Tribunal (NCLT) over non-payment of dues totalling Rs 57 lakh. At the same time, Inox Wind has laid off close to 400 employees at its manufacturing unit. A former employee said Inox Wind was yet to clear his final settlement, which was pending for over four months. “The company has no cash flow whatsoever. It is not even able to …

(It’s behind a paywall. So, no idea what the rest of the article says.)

Anyway, hopefully, I can get the hell out of Inox Wind completely on Monday.

Does the Insolvency and Bankruptcy Code 2016 include even accounts payable? somehow it seems invoking insolvency for 57 lakhs worth of unpaid dues (not term loans etc.) is frivolous. Does Inox not have 57 lakhs cash in its books to pay this off? Not sure if there is more to this tory than what has appeared in the news.

Statement from the Company on its website.

New Delhi, July 15, 2017 This has reference to certain news articles published in various publications claiming that Inox Wind Limited (IWL) is “headed for insolvency”, after the National Company Law Tribunal’s Chandigarh bench (NCLT) ordered commencement of the process in response to the plea made by Jeena & Company, an operational creditor.

In this connection, we would like to clarify that IWL has preferred an appeal before the National Company Law Appellate Tribunal (NCLAT), praying that the said proceedings be quashed. The matter has been listed for hearing on Monday, 17 July, 2017.

Further, IWL has already settled the dispute with the operational creditor, Jeena & Company.

It is also important to mention that fundamentally, IWL remains a solvent company in excellent financial health. Its average revenues for the last three financial years, based on audited accounts, were Rs. 3,525 crores, its earnings before interest, depreciation and taxes Rs 627 crores, and its net profit Rs 354 crores. It has a net worth, as of 31 March, 2017, of Rs 2,190 crores, and the company has a cash balance (including liquid investments), as of that date, of Rs 749 crores. The company has been regular in servicing all its commitments to its lenders, and has a long term rating of AA- and a short term rating of A1+ from CRISIL, India’s leading rating agency.

Reposting Something I posted back in September 2016 on the Wind industry and on Inox.