It has been a part of Gujarat Flurochemicals bag, after the 18x IPO subscription, I feel its going to go to 600 in this calender year and then in next 5 yrs due to the stress on Green enery go to 1000+ levels even paying good 200% dividend regularly just like its parent does. I feel after reading many IPO buy reports by brokerages and analysts it is a good one even if it opens at 400+ or say for that matter 420 odd levels.

Excellent result declared for Q4FY15. Even I find this idea multi year compounding. Any view on technology support for WTG produce by the company?

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=5319af60-db9c-4aad-89d4-f6837a4214c2

Call was addressed by Deepak Asher, Director.Key Highlights by Capital mkt

Sales volume including equipment and turnkey supply, in FY’15 stood at 578 MW as compared to 330 MW in FY’14. Commissioning however stood at 274 MW as compared to 150 MW for FY’14.For Q4 FY’15, sales volume including equipment and turnkey supply, stood at 198 MW as compared to 132 MW in Q4, FY’14. Commissioning however stood at 94 MW as compared to 130 MW for Q4 FY’14.

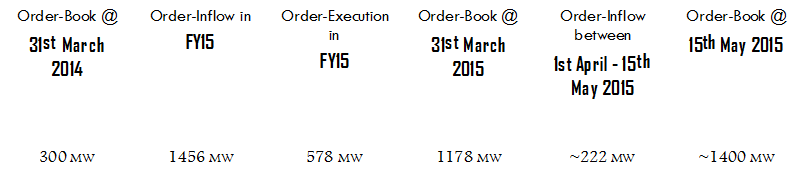

Total order book as on Mar’15 stood at 1178 MW which is to be executed in 12-15 months. About 124 MW of orders added in Q4 FY’15. Current order book position as on May’15 stood at more than 1400 MW. Of the order book, 70% are binding contracts while rests are term sheets to get converted into contracts before Q2 FY’16.

About 96% of total order book are third party orders and are pretty diversified and with reputed clients including Green infra, Tata Power Renewable, Bhilwara Energy, Renew Wind Energy, Hero Future Energy, NHPC, RITES, Continuum etc. Large enquiries of orders are coming and management expects further orders to come in as FY’16 progresses.About 53% of total order book is Turnkey and Equipment sale, while rest is Equipment sale orders. State wise, about 48% of orders are to be executed in Rajasthan, 27% in Madhya Pradesh and around 20% in Gujarat.

Company is also entering Maharashtra and AP during FY’16 and also Tamil Nadu, which is a big market as far as accelerated depreciation, is concerned.96% of orders are from IPP and utilities, while less than 3% of order book are from customers for getting the accelerated depreciation benefits. As FY’16 and FY’17 progresses, there is a large pie of accelerated depreciation market, which is yet to be tapped. Management expects this market to be as high as 1500 MW in FY’16 and FY’17.

Company’s current capacity is about 800 MW of turnkey and equipment supply. It is expanding its Naxals and Hubs capacity in Himachal Pradesh plant. Further, Madhya Pradesh plant which is going to be first ever fully integrated one with Naxals, Hubs, Rotor blades, Tower construction capacity etc will gradually commission during FY’16. Thus, by FY’16, the manufacturing capacity will almost double to 1600 MW. Average capacity for FY’16 will be about 1200 MW.Company’s Ebidta margin of 16.9% for FY’15, is highest in the industry. As per the management, with new capacity coming on stream there will be benefit of economies of scale and this will lead to higher margins.Company’s current debt equity ratio is 0.6. Management expects to be nearly net debt free as FY’16 ends.

3 Likes

Note :

This is just a statistical representation of facts & figures and is part of a general discussion and is not in any way a Buy/Sell/Hold recommendation of any sort. In this post Indian Wind Energy Sector is discussed in general and Listed & Unlisted Indian Wind Power Solution providers are discussed in particular without any opinion of Buy/Sell/Hold. This post should only be taken as a tool to have an overview of background as well as statistical facts & figures which are widely available in public domain like company prospectus, industry articles & magazines, annual reports, etc. No investment/divestment decision should be made based on this post.

Discl. - Invested in Inox Wind

– Inox Wind Ltd. is a part of Inox Group of companies which has two other prominent listed entities viz., Gujarat Fluorochemicals Ltd. (GFL) & Inox Leisure Ltd… GFL still holds 63 % stake in Inox Wind whereas total promoter shareholding of the company including those held in promoters’ personal capacities stands at 85.62 %.

– Inox Wind is a complete Wind Power Solutions provider having two manufacturing facilities at Himachal Pradesh & Gujarat and the third one ( touted to be the biggest in Asia ) at Madhya Pradesh which is under construction and likely to commence operations in phases starting 2HFY16.

– Company manufactures Wind Turbine Generators (WTGs) including all its key components in-house like Nacelles & Hubs, Rotor Blade Sets & Towers. In addition, it is a complete solution provider to the Wind Energy sector in the sense that it also provides allied services like wind resource assessment, site acquisition, infrastructure development, erection & commissioning, operation & maintenance, etc.

– Current Installed Annual manufacturing capacity of the company stands at 800 MW which was expanded at the fag-end of Q4FY15 to 1100 MW and is expected to be enhanced further to 1600 MW by Q1FY17 with a potential to enhance it further to 1900 MW (via MP plant).

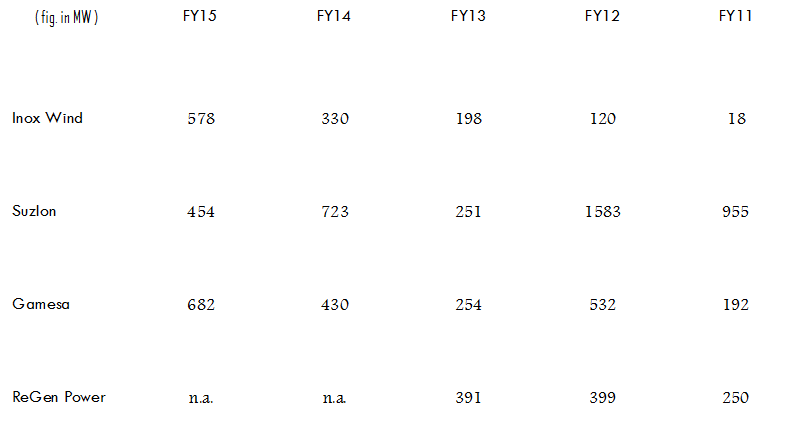

– Inox Wind was the 4th Largest player in Indian Wind Power solutions industry as at FY14 (in terms of annual installations done), and, although statistical details are still awaited, seems to have migrated to become the third largest player in the industry as at FY15 next only to Gamesa & ReGen Powertech (ReGen’s figures of FY15 are not known but recent Industry Association data suggests only these three players gaining marketshare in FY15).

Sales in MW of major Indian Wind Power Solution Providers

( together these 4 players constitute 59 % of total installed WTG manufacturing capacity of India &

~ 90 % of FY14 yearly installation done all over India ) :

– Company commenced full-fledged operations in FY11 and since then has grown quite aggressively at a CAGR of 138 % in volume terms, at a CAGR of 147 % in value terms, at a CAGR of 149 % in EBITDA terms & at a CAGR of 160 % in PAT terms.

Sales in INR of major Indian Power Solution Providers

( together these 9 players constitute ~ 90 % of total installed WTG manufacturing capacity of India ) :

– Industry is very working capital intensive in the sense that, companies need to invest beforehand and build huge inventories and often get paid only at the completion of the project. This could be one of the reasons why Inox Wind has exhibited negative OCF almost consistently since inception.

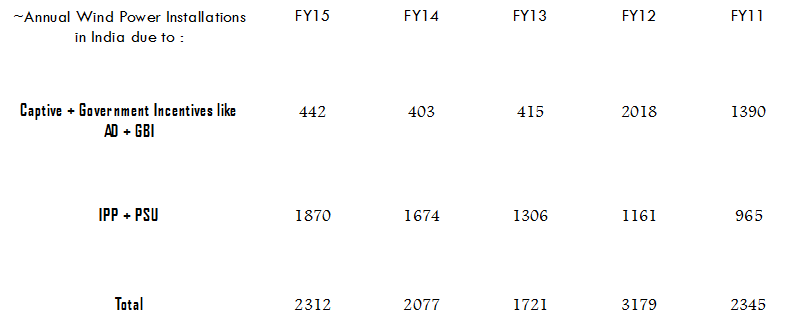

– FY13 & FY14 were tough years for the industry in general as various incentives provided to Wind Energy segment by Indian Government were withdrawn. However, Modi-led government reintroduced the incentives in FY15 and has set an ambitious target of 10,000 MW yearly installation v/s ~2300 MW yearly installations currently :

– If we cite independent report published by CRISIL in early 2015, then it pegs yearly Wind Energy installations to rise to 4100 MW per year in FY17 from current ~2300 MW per year.

– Its almost an oligopoly industry wherein top 5 Wind Power Solution providers constitute more than ~85 % of yearly installations & Top 3 players constitute more than ~70 % of yearly installations.

– Entry into the segment requires good financial muscle as well as access to technology to produce WTG. This is the reason why there are not more than 10 prominent players in the segment.

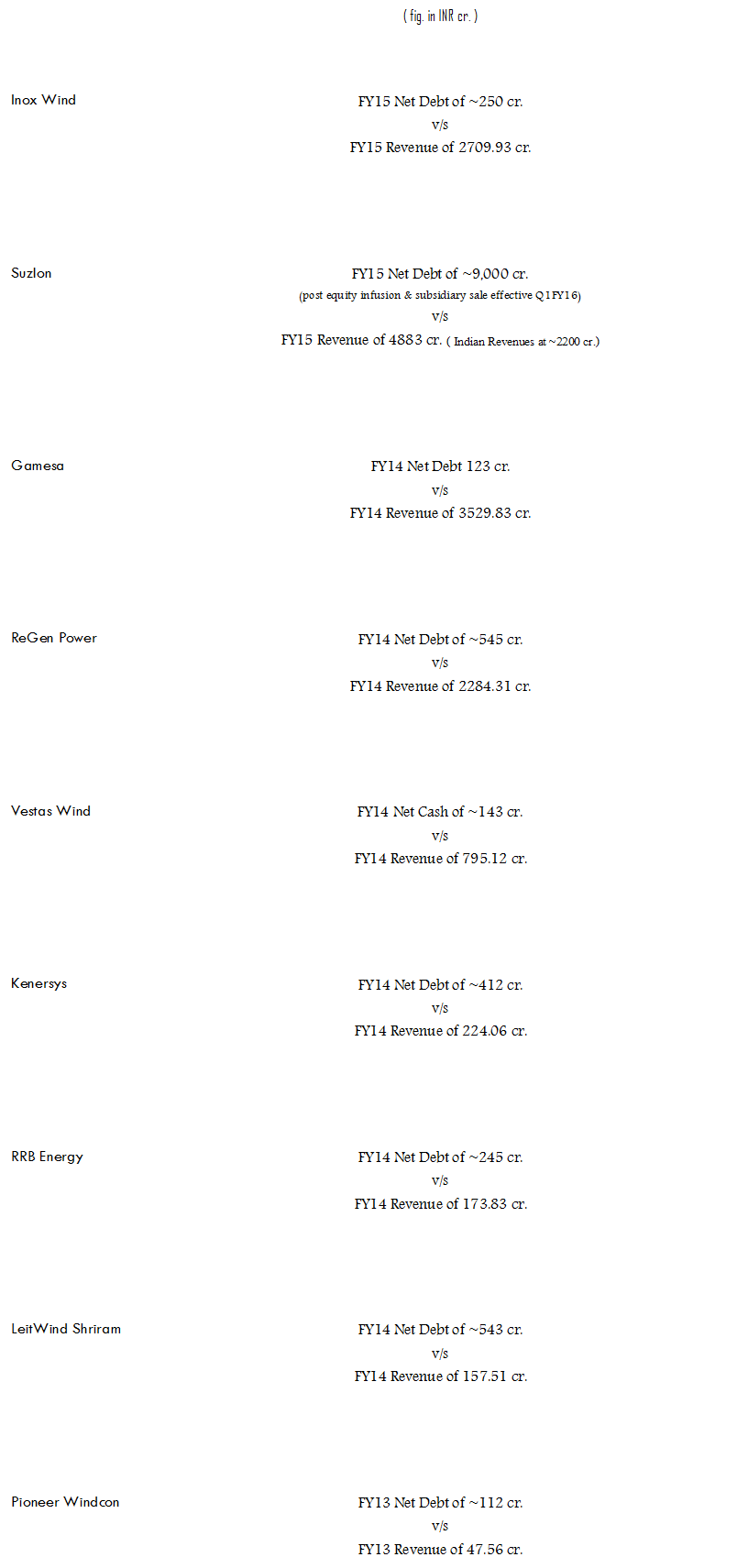

– Key to sustenance & growth in the segment could be balance sheet health of Wind Power Solution provider as the nature of the industry puts extreme stress on the balance sheet. Stated below is an overview of balance sheet health v/s scale of operations of almost all major Wind Energy Solution providers of India :

Balance Sheet Health of major Indian Power Solution Providers :

( together these 9 players constitute ~ 90 % of total installed WTG manufacturing capacity of India ) :

– Gamesa, ReGen Powertech & Inox Wind seem to have reasonable balance sheet health vis-a-vis respective scale of operations. Vestas is focussing more on O&M (Operation & Maintenance) revenues and not looking at aggressively tapping new installations. Suzlon, with recent Dilip Shanghvi backing, is planning to aggressively tap Indian market again, especially Accelerated Depreciation (AD) market.

– Inox Wind’s current revenues as well order book are largely from Independent Power Producers (IPP) with only ~ 3 % coming from AD segment. AD segment is relatively easy to tap as they don’t have stringent quality requirements as also their payment terms are relatively better.

– With an order book of 1178 MW as at 31st March 2015 (worth INR ~5400 cr.) & ~1400 MW as at 15th May 2015 (worth INR ~6400 cr.) to be executed within 15 months or by 2HFY17 and the average capacity available in FY16 worth ~1200 MW, company seems to have almost tied up entire capacity for FY16 and so aggressively exploring AD market seems to be impossible for Inox Wind in FY16.

Order-book Trend for Inox Wind Ltd. :

– There are basically three kind of orders, Inox Wind executes –

(1) ‘Complete Turnkey Solution’

which includes entire lifecycle of Wind Farm project including supply of hardware (WTG, etc.) as well as providing of services (starting from identification of suitable sites for wind farms to ending with implementation & operationalisation of wind farm).

(2) ‘Only Equipment Supply’

which includes only supply of hardware (like WTG, etc.)

(3) Operation & Maintenance (O&M)

which includes operation & maintenance of WTGs sold. First two years are free-of-cost post which ‘Annual Maintenance’ (AMC) type contracts are entered into.

– In FY15, ~12 % of the sales (68 MW) came from ‘Only Equipment Supply’ whereas ‘Complete Turnkey Solutions’ contributed 88 % (510 MW).

– Since for first two years O&M is free-of-cost and company started meaningful operations only from FY12, starting FY16, ‘O&M’ revenues could start flowing in which are very high margin (~30-40 % margins).

– Out of the current order-book of 1178 MW as at 31st March 2015, 53 % (624 MW) is for ‘Cmplete Turnkey Solutions’ whereas 47 % (554 MW) is for ‘Only Equipment Supply’. Since ‘Only Equipment Supply’ orders enjoy relatively lesser risk as well as better collection periods, working capital intensity could considerably improve for the company in FY16.

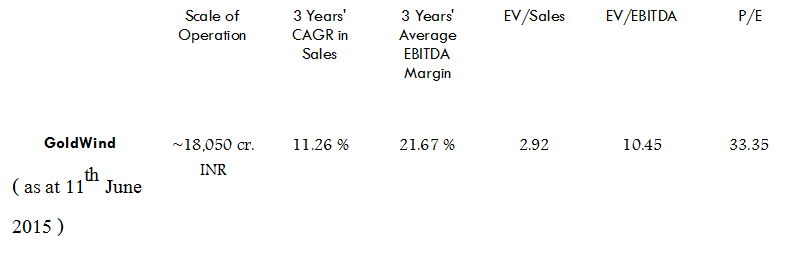

– Mentioned below is the valuation matrix of Inox Wind vis-a-vis other major Indian Wind Power Solution Providers :

– Inox Wind Ltd. seems to be enjoying the second best EBITDA margins globally next to only Goldwind of China. Valuation multiples enjoyed by Goldwind are :

Key things to note with regards to Indian Wind Energy sector in general & Indian listed Wind Power Solution providers in particular :

– Although government has set ambitious targets for renewable energy sector (raising yearly wind enrgy installations 5 times the current size), financial health of Indian IPPs is not that good which lengthens the collection periods.

– High Inventory of Wind Power Project sites is key for success of Indian Wind Power Solution providers.

– Wind Power Solution providers need continuous investments to acquire project sites, buidling capacities and managing high working capital needs. Hence, financial health of a Wind Power Solution provider is key and lets it sustain in lean phases and expand aggressively in boom phases.

– Without adequate financial strength and just piling on debt to expand aggressively results in disaster in the long run as is evident in the case of Suzlon.

– Suzlon has diverted its focus again on Indian market post backing from Dilip Shanghvi. It plans to capture 35 % marketshare in FY16 and 50 % in FY17. However, except huge capacities available and backing of a strong group, if we look at track-record over last few years when Indian Wind Energy market witnessed significant headwinds in the form of withdrawal of incentives by the Government, Suzlon was one of the worst sufferer. In contrast, Gamesa, ReGen Powertech & Inox Wind captured significant marketshare.

– Also, looking at the order-book of Inox Wind & Suzlon, they seem to be neck-to-neck with Suzlon’s order book as at 31st March 2015 standing at 1123 MW (+450 MW from Dilip Shanghvi JV) as against Inox’s at 1178 MW. It is to be noted that out of 1123 MW order-book of Suzlon, some orders are 3 years old.

– Suzlon expects to execute ~1100-1200 MW orders in FY16 and although Inox Wind management has refused to give guidance, but considering the fact that its order-book execution period is 15 months, it also seems to be expecting ~900 MW worth of execution in FY16. If we combine these two then it seems Indian Wind Energy market could see good jump in installations in FY16 itself as against CRISIL’s expectation of FY17.

– Inox Wind and ReGen Powertech seem to be the only Indian players who exhibited resilience in an otherwise tough market with Inox growing quite aggressively even in the bad environment. Gamesa rebounded very well from a one year blip. All other players including Suzlon, Leitwind Shriram & RRB Energy witnessed significant negative growth over the period. Vestas which was a key player in Indian market before, turned its focus on O&M business and intentionally went slow on new installations.

– Generally, 2H of the fiscal is heavy in terms of order execution whereas 1H is heavy in terms of order booking for any wind power solution provider. Therefore, it will not be surprising to see 65-70 % of the total yearly revenues getting booked in 2H of any fiscal.

– Inox’s product dependence seem to be high as it offers only 2 MW product.

– Post fund infusion via Dilip Shanghvi as well as proceeds from subsidiary sale, Suzlon’s debt will come down to ~9000 cr. INR in FY16.

– Inox Wind Ltd. might go for second round of funding before FY18 as its promoters will need to dilute their stake from current 85.62 % to 75 % because of regulatory requirement.

Note :

This is just a statistical representation of facts & figures and is part of a general discussion and is not in any way a Buy/Sell/Hold recommendation of any sort. In this post Indian Wind Energy Sector is discussed in general and Listed & Unlisted Indian Wind Power Solution providers are discussed in particular without any opinion of Buy/Sell/Hold. This post should only be taken as a tool to have an overview of background as well as statistical facts & figures which are widely available in public domain like company prospectus, industry articles & magazines, annual reports, etc. No investment/divestment decision should be made based on this post.

Discl. - Invested in Inox Wind

11 Likes

Nice post Mahesh.

Apart from the GBIs, the govt. also provides incentive in the form of RECs, which have gained traction of late.

I’ve been scouting for companies in the Renewable Energy sector and found Ujaas and Inox Wind to be the only interesting listed companies from the balance sheet perspective (ignoring valuation for a moment). Is there any particular reason you would choose one over the other? Ujaas is an order of magnitude smaller (even in terms of marketshare in its subsegment).

Suzlon had some issues with cracking in blades. Do you know anything about the quality of Inox’s Wind Turbines?

Rgdg., Inox v/s Ujaas, First & foremost is the management…I had attended an analyst meet of Ujaas and found management to be very desperate to convince analyst/investor community rgdg. the potential of the sector as well as company…that was a turn down for me…infact that thing continues even today if you see the recent announcements made by the company regarding RBI directives and APTEL order…I don’t like managements who like to communicate such small small things and convince the investors that everything in the sector looks rosy…

I feel in case of adversities, Inox will be relatively more resilient and will be able to bounce back with much more vigour than Ujaas…

Rgdg. your second query asto quality of Inox Wind products, industry feedback suggests them to be of very good quality and are particularly pleased with the way client relationships are handled by the company.

Rgds.

Discl. - Invested in Inox Wind

Mahesh,

First of all, good efforts in bringing out data/analysis ( as is the case always). A few thoughts here.

- See the DSO around 180 days. Reflects high gestation period and lack of pricing power.

- Wind IPP have a long pay back period and most of the IPP’s are not profitable.

- Please note IPP’s dont have control on the end product as the price is determined on cost plus basis in most of the cases.

- Land availability is a question mark as both solar and wind will compete for the same land.

- Your data itself shows there is no secular growth in wind power installations.

- My main problem here - how i determine the market size and see that enough room is there for Inox.

- Also compare per mw cost in wind, solar and COAL- Coal is coming in a big way and you will not find guys going for wind IPP. Coal thing is very obvious and we cannot go by projections of CRISIL for growth in installed capacity. Solar per mw is almost near to wind and is not capital intensive like Wind, Also, maintenance is very low and equipments have a longer life than wind.

- One more risk - GOVT subsidies, AD

In my view, not a good business for LT but one can take a view till 2018 and play because of a good and cash rich promoter.

Not a good business for long term

3 Likes

Without disputing any of the facts (although some seem unreasonably harsh on particularly Wind Energy sector) presented by you (some like working capital intensity & bad IPP financial health already mentioned in my post), some things need to be noted :

(1) Post Modi-led government coming into power, macro seem to be favourable for Wind Energy segment which were otherwise not in FY13 and FY14.

(2) If you see the order book of Inox & Suzlon and the execution period and if we assume Suzlon stands by its word and Inox continues its track-record of exceptional execution skills then targets mentioned by CRISIL seem reasonable. Also, if you check pre-FY13 era when full blown incentives were inplace (which are now majorly reinstated), installations were already at 3179 MW.

(3) The problem is post FY17 what will happen when competition will start pushing aggressively because of revival in the sector…its a fact that other players like Kenersys, Leitwind Shriram, Windwind, etc.have spare capacities available and its only majorly because of their financial health that they are unable to compete for now…also, what if Vestas again decides to focus on Indian market…these are the questions which will remain but what is interesting is in my next point…

(4) It seems atpresent if I look at only micro then with Inox Wind I am able to ride entire lifecycle…there has been no major acquisition yet, company is having global ambition but even there is no foundation laid so far for that, there is no divesification within Indian renewable sector, paid-up value of the stock is still full Rs. 10, promoters stake is very high at 85.62 %, etc. With these factors for me downside safety is good and that is my first preference.

Promoters could have easily diluted more at this valuation and brought their stake to 75 % but they didn’t…they left scope for further fund-raising which is crucial to sustain in this sector…and with this in case of any failure they seem to be loosing more than minority shareholders which is very important.

(5) If we focus on business, then in FY15 the gross order inflow for Inox Wind was 1456 MW…available capacity for the company in FY16 will be 1200 MW and for FY17 will be 1600 MW…by May 15th of current fiscal it received a further order inflow of 222 MW… 70 % of these orders are binding contracts (all these data are from the company management commentry in the concall)…so, if the company is able to secure another 800 MW order in FY16 (which will mean total gross order inflow of 1022 MW in FY16) to be executed in FY17 then it means it will get tied up for FY17 also with good growth (80 % utilisation)…

(these figures are the derivation from available facts and figures and in case company doesn’t execute orders or faces order cancellations for 30 % of the non-binding contracts or delay in 70 % of the binding contracts then the things could be different)…

(6) With the IPO funds raised, company will be able to expand to ~1100 MW and plans to expand to 1600 MW via MP plant at an expense of ~200 cr. which will be met via internal accruals and debt…47 % of the order-book comprises of only equipment supply orders and expected cash generation in FY16 is 500 cr. (CRISIL estimate).

(7) So, if till FY17 company can exhibit good growth by keeping net debt under control in the range of 500 cr. and then fund-raising is compulsory till FY18 (unless promoters sell their own stake which seems illogical to me)…~3.14 cr. fresh equity shares will need to be issued or a mix of promoters stake sale and fresh share issue might need to be done…so, equity funding for further expansion might be done by FY18 which might take care of further 2 years growth…and here in these many years, if the company can improve on margins that might be an added bonus…

(these are all some of the assumptions based on which I have made initial investments in the stock. My average purchase price is INR ~410 per share…Calculations of these are made based on the data mentioned in prospectus, industry artcles and data, credit ratings, concall commentries of Inox Wind & Suzlon, etc. These might not come true as the sector and companies of the sector have often in the past exhibited volatile financials.)

Note:

This is just part of a general discussion and in response to specific query by a forum member. No Buy/Sell/Hold decision should be made on this post as this is just for information purpose and nothing else. No one should make any investment/divestment decision based on this post.

Discl. - Invested in Inox Wind

2 Likes

I looked at inox today - IMHO, suzlon seems a better bet - inox rode on the white space when neither suzlon nor gamesa nor any of the majors were present in Indian market because of unfavourable policy regulations.

Look at cash flow from operations - it’s substantially negative. That’s quite a worrisome sign - remember that companies do not go bankrupt because of lack of revenues but go bankrupt because of liquidity.

of course market feedback is that inox is always the L1 in any project and hence wins it offering the best price and credit terms. Not something I would like to hear for a long term value creation.

at 6 x PB this is valued like google - one has to remember this is a regulated, government finances sensitive sector.

Look at FY 15 investor presenation

- receivables have gone up 100 % while sales has gone up 73 %

- they have more than 50% of FY 15 revenues locked up in receivables. That’s a lot

-operating cash flows are consistently negative and hugely so - this reminds me of real estate and infra companies the ga ga years of 2007 and 2008. for that matter, suzlon in 2007 - when their revenues were growing but cash flows were not. We all know what happened

Optically D/E looks ok because they just raised Rs. 1000 Cr. otherwise it would have been 1:1 with negative cash flows.

I am quite surprised this was touted as a great IPO - it seems like the company sold stock to wriggle out of tight finances at the right time.

if this had happened in 2013 or in 2012, this would have not passed muster. Cash discipline is the most important in EPC, infra projects

Counter views welcome.

9 Likes

Mahesh, thanks for putting your views.

Looking interesting to me also.

However a few concerns which is making me not to bet heavily-

-

Working capital days is high in the industry. As per industry guys, its closer to 150 days.

With such high days of WC & high days of account receivables, chance of bad debt looks high.

If your customers don’t make money, can you make a lot off them? -

Project execution risks looks to be there. Finding site, getting approvals, doing land acquisition… may cause unnecessary delays to the project. Can Inox really avoid these to grow substantially from here?

-

Valuation looks high currently as company is in high growth stage. What are the chances of PE de-rating after say 2 years?

I am assuming then to reach 1GW of production (nearly 2x of current) & hence post a pat of 2x of FY15 pat. But how much multiple would you assume after 2 years? Won’t it be substantially lower than current one, thereby eating most of our returns?

Disclosure- Minor Holding

Its a wrong inference that Inox ‘rode on the white space’…Agreed Suzlon had its own set of problems because of which it was not able to focus on India…but, that can’t be said for other players like Gamesa, ReGen, Leitwind, etc…if you read annual report of parent of gamesa it was not that it wanted to slowdown in India but instead it was finding difficult to grow in India for the respective period…same is the case with other players like ReGen and Leitwind…It infact seems more the result of the effective business strategy of the company than other things…also, as the company was not having huge capacities and was just beginning that must have helped but that could have backfired also but it didn’t which is commendable…Its a fact that company grew in a shrinking market where except suzlon everyone was eager to win contracts…

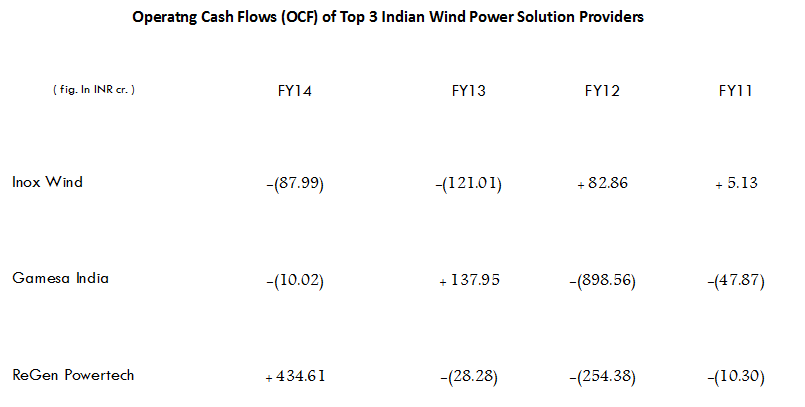

Agree on your negative cash flows side and that’s a concern for me also but I think being this fiscal only sixth full fiscal of operation and having grown at a CAGR of ~140 % since inception, company deserves to be given slight time…However, there is no denying of the fact that other industry players are also facing the same situation. Provided below is OCF situation of top 3 players of the industry :

If a company even after quoting most favourable terms can operate at industry best margins then its a good thing, especially when the sector seems to be on the verge of revival…Also, if I look at client list then they are very reputed names from which company has won orders like Continuum, Tata Power, CESC, Renew Energy, Green Infra, etc…key is again generation of positive OCF and FY16 might be crucial for that…

(1) Yes…high wc days is the norm of the industry especially because of the way it works but key is profile of clients…most of the clients that I can see are most reputed names in the industry and are backed by good funding source…however, there is no denying of the fact that if a large client defaults bad debt can be an issue…

(2) This doesn’t seem to be a larger issue atpresent especially at the scale at which company is operating…already ~4000 MW inventory is already built up by the company…also, except top 5 players, other players lack the required financial muscle to built up the huge project sites inventory…

(3) What I have assumed is that at worst companies might get valued at 9-11x EV/EBITDA in FY17-end when second round of fund raising might take place…the key downside risk is if company goes to average industry margins of 10-12 % EBITDA or if there is significant negative government directive wrt. sector and these risks will remain…

Rgds.

Note:

This is just part of a general discussion and in response to specific query by forum members. Wind Energy sector in general and Unlisted & Listed Wind Power Solution providers in particular are discussed with statistical facts & figures here and there is no investment/divestment opinion aimed to be constructed out of this. No Buy/Sell/Hold decision should be made on this post as this is just for information purpose and nothing else. No one should make any investment/divestment decision based on this post.

Discl. - Invested in Inox Wind

2 Likes

@Mahesh sir, As usual great analysis. There are some queries that i have and they are related to the technical aspects. Do they have manufacturing facilities for all of their products ? Has there been any complaints regarding their supplies till date ? Have you looked at a company from sort of a similar space , albeit unlisted, Mytrah Energy ?

@Ravenrage

Company’s main product is WTG…it has manufacturing facilities for all the key components of WTG viz., Nacelles & Hubs (550), Rotor Blade (400), Towers (150 which will be enhanced to 300 in FY16)…MP plant which they are planning to commission this fiscal (FY16) will be fully integrated and will manufacture all key components at one place viz., Nacelles & Hubs (400), Blades (400) & Towers (300)…It will be great if you refer the prospectus of Inox Wind…you will find all info there.

I haven’t heard any negative feedback for the company yet…but its better all the members activate their ground feedback machine and gather as much info as possible…

Mytrah Energy is I think IPP and not a wind power solution provider…in simple words its a client of wind power solution cos. like Inox Wind…

Rgds.

Discl. - Invested in Inox Wind

I would ask investors to go through prospectus and answer following issues:

- What is cash investment by Inox Group in the company? While the management is good reputation, it worth noting that during FY12 and FY13 substantial sale happen to Inox group. The profit generated from this group sale has created profit balance which was utilised by the company to issue bonus shares and reduce its cash cost substantially which was later divested through offer for sale at substantially high price. While nothing wrong in that, personally, I did not like divestment at very high price. Same was case with Reliance power.

- Technology. They have sourced technology from some European company which was in financial problem. One can not have business model which is constrained by technology in this sector.

- Why not to investment in Gujarat Flouro which is positive cash flow and diversified company then Inox Power? Any market price change shall indirectly also benefit parent company.

I do not hold any shares in company but did evaluated investment in the company and passed due to above cited reason. Individual investors are advised to take their own decisions after reading all information.

The more I dig here, the more skeletons I find out

AMSC has decent WTG technology but by no stretch of imagination can it be called a market leader. Infact, regen for eg., has gearless technology (again franchised out). long term performance of AMSC turbines in India is yet to be tested out.

the group actually sold down their stake. when i looked at the pre-IPO financials, I actually thought for a moment if this was a candidate restructuring program - the numbers looked that bad. Sans the IPO, the company would be in CDR now.

Lowering promoter holding, increasing leverage, negative cash flows, stretched receivables - now where have we heard that before - infra/ real estate in 2007, suzlon in 2009/10.

I would not put my money into a business that cannot generate positive operating cash flows, leave alone free cash flow - remember that in this sector 40% of sales aas receivables is the norm, this company has 50% - and that 10% is the difference in margin between it and its peers - Just saying, red flags galore in this - if you look through it from the view of a cash flow prism.

2 Likes

Pls have a look at the ambit report on inox wind . highlights several issues 20150617 - Inox Wind - Visit Note - Ambit.pdf (431.0 KB)

- poor cash cycle

- no provision for warranty claims and ZERO R & D show exalted EBITDA

- AMSC, its technology partner itself is under financial duress - from the checks I have done, AMSC has a really poor reputation for its technology and its earlier technology partner ghodawat energy ran into problems with installations. None of inox’s wind installations are more than 5 years old. Its technology is not a patch on suzlon or gamesa - a fact I independently veritified with a retired wind mill veteran.

- inox brand itsself is not owned by the company - which is ridiculous.

- 50-60% of its installations so far have been for its own group entities - for earning carbon credits and hence true blue third party customers are of less than 3-4 year vintage.

- they have zero installations in TN/AP - which have the highest power of wind power in India and are the toughest markets to compete in.

- inox’s land banks are limited to central and western india and this is expected to be a bottleneck going forward.

- unlike suzlon, inox’s technology agreement prevents it from exporting wind turbins which is a big road block - hence, they have the smallest capacity of all the wind mill guys

net, net it’s a business that just had a good time imho, when suzlon was struggling and the large majors did not focus on india given the withdrawal of subsidies and issues around land acquisition in india - while FY 16 looks promising, market checks indicate that suzlon is rapidly booking new orders and visibility beyond FY 16 seems hazy.

If orders slow, cash flow issues will come up soon enough and negative OCF’s which have been ignored by the market will start exerting pressure on the balance sheet.

4 Likes

One of the most comprehensive report on Inox Wind…excellent work by the ambit team…kudos to them…

Vardha on your points…

(1) Completely Agree.

(2) Completely Agree.

(3) Partially Agree…infact my feedback suggests no problem with the quality of Inox’s products…only problem with the limited range of products company offers which could work to its disadvantage…

(4) Disagree…this is not a major risk as its a umbrella brand and not company specific brand…all entities combined form Inox group.

(5) Partially Disagree…I think you haven’t gone into detail…out of 1244 MW so far executed since inception, only 255 MW or 21 % belong to group entities…but yes all third party installations must not be more than 3 years old.

(6) Disagree…infact this could in another sense actually be advantageous for the company…

(7) Partially Agree…but is not a major risk…

(8) Again, this could be in a way good for the company…at one point we are concerned of tech.partner’s financial strength and on the other we are concerned of not deep relationship with the partner seems contradictory…

Again Vardha, although you could be right, but I don’t find this argument logical but that only time can tell…look at the profile of clients…IPPs involved do proper due diligence before awarding any contracts…look at the order execution track record…look at current order book which again is 96 % from IPPs…look at the breakup of order book which is 47 % only equipment supply…look at the order size…all these doesn’t seem just a flash in the pan…

Agree Suzlon is getting aggressive but it’s more of the Dilip Shanghvi support that is working in favour of Suzlon as otherwise suzlon’s name has become very bad I the industry…

Completely agree if orders slow it could be a disaster for the company and FY16 is therefore crucial for the company…if it can have even a gross order inflow of 1200 MW in FY16, it might silence all critics…also key to watch will be Suzlon vs Inox order inflow…that might be key determinant of market valuations as in FY16 Suzlon is expected to put its best foot forward. Let’s keep our fingers crossed and watch the story as it unfolds in Indian wind energy solution provider space.

Rgds.

Disco.- Invested

2 Likes

Varadharajan,

Excellent report.