In the AGM notice, Special Business no.4 - re-appointment of Shri Rajeev Gupta as Whole-time Director, Remuneration (pending shareholder approval) is up-to Rs.80 lakh per annum. Is that a fair remuneration by Industry Standards?

Can someone explain it to me why is the stock correcting inspite of showing such an impressive sales growth ?

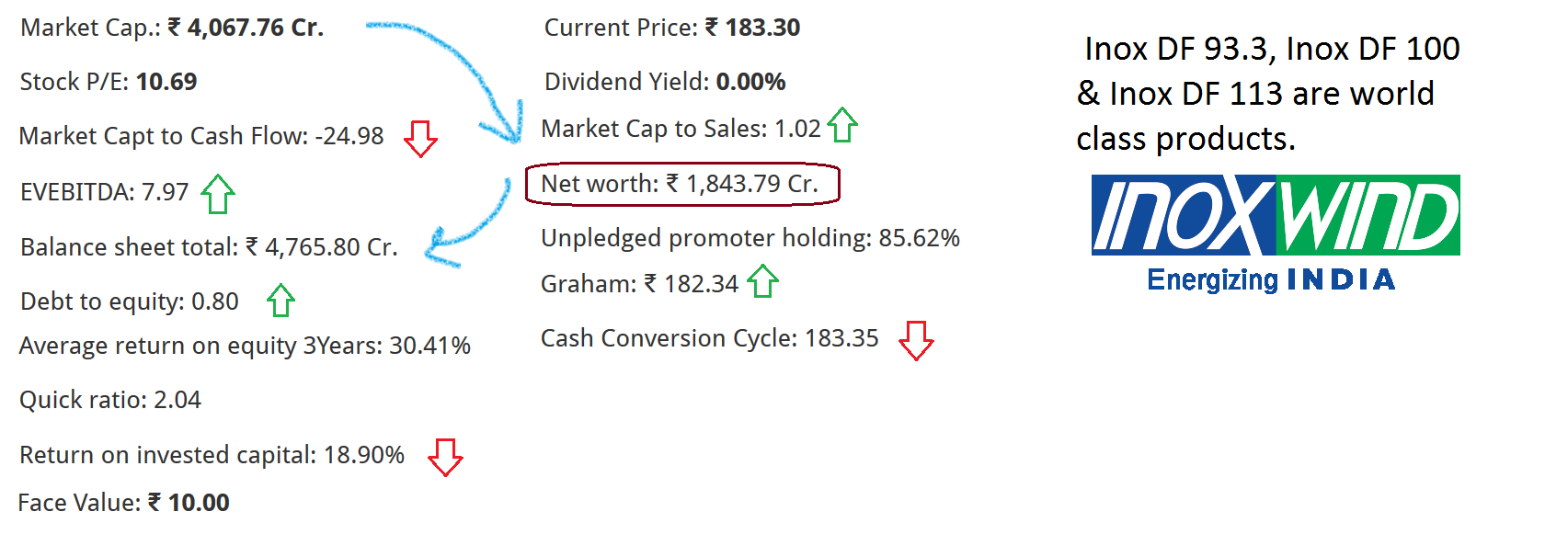

Debt and receivables have gone up significantly.

as well this quarter results were bad, fell from last year.

-Thanks,

Disclosure : Invested

Devansh Jain’s interview on the Inox group’s new venture Inox FMCG.

Is he getting replaced at Inox Wind? If not, then the divided attention is a concern.

One of his replies in the interview caught my attention…

When do you start looking at a new business from a group perspective?

Typically, we build a business when an existing business has matured, generating enough cash and there is no need to deploy that cash into that business.

In the case of INOX Wind, GFCL was generating a lot of cash from its chemical operations, so the intrinsic business of GFCL did not need this cash. So we thought of diversifying.

With carbon credits and all the writing on the wall, it was very clear: renewables is the future.

Inox Wind isn’t exactly a cash generating business. Also, short term debt is still a debt.

Disclosure: Invested.

He is not exactly saying that Inox Wind had generated enough cash.

Look.[quote=“VIFL, post:88, topic:28”]

In the case of INOX Wind, GFCL was generating a lot of cash from its chemical operations, so the intrinsic business of GFCL did not need this cash. So we thought of diversifying.

[/quote]

He was pointing out the Inox Wind Subsidiary GFHL, a chemical company which of course, have an outstanding business model.

This business (GFHL) is generating cash, not IW.

Anyway, Devansh Jain had created an excellent corpus with all of the INOX diversified business Leisure, Wind, Chemicals etc and now, FMGC.

We can argue all day what he meant. He is obviously entitled to venture into a new business, & has been looking do so for quite some time - this is from Nov 2015 on Forbes

He’s already looking for the next big opportunity. “I think Inox Wind

has reached a stage where it is very strong and the management team is

rock solid. It is virtually on autopilot. So now I am trying to figure

out what’s going to be the next avenue for me to build on,” he says.

As an investor of Inox Wind, I would prefer to hear more from the CEO & CFO of Inox Wind in the future, especially in the concalls. After all they are the ones having to deal with the major concerns of receivables, working capital cycle & short term debt.

The reason I’m cribbing about the short term debt is, a considerable chunk of the current order book are turnkey projects where the cash flows are likely to be lumpy.

1 Like

On the contrary, Inox Wind is the subsidiary of Gujarat Fluorochemicals Ltd.

I’m now a bit concerned, I assumed he would remain committed to IW till it resolves debt cycle issues. If you look at it the other way, GFL owns around 65% IW, and solely that is the promoter group. And the Inox Family owns only 60% of GFL. To summarize, Inox parent promoters own roughly 40% of IWind.

This leakage of ownership down the line reduces the ownership and commitment. I have reduced the investment in this due to this lack of response.

Inox Wind Consolidated Q2 Results & balance sheet. http://www.inoxwind.com/wp-content/uploads/2016/10/IWLCONSOLQ2.pdf

I don’t know how much IND-AS is responsible for it, but compared to the Balance sheet on 31st Mar 2016,

the receivables hasn’t gone down at all (It has in fact gone up by 4 Cr); Short term borrowing has gone up by a further 256 Cr. The earnings presentations claims “Significant traction seen in collection of Receivables in Q2”.

Earnings Presentation: http://www.moneycontrol.com/stocks/reports/inox-wind-earnings-presentation-5276821.html

A few things which caught my eye in the earnings presentation:

- Majority of new orders are backed by Letters of Credit (LCs)

- Order Book= 1,416 – 70 = 1,346 MW. 70 MW Order removed from Order Book due to financial issues at customer end. What’s the possibility of more such cancellations?

- Tower Manufacturing can be Outsourced depending on the location of the project being executed. Will the margins take a further hit in that case?

If someone listened to the concall, I request them to post an update.

1 Like

Notes from the Q2 FY17 Con-Call

The numbers for this quarter can be found here, so I will not go through them again. A lot of points were repeated from the previous call.

-

The tone of the call was extremely similar to the one that took place at the beginning of last month. The quarter was focused on bringing down the mismatch in the production of the turbine components. Going ahead, they will be providing synchronised components to all their customers. You can expect a lot of commissioning to take place in H2, with the wind market expected to be at 4-4.5GW this year. Devansh re-iterated the company’s aim of being net-debt free by the end of the year.

-

They maintain their annual guidance of supplying turbines worth 1GW.

-

Receivables are going down as new PPAs are being signed in Gujarat. Collections have more than doubled in Q2 over Q1, with H2 expected to be even stronger in terms of collections.

Age of receivables :- Out of the 2,400cr receivables, 2,000cr is under 6 months. -

IPO proceeds :- Part of it is still not utilised. A portion of this was raised to build a new plant for the production of nacelles, but debottlenecking at the existing facility at incremental capex should allow the capacity expansion to 1,400-1,500 MW. The other portion was meant to be used for certain project sites in Maharashtra and Gujarat, which haven’t been used yet due to policy issues in these states. This seems to be a prudent step taken by the management (and a temporary source of other income).

-

Wind auctions :- Expect the first tranche of the 1GW wind auctions to start by end of December.

-

Hybrid power :- The company plans to leverage its already set up wind infrastructure to add solar panels there and take advantage of the hybrid power policy. Since there is hardly a 2-3% margin in solar EPC work(management estimates), the value add will be in the cost saving of the infrastructure already in place, which should add 2-3% more to the margins.

We will need more clarifications on this, specially on its effects on the working capital. While Suzlon has officially entered into the solar space, this approach seems like a more sensible way to take advantage of the hype in solar energy, while not losing focus on its core competence. -

The company has started outsourcing the production of towers for supplying it in Andhra Pradesh. This will be a recurring theme for the company, as this component is difficult to transport over large distances and can be easily made by third party vendors. This is one reason for the increase in other expenses.

-

The land banks on the books are generally waste lands or other cheaply available land, purchased on an average of 1-2 lakh/MW. Private land is purchased only if the sales for that site are happening in the same year.

-

For a ballpark figure, you can assume that it takes 20 days for the turbine components to reach the sites in the southern states of India.

-

My takeaways :- The management refused to give a revenue guidance for the year, which makes me think that the execution of the stranded towers in Gujarat will significantly add to the execution numbers, while obviously contributing <6cr per MW. I certainly expect this year to be a consolidation period wherein they get their working capital in order to improve sales going ahead. We can perhaps expect better sales in H2, but the year as a whole will see a de-growth for the company, with the profits looking a lot lower due to the increase in fixed costs, while the volumes have not gone up. I am still bullish on this company being one of the best bets in the renewable energy space in the longer run, but changing policies can always be a spoiler.

2 Likes

The stock getting to a TP of 400+ is unlikely in the near to medium term. I’ll be more than glad if I’m proved wrong.

Let me rephrase. The stock doesn’t deserve to trade at 400+ levels in the near to medium term.

1 Like

Can anyone please provide access to conference call notes. Would love to read them!

Thanks,

Navneet

Lets watch how the story unfolds. Its a really futuristic and trending business, its just the cash from sales thats not coming in

Management had been claiming for long to reduce ‘receivable days’ however nothing visible so far… Hope H2 current FY we see some improvement there …

1 Like

INOX group sells its wind farming business in four states .

http://m.thehindubusinessline.com/companies/inox-exits-wind-farming/article9576032.ece

This is from Analyst call transcript of INOX WIND

Suyesh Kapoor: Sir, my first question is regarding this article which has come in ET Now a few days before regarding Mr. Narain Karthikeyan;he will invest Rs. 1,200 crores in Inox Wind Farm. So if you can please give you views, is it is possible, if it is legally permitted to give your view, if you can please give your view, sir?

Devansh Jain: I am sorry, we do not comment on market rumors. And in any case the supposed article spoke about Inox Renewables;the company we are dealing with over here is Inox Wind. So honestly,we have no comments on Inox Renewables.

I guess this may not have any impact on INOX Wind

Well there is nothing much in detail on the IRL website. The following article talks about the group wanting to focus on the “core business, including wind turbine manufacturing”

Although, not very sure what effect it would have on Inox Wind’s stock performance. As of now it is up close to 5%