CRISIL has no new information, their rating has been revised on the basis of the same March 31 numbers.I am not a fan of general investing jargon, like value trap or growth trap since it makes for some lazy generalising. This is a 25% RoE business where EPS grew 50% last year and will grow atleast 25% this year. There is no conceivable case for a single digit P/E multiple here

See CRISIL report below

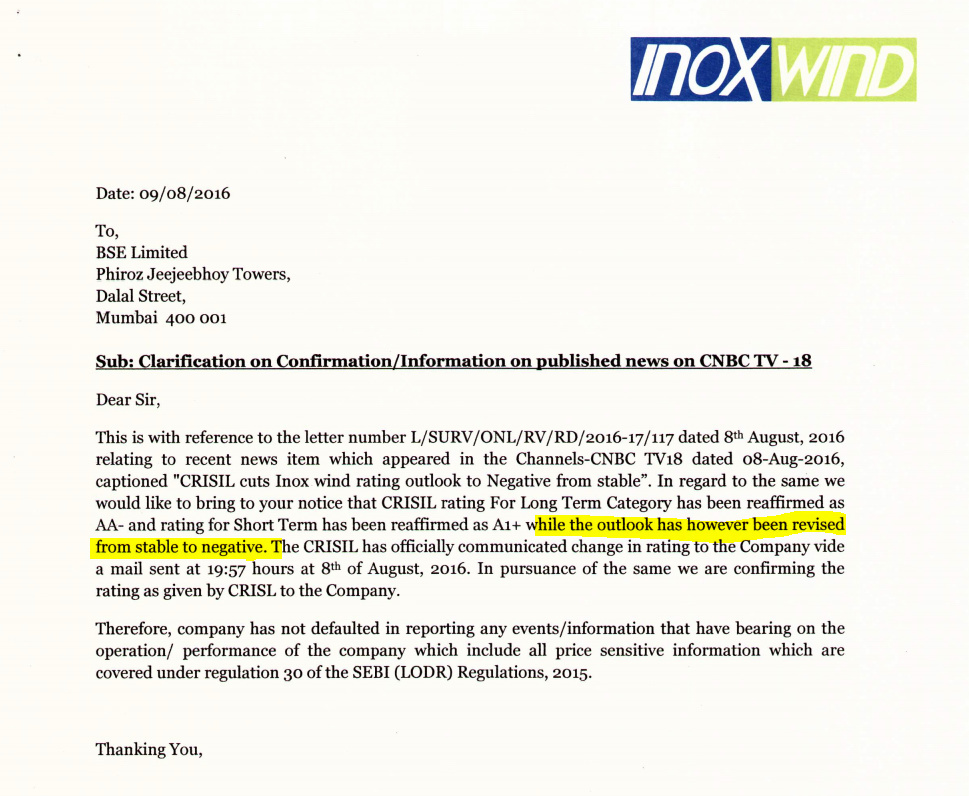

CRISIL has revised its outlook on the long-term bank facilities of Inox Wind Limited (IWL) to ‘Negative’ from ‘Stable’ and reaffirmed the ‘CRISIL AA-’ rating. The ‘CRISIL A1+’ rating on the company’s short-term bank loan facilities and commercial paper programme has also been reaffirmed.

The outlook revision reflects CRISIL’s belief that IWL’s credit risk profile may be constrained over the medium term because of its large receivables. Contrary to CRISIL’s earlier expectation of a decline in the receivables because of increase in equipment supply orders and alignment of manufacturing capacity of various components, the receivables increased to 148 days as on March 31, 2016, from 140 days as on March 31, 2015. This is because some projects were stuck on account of pending commissioning or power purchase agreements (PPAs), and manufacturing capacity of components was not fully aligned. IWL expects resolution of the pending projects and the pace of receivables collection to improve in the next few months. The inventory and receivables will also improve once the full benefit of the Madhya Pradesh plant, commissioned in November 2015, starts accruing. However, most of the orders are expected to be turnkey projects, which entail a longer collection cycle than equipment supply orders. Time-bound correction in the receivables collection cycle will remain a key monitorable.

The ratings continue to reflect IWL’s healthy market position, strong operating efficiency, and support from parent, Gujarat Fluorochemicals Ltd (GFL; ‘CRISIL AA/Stable/CRISIL A1+’). These strengths are partially offset by the company’s large working capital requirement, and susceptibility to technological and regulatory changes.

IWL has benefited from healthy demand for renewable energy, and is one of the leading wind energy equipment manufacturers in India. It had orders of 1104 megawatt (MW) as on March 31, 2016, against just 300 MW as on March 31, 2014. The company has sourced technology from AMSC Windtech, Austria, which has over 15 gigawatts (GW) of wind capacity globally. IWL’s considerable inventory of wind sites for over 5000 MW provides it with a competitive advantage in securing and executing large orders.

IWL’s revenue grew 2.8 times over the three years through fiscal 2016, and its healthy order book provides revenue visibility over the medium term. The company reported average return on capital employed (RoCE) of 25.3% and operating margin of 14.7% in the three years through fiscal 2016. Its market position will continue to be supported by its healthy order book, strong technology tie-ups, and robust execution capability.

GFL holds 63% equity stake in IWL, and the company is central to the parent’s growth plans in the wind energy business and has grown rapidly over the past three years. CRISIL believes GFL will continue to extend timely support to IWL, if required.

IWL’s operations are working capital intensive because of substantial receivables, driven by the large proportion of turnkey projects in its order book. Delays in commissioning or signing of PPAs have also resulted in a long collection cycle. Although the stretched working capital cycle led to increase in debt to Rs 14.7 billion as on March 31, 2016, from Rs 8.7 billion a year earlier, healthy cash accrual supports the company’s debt protection metrics and gearing. IWL had cash and equivalent of Rs 4.8 billion as on March 31, 2016, which supports liquidity. Its interest coverage and net cash accrual to total debt ratios were 8 times and 0.3 time, respectively, for fiscal 2016, while gearing weakened to 0.8 time as on March 31, 2016, from 0.6 time as on March 31, 2015. The working capital cycle could improve in fiscal 2017 on account of resolution of pending projects and full benefits of alignment of manufacturing capacity. The pace and extent of correction in the working capital cycle will be key rating sensitivity factors.

IWL is susceptible to technological changes in the wind energy sector, even though its strong relationship with AMSC Windtech helps mitigate the risk. Moreover, wind power generation is subject to complex regulations and is supervised by multiple regulatory authorities. Any adverse impact of regulatory change, such as lowering of feed-in tariffs or withdrawal of benefits to wind power producers, may affect capacity addition in the industry, and hence, IWL’s operations.

For arriving at the ratings, CRISIL has combined the business and financial risk profiles of IWL and its subsidiaries.

Outlook: Negative

CRISIL believes IWL’s working capital cycle will remain stretched, leading to large debt and risk of non-recovery of certain receivables over the near term. Its cash and cash equivalent will support liquidity. The ratings may be downgraded if the working capital cycle does not correct, or if the company’s operating performance declines considerably, or if support from GFL reduces. The outlook may be revised to ‘Stable’ if the operating performance and working capital cycle improve on a sustainable basis.