Management answers some issues raised in the report namely competition, customers, warranty claims etc here–

you did a better job I wish you started a new post on INOX than continue what I just started as a formality during the time of IPO. I feel your analysis is complete and deserves a standing ovation. I feel that financially also(after few years), apart for the story which you have at length covered, the stock can do very well farting heavy dividends on the way for value investors like us.

Motilal Oswal has come out with a research report on Inox Wind.

Conference Call - from Capital Markets

Inox Wind

Ebidta margins excluding forex movements stood at 14.9%

The company held its conference call on 27th July’15 and was addressed by Deepak Asher, Director and Mr. Devansh Jain Executive Director

Key Highlights

• Sales volume including equipment and turnkey supply, in Q1 FY’16 stood at 120 MW as compared to about 66 MW YoY. Commissioning however stood at 78 MW as compared to NIL for Q1 FY’15. There are about 200 MW of wind turbines yet to commission and will be commissioned during rest of FY’16.

• Of the total revenue of Rs 635.83 crore for Q1 FY’16, about 92% of revenue came from sale of products and rest from sale of services, as compared to the entire revenue of Q1 FY’15 of about Rs 304.37 crore from sale of products.

• As per the management, Ebidta margin has come down from about 15.5% in Q1 FY’15 to about 13.6% in Q1 FY’16, primarily due to forex movements ie in Euro currency. There was a forex loss of about Rs 8.2 crore, as compared to about Rs 4 crore gains for Q1 FY’15. Excluding forex movements, Ebidta margin for Q1 FY’16 stood at 14.9% as compared to 14.1% for Q1 FY’15. The margins have improved on account of better economies of scale and operating leverage. Margins are expected to improve further as per the management.

• Total order book as on June’15 stood at 1220 MW which is to be executed in 12-15 months. About 162 MW of orders added in June’15 quarter as compared to execution of about 120 MW of orders in June’15 quarter. Of the total 1200 MW orders, bout 800 MW are binding government contracts (firm commitment).

• About 97% of total order book are third party orders and are pretty diversified and with reputed clients including Green infra, Tata Power Renewable, Bhilwara Energy, Renew Wind Energy, Hero Future Energy, NHPC, RITES, Continuum etc. Large enquiries of orders are coming and management expects further orders to come in as FY’16 progresses.

• About 60% of total order book is Turnkey, while rest is Equipment sale orders. State wise, about 39% of orders are to be executed in Rajasthan, 47% in Madhya Pradesh and around 14% in Gujarat.

• The company has sufficient land bank for installation of aggregate capacity of more than 4500 MW as on June’15. The company is in process of increasing land bank in existing States as well as new States like Tamil Nadu.

• The company’s proposed Blade plant in MP is ready to commence operations as on Aug’15. This plant is amongst the largest in Asia and this will double the overall installed capacity of Blades for the company to about 800 blades.

• In terms of Technology Upgradation, the company has launched 100 Rotor dia blade from earlier 93 Rotor dia blade. This increases the overall generation capacity, reduces costs of energy and would give further better margins to the company.

• Government’s thrust on Renewable energy continues to remain. RBI notified Renewable energy lending under Priority sector in Q4 FY’15. Government aims to add about 10 GW of power capacity every year through wind sector.

• As per the management Lot of action is seen from States like MP, AP, and Gujarat in terms of signing the PPA’s from wind power while Rajasthan has slowed down. More States are expected to participate.

• As per Crisil, the wind power equipment supply market is expected to be about 3600 MW in FY’16 and about 4100 MW in FY’17.

• While Solar power is catching up faster, returns from wind is always higher by 15-20% compared to solar. Further, land acquisition is a big issue in Solar, as solar needs much more land compared to wind.

• Globally competitive bidding has failed across the boards for wind power projects. As per the management, if competitive bids do take place in India, it will be more beneficial to players like Inox Wind.

Disc: Not Invested

Call add by Deepak Asher,Director &Mr.Devansh Jain ED.Highlights Capital Mkt

Sales volume including equipment and turnkey supply, in Q2 FY’16 stood at 212 MW as compared to about 114 MW YoY. Commissioning however stood at 140 MW as compared to 30 MW for Q2 FY’15. There are about 160 MW of wind turbines yet to commissioned and will be commissioned during rest of FY’16.For 6 months ended Sep’15, the sales volume including equipment and turnkey supply stood at 332 MW, an increase of about 84% on YoY basis. For 6 months ended Sep’15, commissioning stood at 218 MW an increase of about 627% on YoY basis.Of the total revenue of Rs 1008.2 crore for Sep’15 quarter, about 92% of revenue came from sale of products and rest from sale of services, as compared to the entire revenue of Q1 FY’15 of about Rs 304.37 crore from sale of products.

During Sep’15 quarter, about Rs 194 MW of orders were added as compared to about 212 MW of orders being executed. About 71% of total order book of 1202 MW is from Turnkey and rest from Equipment supply. About 39.1% of order book is from MP, about 38.3% from Rajasthan, 21.8% from Gujarat and rest from Andhra Pradesh. The order book has an execution time frame of about 12-15 months.The company has sufficient land bank of capacity more than 5000 MW as on Sep’15. The company is in process of increasing land bank in existing States as well as new States like Tamil Nadu. As per the management lot of action is seen from States like MP, AP, and Gujarat in terms of signing the PPA’s from wind power while Rajasthan has slowed down. More States are expected to participate.

Orders are from clienteles such as Tata Power, Sembcorp Green infra, Bhilwara energy, CESC, Renew Wind Energy, Ostro Energy, Continuum Wind and PSUs such as GMDC, NHPC, RITES, GACL etc.The Blade plant at MP got commissioned in Sep’15 quarter. The Tower plant in MP is on track and will get commission in H2 of FY’16. The new 100 meter Rotors have higher efficiency and higher energy yields which will result in higher margins for the company. 113 meter turbines which will be launched in H2 FY’16 will also result in higher margins for the company.Ebidta margin for Sep’15 quarter stood at 13.6% as compared to 16% for Sep’14 quarter. Excluding forex fluctuations on like to like basis, Ebidta margins stood at 14.1% as against 15.3% for Sep’14. Lower margins were on account of higher employee costs and site related activities for future upcoming facilities. As per the management, margins are set to improve only from here on.Net working capital days fell to about 148 days as compared to 169 days as on June’15. Lower inventory levels and receivable days together with steady order intake, helped in improvement in working capital days.Government’s thrust on Renewable energy continues to remain. RBI notified Renewable energy lending under Priority sector in end of FY’15. Government aims to add about 10 GW of power capacity every year through wind sector.Overall management continues to remain optimistic for rest of FY’16.

1 Like

An article relevant for Renewable energy companies:

Google steps up its purchases of renewable energy:

http://www.ft.com/cms/s/0/68e01302-99b2-11e5-9228-87e603d47bdc.html

Re: Inox Wind – Concall Update

Technology tie-up with AMSC – Key Features

• Company got license to manufacture Electrical Control System (ECS) indigenously – Exclusive License from AMSC to manufacture ECS in India. Will pay one time license fee of $12mn to AMSC which will be capitalized. Fees will be paid in phased manner over next 1 year as the technology gets transferred. Further, Company will have to incur Rs 2-3cr capex to setup assembly unit at its existing facilities.

• Long term supply agreement of ECS from AMSC to secure sourcing of the equipment – Here AMSC will supply 50% of the ECS requirement of Inox over next 5-6 years at a fixed price (balance will be manufactured by Inox in India). As per AMSC’s press release, such agreement is valued at around $210mn (including license fees) over the agreement period – around $40mn annually (assuming 5yr agreement)

• Collaboration for 3MW turbine technology

Benefits of ESC tie-up

• Company was dependent on AMSC for ECS supply which was seen as a risk given the questionable financial health of AMSC. With this deal, company not only secured the supply of key component but also secured technology to manufacture it indigenously.

• Company will save significant cost both from cost of ECS as well as logistics/supply chain perspective

• Mgmt said ECS cost is around 8-10% of the imported cost of turbine, which is around 35% of total wind turbine cost. So cost of ECS is around 2.8-3.5% of total wind turbine cost.

• Mgmt did not divulge cost savings but the rough guesstimate would be around 50bps to 75bps/MW savings can be achievable (of 2.8-3.5% cost – 50% will remain unchanged due to imports, benefit will come in balance 50% indigenous ECS - cost saving, logistics savings, WC savings)

Benefits of 3MW turbine technology

• Mgmt said India market is not ready right now for 3MW turbine due to various factors including logistics

• However, company has secured technology to be future ready as and when India is ready for 3MW

• Will be able to roll out in next 18-24 months

Other aspects and Concerns addressed:

• On provisioning for spares and warranty: Management indicated that for outsourced components they have back to back guarantee with the suppliers. For indigenous components which company manufactures, company has insured all products for any mfg defects. Still against industry practice of providing provision every year.

• On AMSC’s health: Securing technology for key component and long term agreement, clears some air around the same.

Disclosure: Not invested

2 Likes

Is there an updated view from @varadharajanr and @Mahesh given the steep correction? Trades at 13x NTM P/E vs 17x for Suzlon.

1 Like

No significant updates except that the recent strong correction in good quality mid/small cap stocks might make it even more of a long term story of say 3- 4 years than 2 years that I thought before. Also majority of the peers are getting aggressive on solar front while Inox seems to be sticking to its core which might be perceived negative by the market for the time being.

Dicl. - Invested. Have sold some quantity over last few weeks as a portfolio reshuffling exercise and nothing else. Company forms ~3 % of family portfolio.

3 Likes

CONFERENCE CALL - from Capital Markets

Inox Wind

Expects pick up in order inflow in Q4FY16

Inox Wind held a conference call on Feb 9, 2016. In the conference call the company was represented by Deepak Ashar, Director (Corporate Finance).

Key takeaways of the call

Order intake in Q3FY16 is about 110 MW. So order book of the company as end of December 31, 2015 was 1146 MW. Current order book will be executed in next 12-15 months. Of the order book about 40% is from the state of MP, 20% from Rajasthan, 20% from Gujarat and rest from AP.

It also sees significant traction in order inflow during the coming quarter. The government of India’s thrust on the development of renewable sources of energy is emphasized by the revised tariff policy which levies no inter-state transmission charges and losses for power from renewable sources and introduces the Renewable Generator Obligation. With a supportive regulatory framework, India’s wind market is expected to be one of the world’s fastest growing.

With tariff policy coming for expiry in March 2016 for about 3 states, the clients hold back order finalization for want of clarity. Now with lot of clarity emerging of what the new tariff policy would be, the next couple of weeks in Q4FY16 will see strong order inflow.

Sales for the quarter and nine month ended December 2015 stood at 166 MW and 498 MW respectively. Minor procedural delays affected volumes for the quarter and the company expects significant pickup in sales going forward. Some components struck in customs for 7-10 days without clearance. So manufacturing, despatch and billing of about 80 MW WTG which was scheduled and site is ready for installation got shifted to next quarter. The impact of delay on top-line of Q3FY16 is about Rs 247 crore as certain part of the turbine could not be billed. Its impact also felt in the profitability of the company.

Q3FY16 has been a momentous quarter for the company with several developments that offer the company substantial long term benefits. Foremost among them is the licensing agreement with AMSC that assures continual supply and offers security in sourcing of one of the critical components of a Wind Turbine Generator.

The blade manufacturing plant (of 800 MW capacity) at the company’s world-class integrated manufacturing facility in Madhya Pradesh was commissioned during Q3FY16.

The company has also further commissioned 400 MW common infrastructure facilities at Rojmal, Gujarat In January 2016. The company has also commissioned the common power evacuation facilities (200 MW) at its Nipaniya site in Madhya Pradesh. The commissioning of the common infra facilities at Lahori (200 MW+ at Madhya Pradesh) is also ready.

With significant ramp-up in execution activities going forward, the company expect growth to accelerate over the course of the remaining year.

The company has strong land bank for wind installations and the company has acquired land in AP for 4500 MW of WTG installations.

Inox Wind continues to strengthen its position and increase market share across IPPs, PSUs, Utilities, corporate and retail customers.

Renegotiated rates for components kick started in Q3FY16 onwards and the lower steel prices, which witnessed a weighted average prices was lower by 20-25% has kept the material cost lower. Higher other expenses is largely due to booking of new plant commissioning.

Q4FY16 margin will have the benefit of lower material cost, operating leverage and better mix.

The market could see 3000 MW of WTG commissioning in 2015-16 and the market may grow by 20-30% next fiscal depending on policy environ

2 Likes

Below are important key takeaways…Q4 will be a good one for the company. Although wind business is very much dependent on the govt policies, I think it will do well. What separates Inox wind from competition is its strong execution and strong balance sheet. Its a delight to see how they have scaled up and managed the finances well.

Discl- Small position in Gujarat Fluoro

2 Likes

I think what company has achieved in 5 years is remarkable. Of course, high receivables are there, but that’s the nature of the business. Also, government has focus on renewable energy and also accelerated depreciation benefit has been restored. I think this company has a good future.

Disc : Invested in Guj Fluoro.

2 Likes

Why its falling suddenly >

@brajeshrawat

Despite good result the price has fallen due to sharp increase in short term borrowings and also spurt in debtor days.The management came out with clarification after market hours which seems to be fair.

To me it is a great opportunity to buy.Views from experts please.

Source-Interview to CNBC-TV18 by Devansh Jain,Whole time Director.

Dis-Invested@Rs.280/- small quantity.

Not sure if this story (several weeks old) is true, but if it is, it would explain the negative sentiment.

http://www.centralchronicle.com/inferior-technology-turbines-burst-into-fire.html

1 Like

Exactly, that’s the nature of the business. How much are we going to punish the stock? Director Devansh Jain seems to be a young, dynamic, up-to-date (with latest technology and information) person.

Govt. targets wind energy generation capacity of 60GW by 2022 from 26.7 GW on 31st march 2016. As per a report, nearly 4.5 GW will be added in 2016-17, most of which will be supplied by top 3 wind power cos. (inox wind is one of them).

Wind power has become competitive with solar and thermal at 4.x Rs. per unit (kWh) . So, it doesn’t require subsidies anymore.

Inox wind has emerged as the leader in whichever state it has entered. And now, it is entering southern states as well. It seems worth taking a bet on this one.

Disc: invested recently and may add more.

Short term borrowings spike by 630 odd crores and only things which catches attention here…

Company’s wholly owned subsidiary IWISL has acquired 100% equity shares of VEGPL and SWKPL in last quarter of 2015-16.

Possibly borrowings has been used for this purpose…

More over they have been able to grow eps in organically only

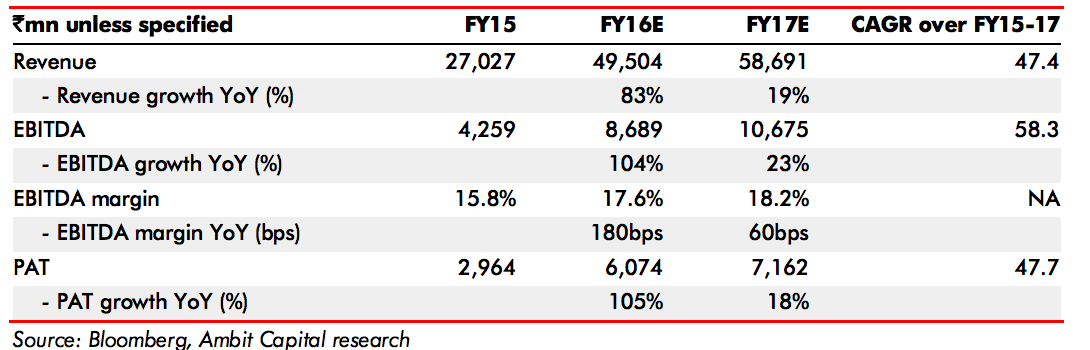

Ambit had showed worries regarding Inox Wind maintaining their CAGR in both revenue and income. Looks like Inox had managed to stay up. ~55%+ CAGR

And the market price went down solely because of the annual results, which was obviously showing YoY improvement ( with all the issues still persistent - High DSO, No Warranty Provisions etc ! ).

Adjusted heavily during May 5 - 6th:

Regarding the fire incident, I recall Devesh Jain telling that the company had zero claims during the first three years of its third party business ( FY13-FY16 ). I do not know if this was an actual incident. I couldn’t find any article anywhere except the common plagiarized content:

-

Inferior technology turbines burst into fire | Wind Energy News

*http://www.patrikagroup.in/nation/madhya-pradesh/inferior-technology-turbines-burst-into-fire/

*http://www.centralchronicle.com/inferior-technology-turbines-burst-into-fire.html

As an ex-blogger, I have serious suspicion regarding the authenticity of this news! In fact, If somebody sold shares due to this, I have got that much more interest in buying Inox Wind!

When the arguments are made against promoters who have been there for 50+ years, and the next generation well entrenched into the businesses, I do not know how else they can be invested in the business than having 85% of the MCap. ![]()

They have got zero surplus capacity year on year for the last half decade, Have acquired lots of land in over 5 states ( even in AP ). I would say that they are pushing their foot down on the pedal!

Disclosure: No holdings.

1 Like

Inox Wind is facing a lot of head wind due to strong competition from Gamesha and Suzlon which was missing a few years ago.

Now that Suzlon is well capitalized and Gamesha has got its act together INOX WIND is facing the heat,

During April-June Inox has reported only 50 MW of order win as against Gamesha winning 460 MW.

While Suzlon and Gamesha have increased their market share in 2015-16 Inox has just managed to hold onto its share.

The competition has intensified within the wind players and is also facing competition from Solar.

Disc: Exited at a loss by switching to Ujjivan

Suzlon is not well capitalized.

- They have severely high debts.

- Tanti still believes the company will grow annually at post 2010 pace for next 4 years.

- I read an article in Forbes, in which he is clearly trying to navigate himself out of the troubled areas. Specifically, they are hoping to get more of those IPP projects, which has lesser margin. INOX clearly has well diversified clientele.

Another point to be noted:

- Wind energy orderbook gets filled in a choppy manner.

- Gamesa contracts were signed in Q2 2016, it is just that they are getting commisioned now. Revenue would’ve been recognized partially in Q4 at the least by them.