Regarding the Video content: Below are some interesting posts related to Video content growth and its dominance in Ad share.

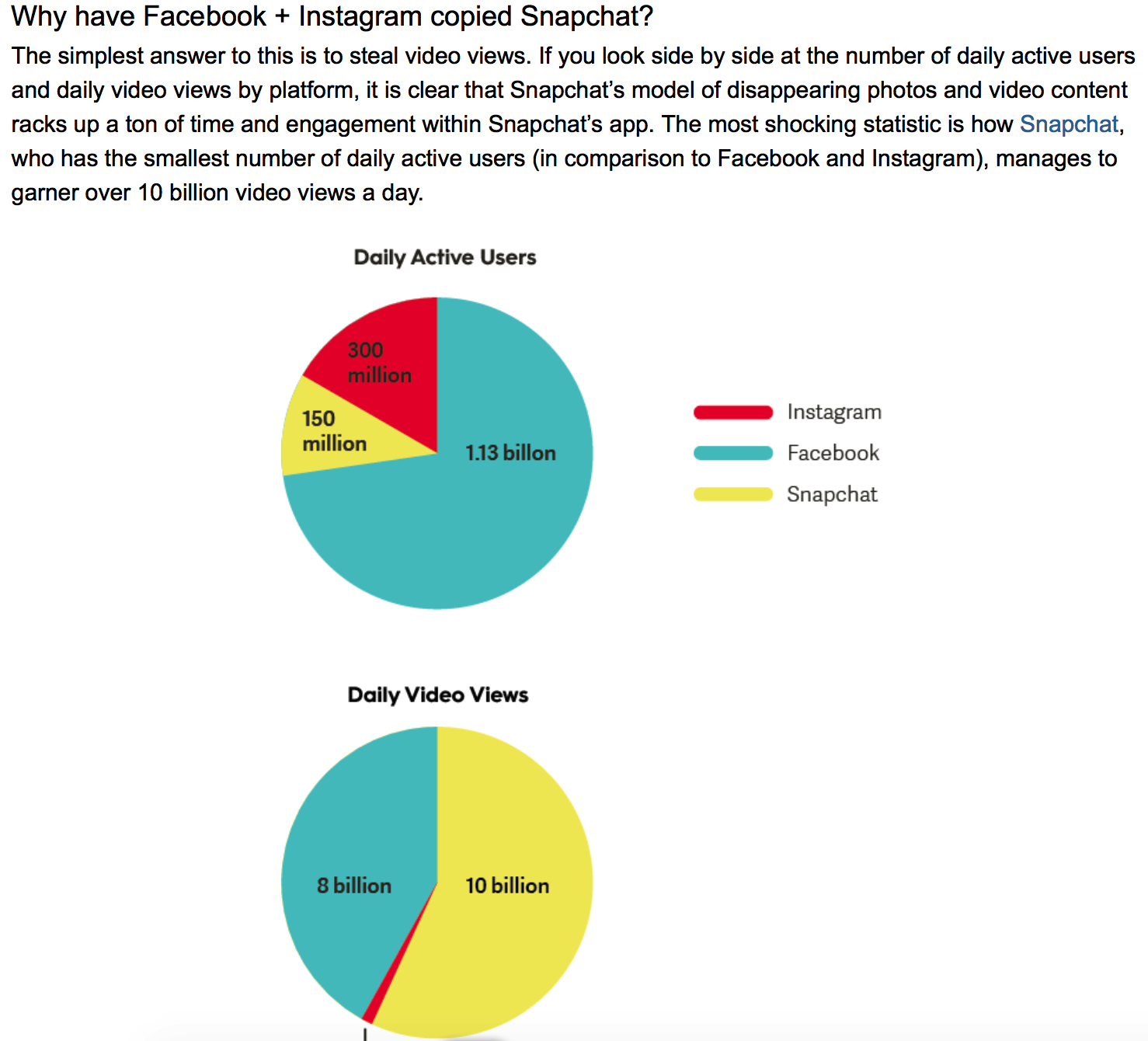

It’s no secret that video content is on the rise. By 2019, video content will be the driving factor behind 85% of search traffic in the US. Whether it’s Snapchat, Instagram, or Facebook, video content on social media is what marketers need to focus on.

“Brands should anticipate their audience to expect them to offer video content. Those who don’t will be left behind, with consumers opting to engage with brands that tailor their content to consumer preferences. In addition, marketers will be creating more video ads, especially on Facebook and Instagram, as they yield more engagement and higher click through rates than traditional static ads.”

Facebook Watch to overtake Youtube: Only time will tell it, it won’t be cakewalk for Facebook when the competition is with Google, same things were touted when Facebook started giving ads that the google ads would dry up, but that didn’t happen.

As the trends show’s video is the new focus area and Irrespective of the technology to deliver the video content will be served more and more, also as the content creation will get fragmented better it gets for content aggregators, in the end, content owners are the king.

Regarding the Monetization of content, it seems obvious that per view/click monetization will go down with respect to the amount of content creation or it won’t be applicable as the monetization policies will keep getting enhanced/sharpend as per the focus needed from Advertisers also as per the variables like Ad blocker, Type of video(all the genres), Viewer type (Age, gender, class, location, spending capability), total number of view on video, length of video, and ethnicity of content creator and so on.

Rest I think its futile exercise to predict the exact monetization model due to so many variable, but I feel that older content which already has mass appeal should be valued higher in Ad serving business, as it can instantly generate the views.

For Example: in the continuous feed of new videos, I would be reluctant to risk my time on new video rather I would definitely watch a clip from Sholay or any known movie, as I already have an association with it and almost surety of getting entertained.

Also, there is Bias at play “Old is Gold” even in normal day to day things people are valuing older things as precious, even in naming, the old Great Great Grand Father ![]() although its certain that ALL the forefathers were not great but we just call them Great, such a bias won’t go away easily.

although its certain that ALL the forefathers were not great but we just call them Great, such a bias won’t go away easily.