We have been witness to the huge explosion in mobile and broadband data consumption in India. There are different entities participating in this digital media ecosystem - from Content Creators, Content Aggregators, Multi Channel Networks (MCN), Over-the-Top (OTT) and Video Platforms, Media buyers & planners, Advertisers, and more.

Apart from Shemaroo, Balaji Telefilms there aren’t too many listed opportunities that benefit from this space. Recently Silly Monks listed on NSE emerge. DRHP. The opportunity being huge, there should be more value creation opportunities down the line. At the same time, I felt we do not understand this space well enough to do justice to even the listed opportunities - motivation for this exercise.

Leaving aside the well known Bollywood/Movies Content Creators and Aggregators, here’s a starting list of new players in the digital eco-system. We will cover each category in separate sections (if needed) later in this Industry mapping exercise.

A. Content Creators - (primarily videos/web series) - Alt Balaji, TVF, AIB, Scoop Whoop, Arre - apart from Alt Balaji which started a OTT subscription service, most others came into prominence through YouTube/Monetisation

B. Multi Channel Networks (MCN) - (primarily Aggregators on YouTube) - Culture Machine, Nirvana Digital, Ping, Qyuki, Fame, One Digital, Whacked Out Media, Silly Monks. The first 4 have 80-100 Mn views per month and have taken the PE funding route between ~$10-20 Mn. Silly Monks recently listed on NSE Emerge. (Disney had acquired MCN Maker Studios in 2014 for $675 Mn (380 Mn subs, $5.5 Bn monthly views) that has seen troubled times

C. Subscription driven Video OTT Platforms (SVOD) - Amazon Prime, Netflix, Hooq, Sun Nxt, Alt Balaji

D. Fremium/Advertising driven Video OTT Platforms (AVOD) - Voot, OZee, YouTube, HotStar, Sony Liv, Viu, Ditto TV, Silly Monks

To understand value creation opportunities in the industry, think we need to understand how these players make money. A quick glance would tell us that although a few (with deep pockets) have chosen subscription driven models, most owe their existence and survive on advertisement driven models. While we all know digital consumption has forged ahead by leaps and bounds in 2017, digital advertising though growing at a fast pace, has not kept pace with this consumption explosion.

Some answers we are looking for, to get an initial grip on the Digital Advertising Industry:

- Total Advertising Market Size in India?

- Advertising Spends on different Media - TV, Print, Digital, Radio?

- Which Sectors are the bigger spenders on Digital Media?

- What kind of Advertising strategies are being used by them? Push vs Pull?

- For digital advertising to grow rapidly, 3rd party measurement metrics will be essential. What kind of Measurement Metrics are initiated for Digital Advertising? Is BARC Ekam going to be the standard?

- In this era of rapid technological changes, how is the Advertising Industry likely to grow? If Digital Media share has to grow, it has take away some share from both TV and Print? How big or small is that change?

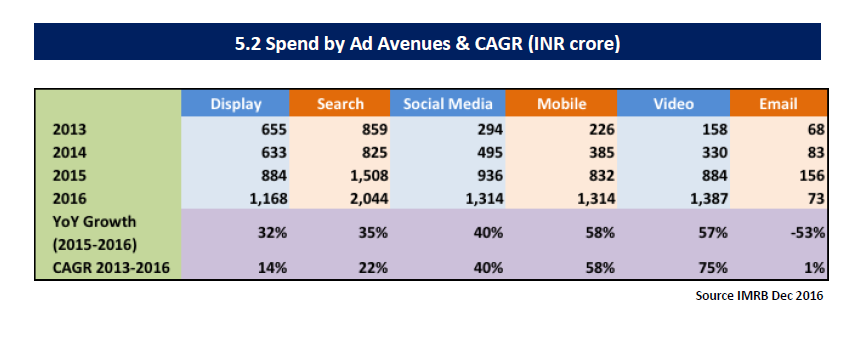

- Digital Media spend in different formats - Search, Social, Video, Display?

- Since most of search and social media spends are NOT shared with content publishers/owners, what is the Addressable Digital Media spend, really?

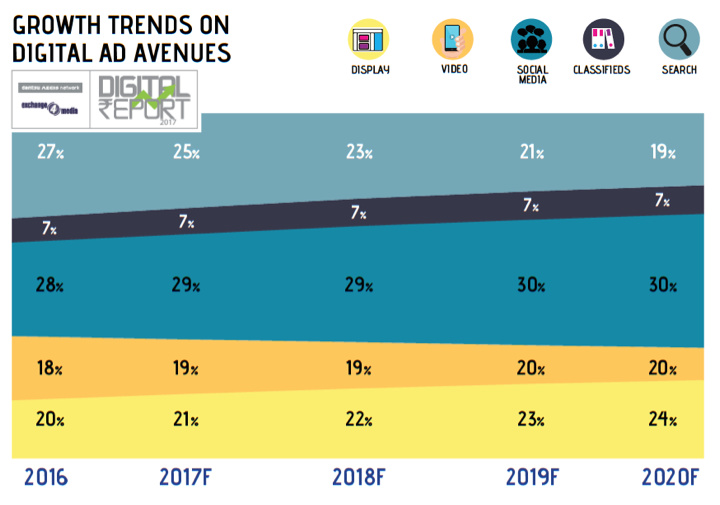

- What are the growth trends for Digital Media spends in future - Search, Social, Video, Display? Is display spend going to drastically go down like in Global trends? Will Video spend grow very fast?

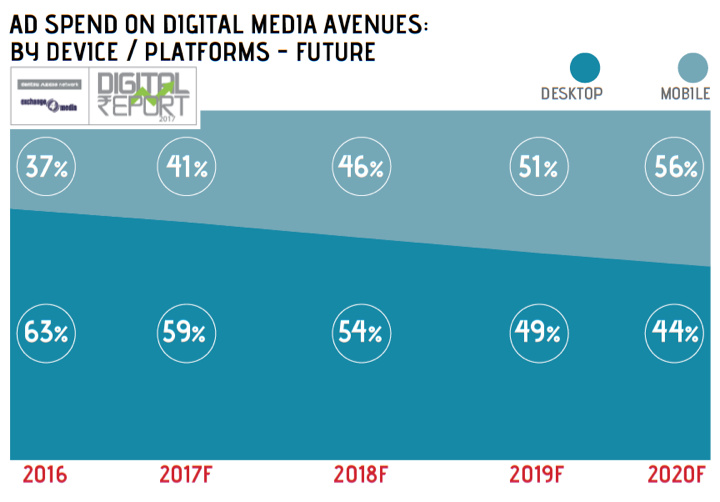

- What is the share of Digital spend between Mobiles and Desktops today? Since India data growth is being propelled hugely by Mobiles, how much of a share is Mobile likely to take away in future?

- How stable is YouTube Monetisation rates? Are there other issues? YouTube Monetisation (55% to content publisher) rates have fallen from $150 for 1 Lakh views (in India) to $100, to $22 after some major brands pulled out of YouTube (on brand ads getting served alongside objectionable content) and also demonetisation effect. Another major brand pullout in Nov 2017 It has since recovered to $33. YouTube undertook major content clean-up exercise and recently introduced changes to Monetisation Eligibility criteria

- Now that Facebook Watch (launched in US) is being beta-tested in India (reportedly offering similar 55% share like YouTube to subscribed Content Publishers), how does that change the dynamics? Does it expand the market or more likely take away share from YouTube? How does it affect existing publishers dependent heavily on YouTube monetisation? How does it affect OTT players?

- Regional Content prominence versus Hindi Content?

- Direct Channels versus Programmatic Advertising share - buying on real-time bidding basis which allows brands to buy and sell inventory on per impression basis in real-time, target more effectively and improve RoI? What’s the Programmatic Advertising uptake in India?

- Digital ad Networks and Ad Exchanges becoming the norm in 5 years?

- Flipkart like Commerce Advertising? Reportedly 500 Advertisers have created at least 1 campaign in 2016 on Flipkart. Flipkart Advertisements how they fared in 2016

It makes sense therefore to start with a look at the digital advertising landscape first, before moving on to identifying the issues, challenges and opportunities facing the industry players. With help from VP Community media specialists (please put your hands up) – we aim to refine this progressively, and get a better grip on the myriad moving parts. (Please help correct mistakes).

References:

- Digital Advertising in India 2016 – Dentsu Aegis, Exchange4Media

- Media for the Masses - KPMG FICCI Frames

- Global Advertising Forecast - MAGNA

- Digital Advertising India Insights - Adobe

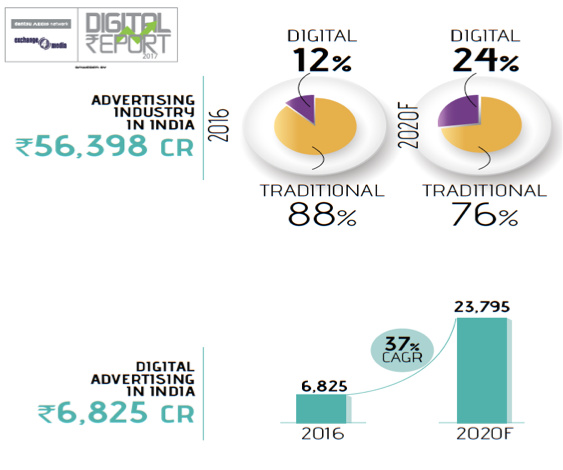

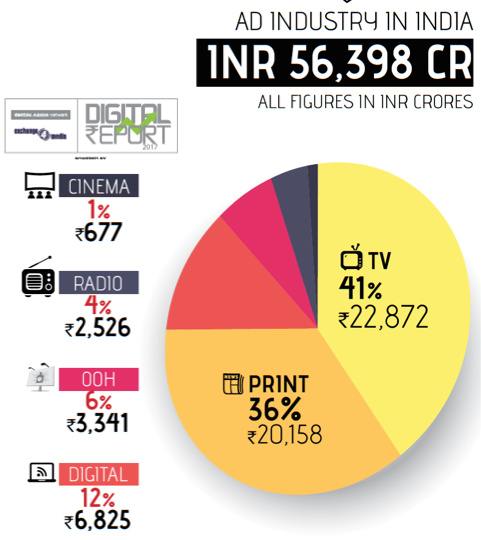

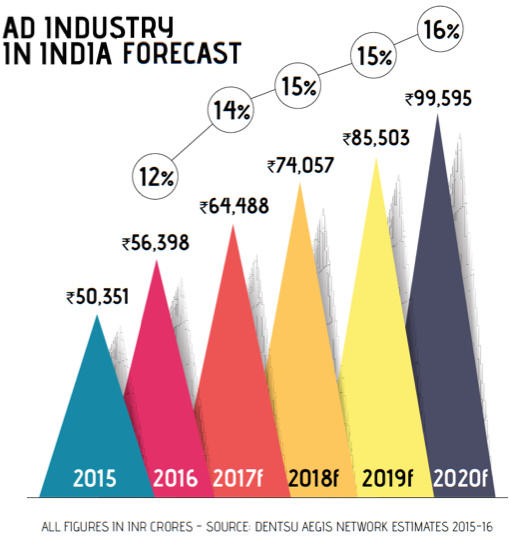

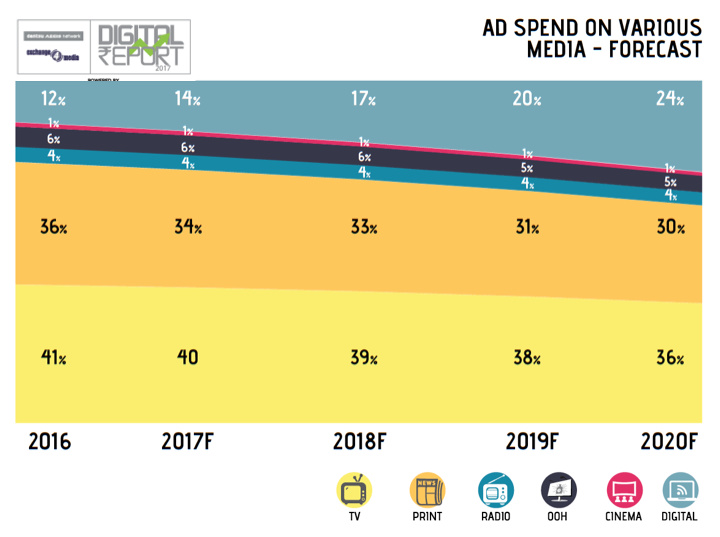

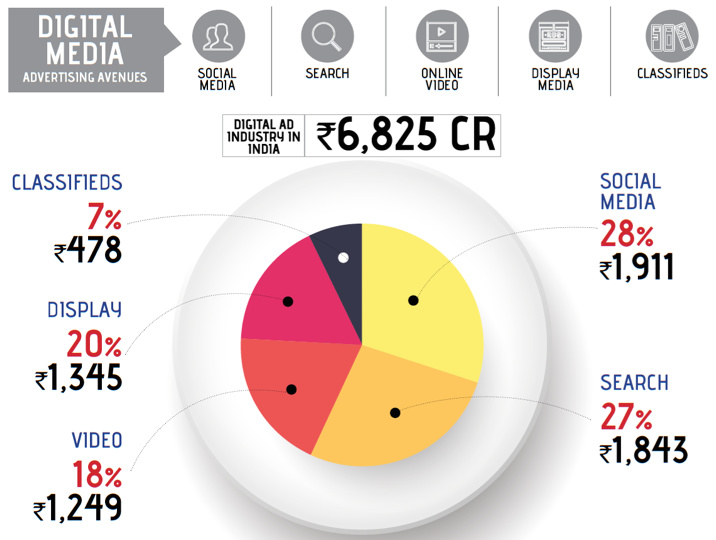

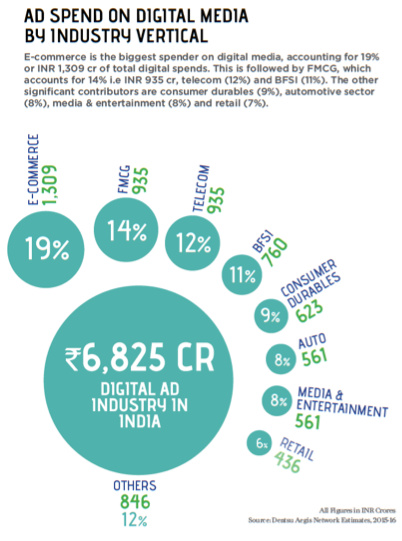

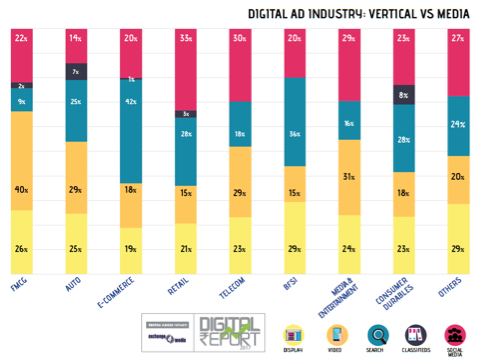

While there are several reports referenced above which provide more or less similar data points, I found the Dentsu Aegis network -Exchange4Media report most useful. Please bear with me for presenting next the visual charts to draw attention to the most relevant data-points for our exercise. Felt this is the quickest way to bring everyone on the same page (instead of writing voluminous text  )

)