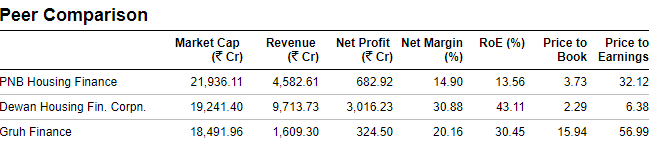

I guess what @SlownSteady trying to ask @hitesh2710 was this wide disparity in RoE when compared to other HFCs and whether PNB is still undervalued when compared against this criteria.

As Aditya mentioned above, ROE calculation also includes net profit that are not redistributed to shareholders as dividends also called reserves.

Generally price of a financial share depends on growth expectations and ROE. While growth expectations are good for PNBHF, the ROE is sub par. So Is PE of 25 is justified?

I have invested 5% of my portfolio in PNBHF at a price of Rs1,310.

@hitesh2710

Congratulations for excelling in medical field as well as investing. Even more Jai Ho for being an excellent teacher in VP forum.

I hold 3 HFCs bought in sequence 1. Repco 3.75% of my pf( after booking out most of it getting almost 300% gains). 2. Can fin 27%of pf (entry @196 after split) & recently 3. PNB hsg 3.75% (late entry @1215). Lot of noise that better days of HFCs are gone. But Govt want affordable houses for all. So far HFCs are leading this bull market. Even after demonetisation, RERA, registration problems in South, GST etc they are growing. NPAs seems to be temporary in nature in home loans & somewhere I read that real loss is very less(probably <4% of total home loan) even if a defaulter doesn’t pay. NPAs are the main killers for lending businesses.I hope next 2 to 3 years may be bumper years for construction of affordable houses by most of the known real state companies helped by newer technology of prefabricated houses etc. Reduction of EMI due to interest subsidy should be a big trigger. with your experience please guide me if I am right to have almost 35% of my PF in HFCs. Secondly you can see that I hold most of it in Can fin bought in late 2015. Canara bank is in process of selling their holding but they are not consistent in their public statements which has caused significant correction in prices. Is it a good fundamental & technical hold. Dr Bajaj

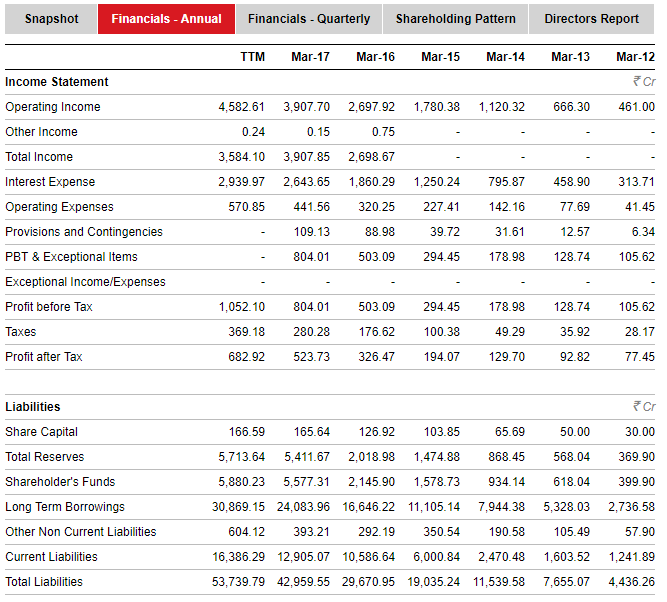

There have been a lot of queries on the poor ROEs of PNB HF as compared to peers.

I think with consistent growth, there should be reduction in cost to income ratio which at around 28% is highest for PNBHF amongst all HFCs. For other HFCs it is in the range of 14 to 17% and for HDFC it is around 11-12% and for DHFL it is around 26%. So with new offices generating higher businesses and loans per employee going up there could be sufficient space for improving cost to income ratio. This should help in improving margins and ROAs.

ROEs in case of financial companies is ROA multiplied by leverage. As compared to gruh and other comparable peers, leverage at 9% is lower. For other companies it ranges in vicinity of 12-13%.

So for ROEs to go up there are enough levers which PNBHF can utilise. Usually once a company grows for a few years with reasonably good asset quality, all other parameters tend to fall in place. I recall similar concerns which were prevalent in case of canfin back in 2014 or thereabouts.

Hitesh bhai, Would like to know your view about Aksh Optifibre in view of digital revolution happening in our country and also as they are entering Opthalmic Lenses manufacturing. The businesses of this company seem to have good growth potential. Huge equity and low promoter stake however are prohibiting me to take a plunge. Your expert view please…

Hitesh Bhai, I am new to technical analysis, and want to combine it with fundamentals. Could you please suggest resources/books to initiate on technical analysis? I tried google search and shortlisted the following books 1) Technical Analysis of Stock Trends by Robert Edwards, John Magee 2) Technical Analysis Explained by Martin Pring 3) Technical Analysis of the Financial Markets by John Murphy. If you could suggest simpler way to approach the topic, that would be great. Thanks.

I dont track aksh optifibre but have been looking at the charts off and on since it was put up as a technical pick by @Mehnazfatima. The stock price has doubled from his levels of around 20 odd. Must have been because of strong sectoral tailwinds as in same space, sterlite technologies also has done very well.

I read some time back about bajaj finance having written down value of mobikwik for further increase in stake. That might be perceived as negative. And the stock is in a corrective phase, posting lower lows while market is going up. It might be prudent to wait and watch some more time.

I had bought it at the time of demonetisation but exited some time back looking at weakness in technical structure.

Hiteshbhai, which should be the 1st book to read out of all these for a typical long term investor but willing to use technical as 2nd filter. Intent of this question is to start from right book to make correct base and use limited time effectively.

One chain of thought is that aviation industry has finally figured how to make consistent profit. Somewhere I read that globally aviation profits are on rise and unlike in past new capacity addition is less disruptive. As a proxy, one could argue when was the last time a US carrier declared bankruptcy (rhey were famous for it).

And as a frequent traveler, I can vouch that flights are consistently full.

@hitesh sir,

Thanks for the book name.Could u advise some sites wherein I could see the price & volume charts of Indian stocks in the manner described in the book.If more than one, which one is better?

Hi Hitesh @hitesh2710 , Congrats for the feature, saw it a bit late! Your contribution to this community needs no special mention. Well deserved and wishing you more success in life! You are an inspiration and source of knowledge for many.

I know that you followed Page Industries very closely, how do you assess the current valuations given that growth has revived from the past 3 quarters albeit not at supernormal 35% but 20 levels? Secondly, the revival in the Ajanta Pharma?

Would like to know your opinion about Bosch India. It is supposed to be a high quality business but is in downtrend in this bull market. It is currently on 200 week moving average which is considered by some people as ultimate support level. What is your reading of Bosch, from technical as well as fundamental perspective?

congrats @hitesh2710

I dont have to write about your skills. But its your humility which makes you different from the rest of the people. Also i am impressed with your patience to answer any type of questions.

Wish you the best sir

@hitesh2710 could you pl. give your opinion based primarily on technical analysis & fundamental on APL apollo pipes & morepen lab as I feel they are indicating a pattern, though volumes in APL apollo pipes r not large.

Hiteshbhai-Request some elaboration about the weak technical structure in Bajaj Finance to understand better. It is definitely a marquee name in financial services with excellent demonstrated execution skills.Since it forms 16% of my PF-keen to understand