In reference to the above post,

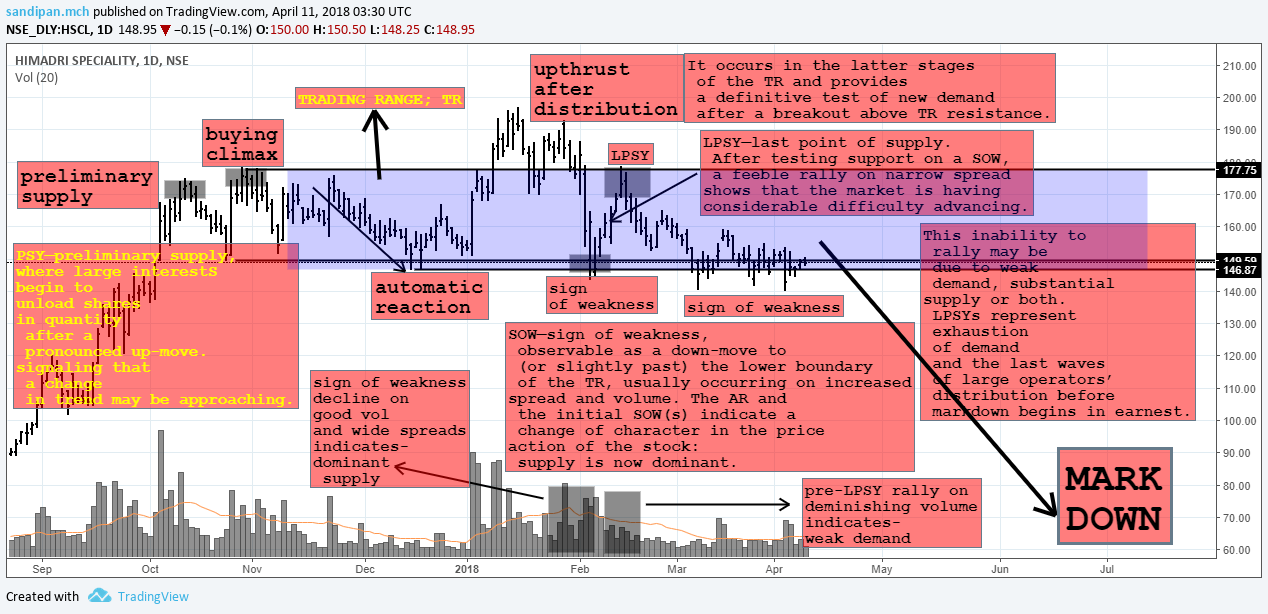

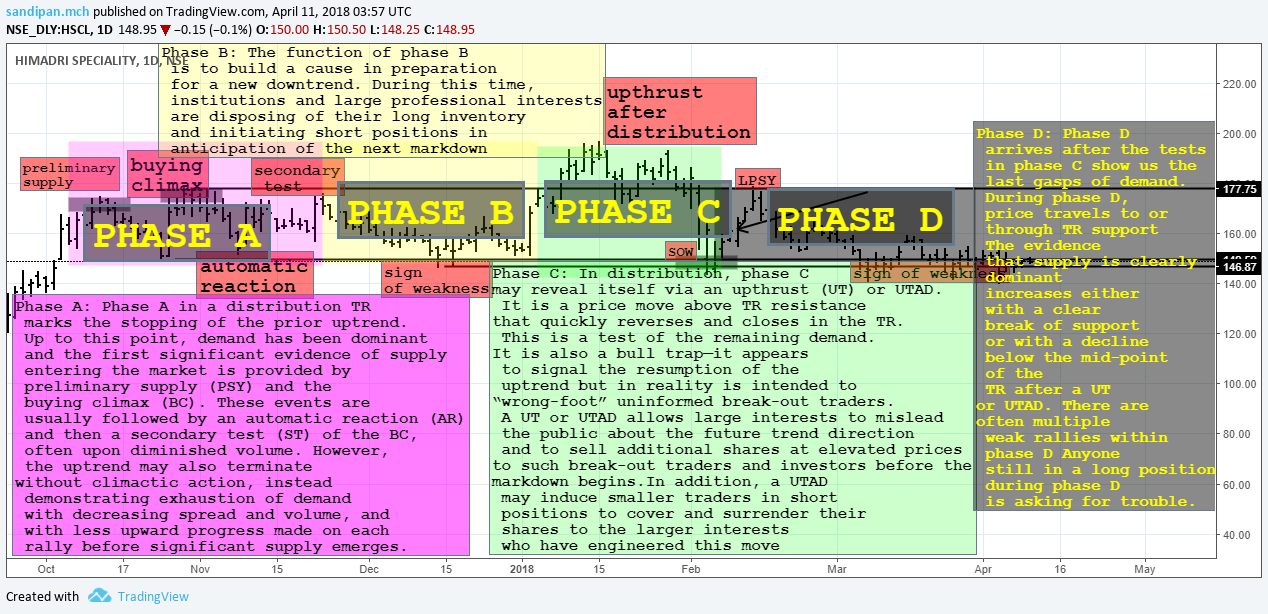

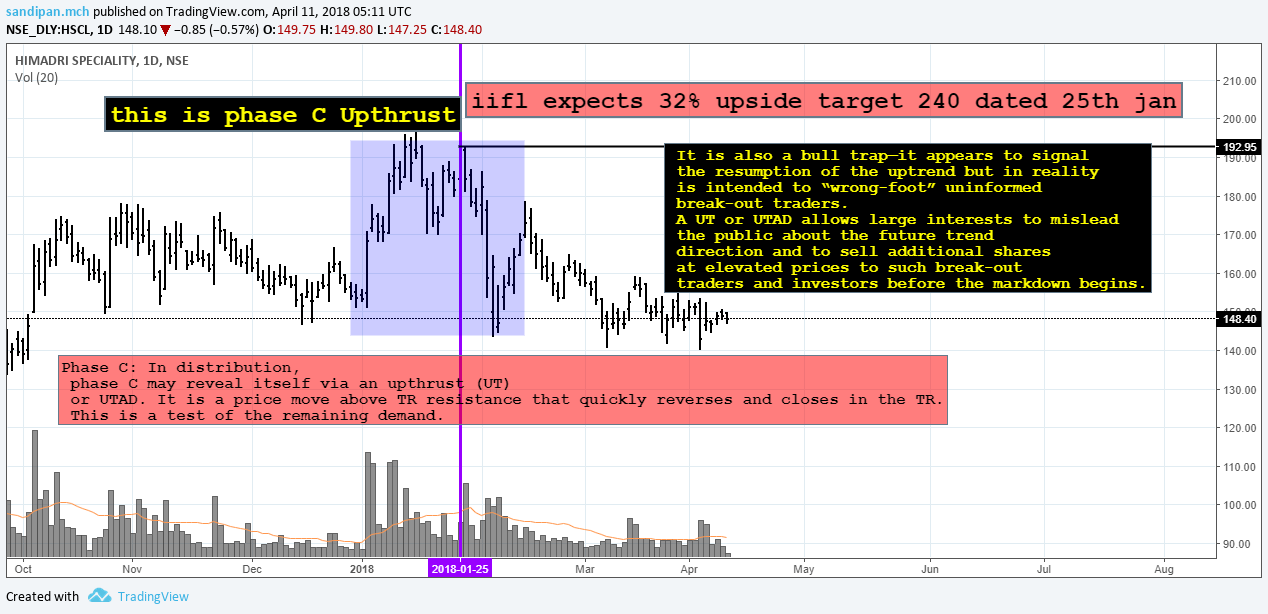

This is the breakup anatomy of the Wyckoff Distribution

This is a beautifully orchestrated happening by the operators , otherwise invisible to the Retail eye…

This is a bit cumbersome i know…

But its beautiful if can be read with attention i believe…

was fun charting it also…

I have used reference from this link for better written description http://stockcharts.com/school/doku.php?id=chart_school:market_analysis:the_wyckoff_method

This is the first part, which is the basic component-events

Here the Phase A and B transition is not distinct, so some position of event change has been done in the second one…

Hope this helps…

Disclaimer… This is a pure technically analysed opinion, keeping fundamentals at bay…

Not an investing/trading recommendation…

Not invested/not interested.

Crude at 3 year high, above $72 and looks heading for $80, going by macros and geopolitics (I feel these are lagging indicators in this case). I think it will be manipulated to get to $80 for Saudi Aramco listing.

Disc: Booked out all my holdings as the thesis is not as strong as it was in the last couple of years.

it will be staircase like breakdown i presume…

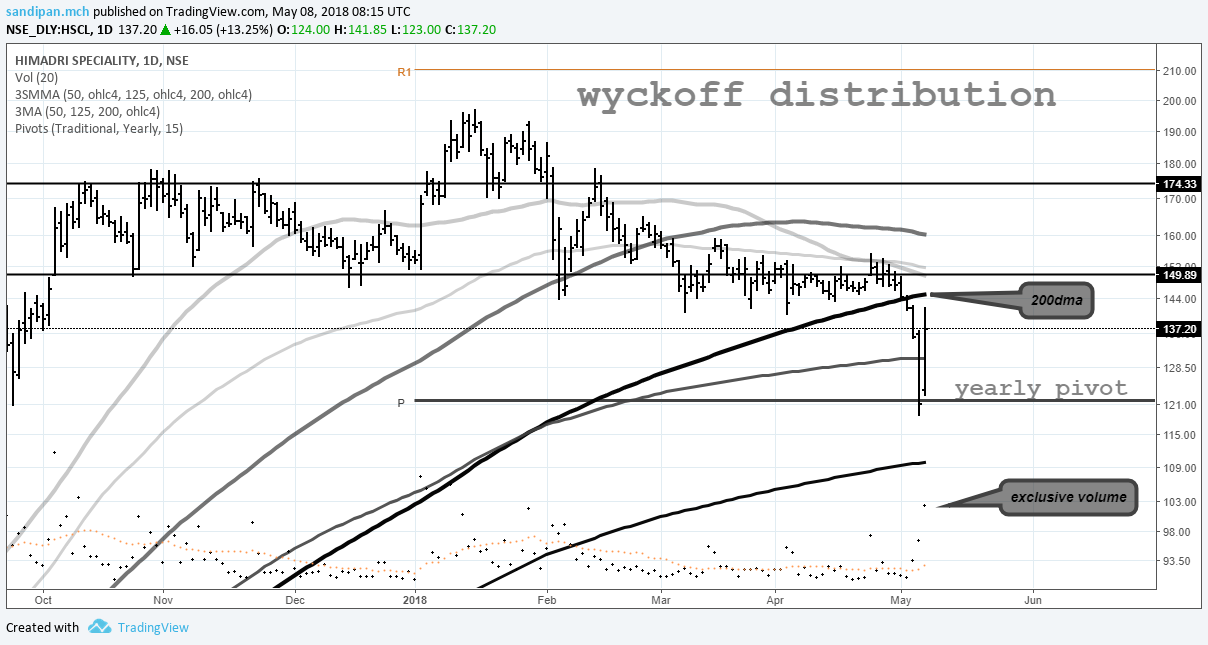

The yearly pivot most likely be a major major support, the effect of the automatic reaction from the support towards the 200day moving average on tremendous volumes shows the significance…

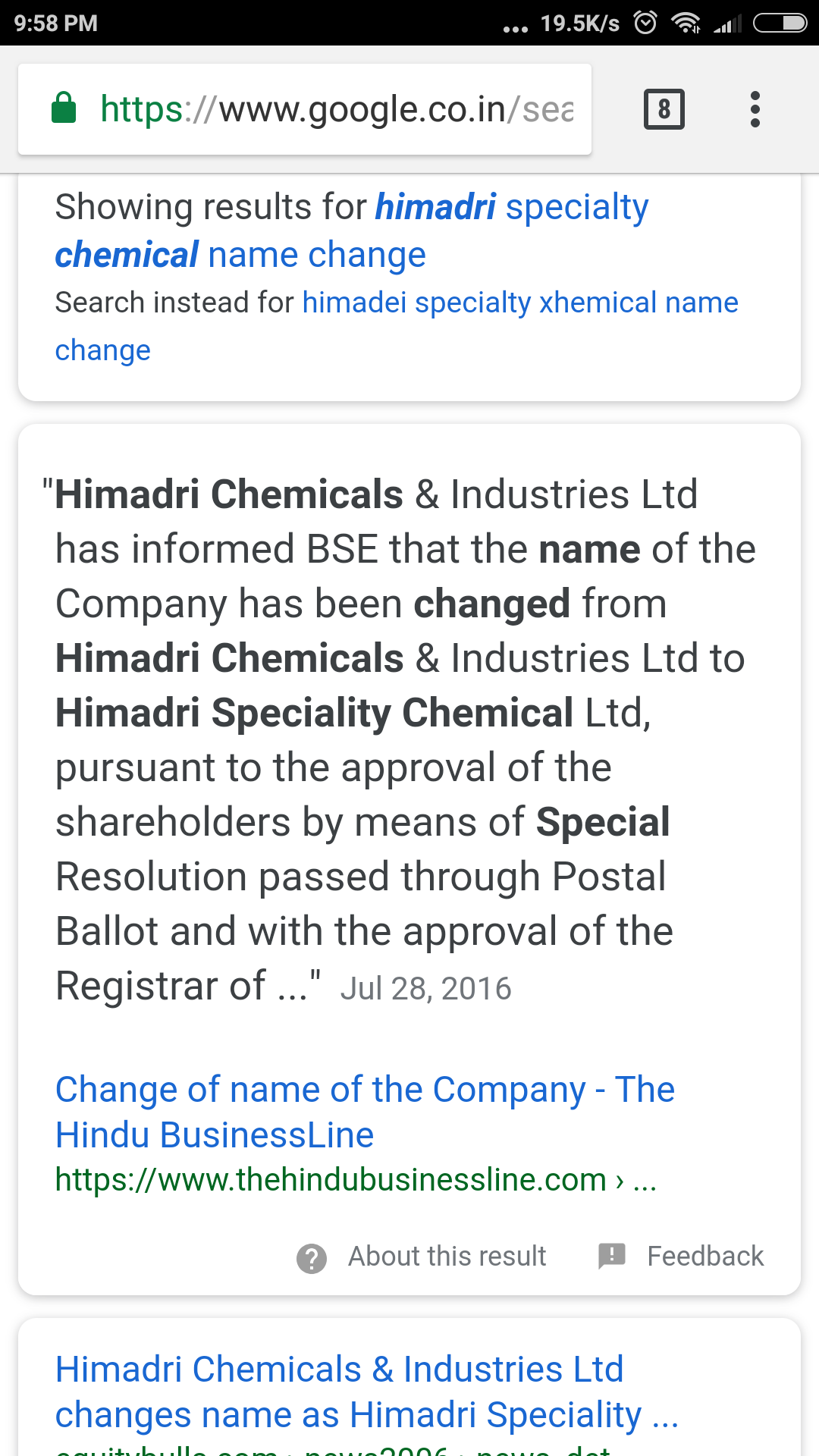

Himadri Speciality Chemical Conferred World’s 100 Greatest Brands 2017-18. In addition, Mr Anurag Choudhary, CEO, Himadri Speciality Chemical Ltd. was recognised as a “World’s 100 Greatest Leaders 2017-18”

7 dispatches in 7 days ranging from website redesign, appointment of PR agency and awards and recognition etc. Is it a mere coincidence that on 8th May they appoint a PR agency and on 10th May, HSCL is in 100 greatest brands and the CEO is in 100 greatest leaders? Just looked up “India–UAE Business and Social Forum” - It seems to be run by Asianet and is in all likelihood a PR venture that provides awards to the highest bidder.

The company does not quite provide the break up of revenue split in to CTP, Carbon Black, Advanced Carbon Material(HSCP), Napthalene and SNF. At least the specific about proportion of revenue and profit contribution thorough CTP, Carbon Black and Advanced Material would be helpful. I could not find it even in the investor presentation. Also, last quarter’s utilization for all these segments is not clear. Also the commissioning time line for proposed expansion - for 20000 MT advanced carbon material & 60,000 MT speciality carbon back is not clear. Does the management hold conference call. If any board member can throw light these aspect, it would be very useful. Thanks

They have arranged a concall.We will get more clarification about segment.yes its strange and not helpful at all.But they discuss this point in concall.

Listened to the concall - There is a lot of noise around optimism for demand and performance Having said that, there are few key takeaways from my point of view.

Cash flow for the FY18 was 316 Crs. post taxes and working capital; Debt reduction is 89 Crs.

The capex for next 2 yrs. is in tune of 600 Crs. This will be entirely funded thru internal accruals. There would be no dilution of equity. There would be no incremental debt taken for funding the capex.

The above referred capex to be used for expanding Advanced carbon material by 20,000 MT by FY 2020 & 60,000 MT speciality carbon black at the end of FY 2019.

For FY 18 company had 10 grades of speciality carbon black. They plan to have about 40 grades of carbon black in next 2-3 yrs. Company aims to get in top league of speciality carbon black producers such as Orion, Cabotcorp in next 5 yrs.

The current 15 MT capacity for advanced carbon material is completely sold out and operating it at 100%.

Antidumping duty on SNF material is expected to improve realizations and utilization for that product

CTP distilation capacity to increase by 20% and come onstream from Q3 after the annual shutdown

Overall, very positive commentary. The only negative I could sense is - Management is not ready to admit for any negative scenario They did not provide the revenue contribution from the Advanced carbon material. For me, management making sure to not increase debt or dilute equity are positive signs. Focus on “speciality” products is another positive. However how “special” the execution and demand turns out - That needs to be seen…

History tells us to be more cautious about companies who change/tweak their names to suit to flavor of the season. In 2014-16, all of a sudden some company realized the special situation of being a specialty company.

Having said that, there are few key takeaways from my point of view.

Having said that, there are few key takeaways from my point of view. They did not provide the revenue contribution from the Advanced carbon material. For me, management making sure to not increase debt or dilute equity are positive signs. Focus on “speciality” products is another positive. However how “special” the execution and demand turns out - That needs to be seen…

They did not provide the revenue contribution from the Advanced carbon material. For me, management making sure to not increase debt or dilute equity are positive signs. Focus on “speciality” products is another positive. However how “special” the execution and demand turns out - That needs to be seen…