1 Like

I think the product they produce falls under speciality domain. Then why not claiming the speciality product maker status.

Moreover we should track the earning profile and management integrity of a company more, rather than name changing history. With respect to earnings company is doing good and I dont see any suspicious wrong doing from management end. Now people with different openion would say all the awards and appreciation company getting in last 6 months are paid and fake. Now different people would have different say on different things.

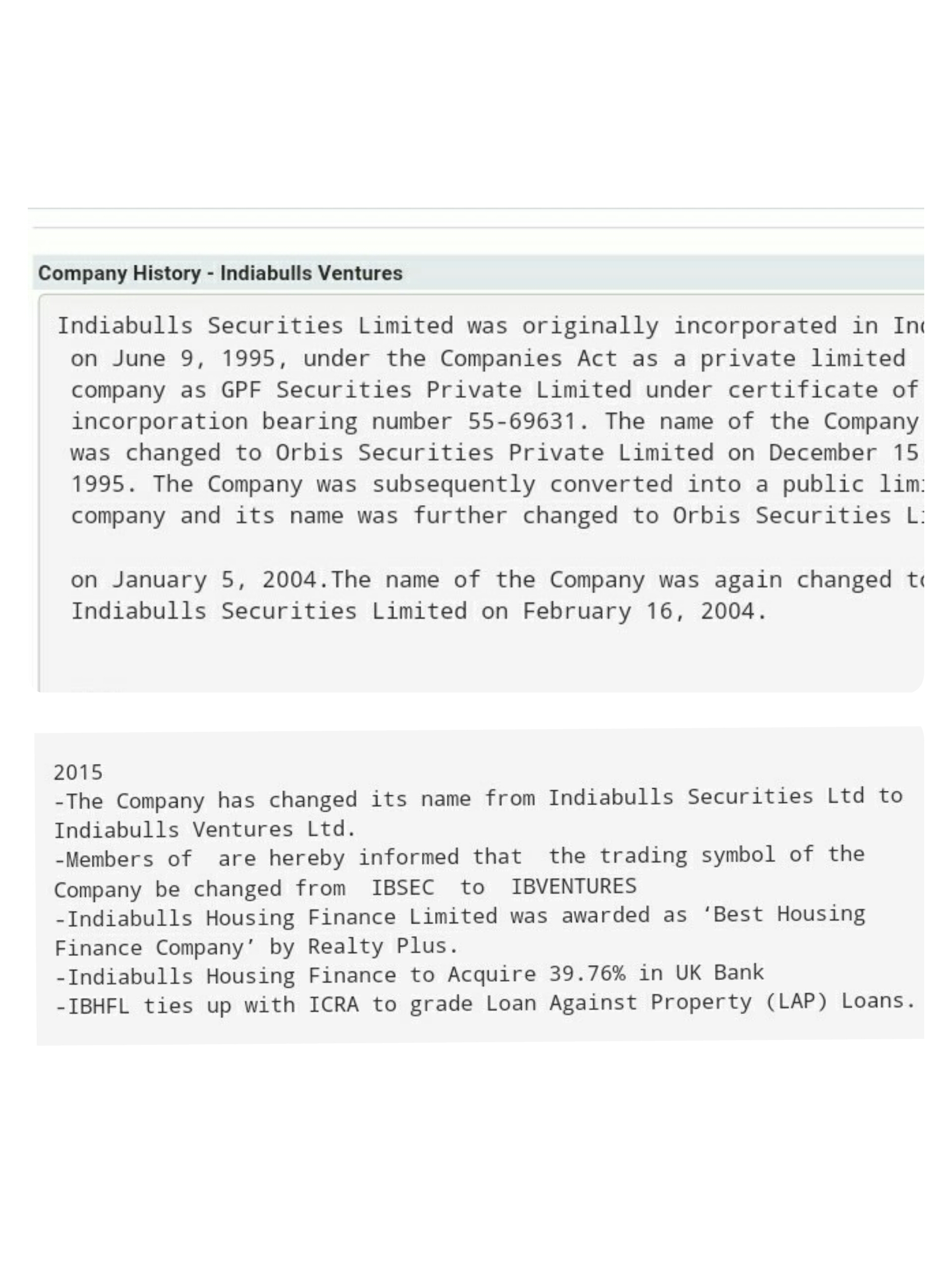

Even if we see the name changing history of Indiabulls group, they have changed multiple times. But IB group is one of the most aggressive group in India today who made a lot of people super wealthy by their earnings, and still doing exceptionally good.

1 Like

Himadri Speciality Chemical Ltd’s Q2FY19 standalone net profit rises 44.82% yoy to Rs74.09cr

The company’s standalone revenue stood at Rs601.77cr, up 28.58% yoy but down 0.49% qoq

operating profit for the quarter increased by 26.5% yoy to Rs 129.8cr

EBITDA margin declined by ~36bps yoy to 21.6%

adjusted net profit after tax stood at ~Rs74.1cr, up by 44.8% yoy

other expenses increased by 41.5% yoy to Rs55.1cr in Q2FY19. This includes forex loss of ~Rs12.1cr

finance cost decreased by 15.8% yoy

total borrowing of the company came down to Rs537.7cr

effective tax rate of the company for the quarter stood at ~30% vs. ~32%

Nothing special in the results. They are now keen to raise funds via equity (most likely) although initially they had said they were would not dilute stake. Also, they have delayed Advanced Carbon Materials project timeliness after making big noise about it in last one year. Poor Corporate Governance

1 Like

The theme of ev will be big in times to come. Himadri to significantly benefit from lithium ion batteries esp advanced carbon. With refinery increase by reliance more coal tar will be available to develop advance carbon materials for ev. Graphite india and HeG are key clinetele. EV arc furnace will also increase in India after china with rapid pollution concerms and renewable target. This mega trend will be exponential like all trends after the advent of internet. Electric vehicles once again finding its rightful place after killing off by rockfeller oil lobby in 1900s.

https://www.bloomberg.com/news/articles/2018-11-19/evs-set-to-become-the-biggest-battery-users

Is there any news on this counter? Massive buying seen at last minute of today’s trading session and after hour buying qty is showing more than 3L with 132 buyers !

I received a e-Voting for Himadri Speciality Chemical Ltd mail with below Special Businesses:

-

Approval for raising of additional capital by way of one or more public or private offerings to eligible investors through an issuance of equity shares or other eligible securities for an amount not exceeding Rs.1000 crores. -

Approval of Contracts/Arrangements with Proposed Related Party.

I do not see any announcement on BSE website on this. How is it possible? any views?

On 12 Nov board meeting company declared about the the 1000 Cr fund raising.outcoming of board meeting released that time.

For second item, related party transaction, promoter has 2% stake on an EPC company which has taken expension work in its site

1 Like

Was wondering if anybody caught this from the FY17 annual report:

"The Holding Company, on 24 September 2001, had issued 12,300 Deep Discount Debentures (’‘DDD’’)

of face value of 100,000 each to Himadri Coke & Petro Limited, aggregating to 12,300 lakhs at a

discount of 90% on face value and which were redeemable at par at the end of 20 years from the date of

allotment. The DDD carried an implicit rate of interest of 12.18% approximately compounded annually.

During the year ended 31 March 2016, the terms of the existing DDD were amended to provide, inter

alia, terms of conversion of the DDD into the equity shares of the Holding Company. Accordingly, by way

of approval of the shareholders by a special resolution, passed at the Extra Ordinary General meeting

held on 22 March 2016, the above DDD were converted into 32,675,297 equity shares of 1 each at a_ _price of 19 per equity share (including a premium of 18/- per equity share) aggregating to 6,208.30

lakhs as per the valuation report of an independent qualified valuer. The above equity shares were

allotted on 25 March 2016. On above conversion, ` 2,152.50 lakhs was transferred from Debenture

redemption reserve to General reserve. The Holding Company has complied with requisite provisions of

the Companies Act, 2013 and SEBI, as applicable."

Essentially, non convertible debentures issued to promoters in 2001 got converted to equity at 19 per share - which was the approx. price then anyway.

So in 2001, the company borrowed ~12.3 Cr @ 12% + compounded from the promoters.

That 12.3 Cr is now worth 390 Cr + just because a conversion to equity was allowed by shareholders.

4 Likes

12300 lakhs is 123cr.

yes. but issued at a 90% discount to that FV of 123 Cr = 12.3 Cr

Himadri Carbon Black has appointed Weber & Schaer GmbH & Co.KG (W&S) as its exclusive distributor for ‘select’ rubber end-use markets in several EU countries, W&S has announced

The deal, which covers Germany, Austria, Switzerland, Benelux, France, Spain and Portugal, follows a “significant capacity expansion” at Himadri’s specialty carbon facility.

Himadri is a division of Himadri Specialty Chemical Ltd (HSC), a supplier of carbon-based products based in Kolkata, India.

2 Likes

Very detailed investor presentation for Q3.

They claim to have improved on Ebita per ton. Volumes are lower but sales, EBITA are higher compared to earlier quarters. Is it indicating at better pricing? would be very useful to know view from fellow boarders.

Himadri Speciality Chemical is ranked no. 1 on the Fortune India Next 500 list, the definitive ranking of India’s largest midsize companies.

I would personally not give much weightage to such rankings. They tend to be purely short term number driven and does not make a lot of sense for cyclical companies.

For the love of the fortunes n Forbes n Deloitte rankings . This is just an example. There r many.

1 Like

They have Quick ratio of 0.69 and current ratio of 1.44. Both are low in compare to what is required. Is it matter of concern? Can someone put some thoughts on this.

1 Like

Investor Presentation

After bouncing from 96 level during Feb 2019 to 124 within 1 month ‘HSCL’ stock again starts declining and back to 98 level again.

What are the reasons behind it as last quarterly result was better

- Debt to Equity is reducing and now below 0.5 level

- For last 3 years EPS, ROCE (%) is increasing