A capex of Rs 628 cr has been approved for capacity expansion of 30 mmtpa in carbon black and 200,000 mt in advanced carbon. The funds would be raised through equity instrument/s.

One thing to note: Q2 revenue and other expenses are not comparable with earlier quarters. Q2 revenue of Rs. 470 crores is net of GST, whereas exceise duty formed part of other expenses in earlier quarters.

1 Like

Whats the inference from this Madhavi…is it +ve and showing better results?

There was a 50 cr excise duty last quarter. Net of that revenues have gone up slightly.

Dear @amberjain2001, I am not an expert on GST/ excise duty, hence my interpretation could be wrong. Friends, please correct if I am wrong. I interpret it this way: Q2’18 revenue figure excludes GST. However, I am not sure about the exact GST rate applicable. If we just approximate the Q2 GST to the Q1 excise duty of Rs. 50 crores, the equivalent Q2 revenue could have been Rs. 518 crores. This way, my interpretation is that, Q2 sales are higher than Q1

HIMADRI VS RAIN INDUSTRIES

Both the companies along with philip carban or Goa carbon rising because of rise in demand seen in Aluminium industry , rising demand of Electic blast furnace process in steel industy i.e pollution problem seen rising because of heated blast furnace method. Also shut down of many industries chemical and steel co in china due to environmental issues.

Rain industry is present mainly in CPC, CTP and other speciality chemical and cement plant. They are one of the Global leader in CPC with capacity of 2.1 MMTP ( proposed to increase to 2.45 MMTP) and 1.3 MMTP of CTP.

Himadri speciality on the other hand is leader in INDIAN CTP market with 70% market share ( 0.4 MMTP). CTP is the product having entry barrier in usage because of its properties of use in liquid form where it has advange of usage in Indian market. They have carban black capacity of 1.2 LMTPA ( proposed to increase by 30,000 MTPA) and Advance carbon material proposed to increase to 20,000 MTPA

Though PE and PS ratio or capacities of Rain industries( 24 and 1.1) are much better as compared to Himadri ( 45 and 4.2) however D/E ratio of himadri is lower than Rain.

Himadri Management in its concall said they are concentrating on high margin value added product . It has developed zero QI ( quinnolene insoluble) pitch ( one of three global manufacturer) , special pitch for long range missile and SNF for non construction ( agrochemical, gyspum) . Himadri is only producer in India for Anode material for Li-ion battery.

Both CPC and CTP are used in Aluminium industry smelting and for making Graphite electrode. Rain is Global co with huge capacities but himadri looks interesting too looking at product portfolio and continous R&D in Advance carbon product and capacity expansion.

Recent capacity addition will be done by equity infusion of 628 cr for which shareholder approval has been taken.

8 Likes

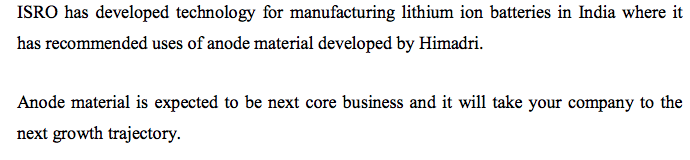

ISRO offering its technological competence on Lithium-ion batteries to BHEL is a bit of old news. Hopefully this will materialise soon enough to make domestic production commercially viable. Even if cells can be manufactured, getting automotive grade batteries might be a completely different ballgame.

In the last earnings call, I noticed this part about ISRO recommending anode material manufactured by Himadri. It could be way into the future but if things go well, this will auger very well for HSCL.

Reference:

http://www.himadri.com/HSCLConcallTranscriptQ1FY18.pdf

5 Likes

http://www.bseindia.com/stock-share-price/VotingResultMtingResult.aspx?scripcode=500184&expandable=1

Hi Abhishek, Are you invested in HSCL now?

Anti-dumping duty on SNF. With 68k TPA installed capacity, and an estimated $397 anti-dumping duty (Rs.25,000 roughly), this could be a great benefit of HSCL.

1 Like

1 Like

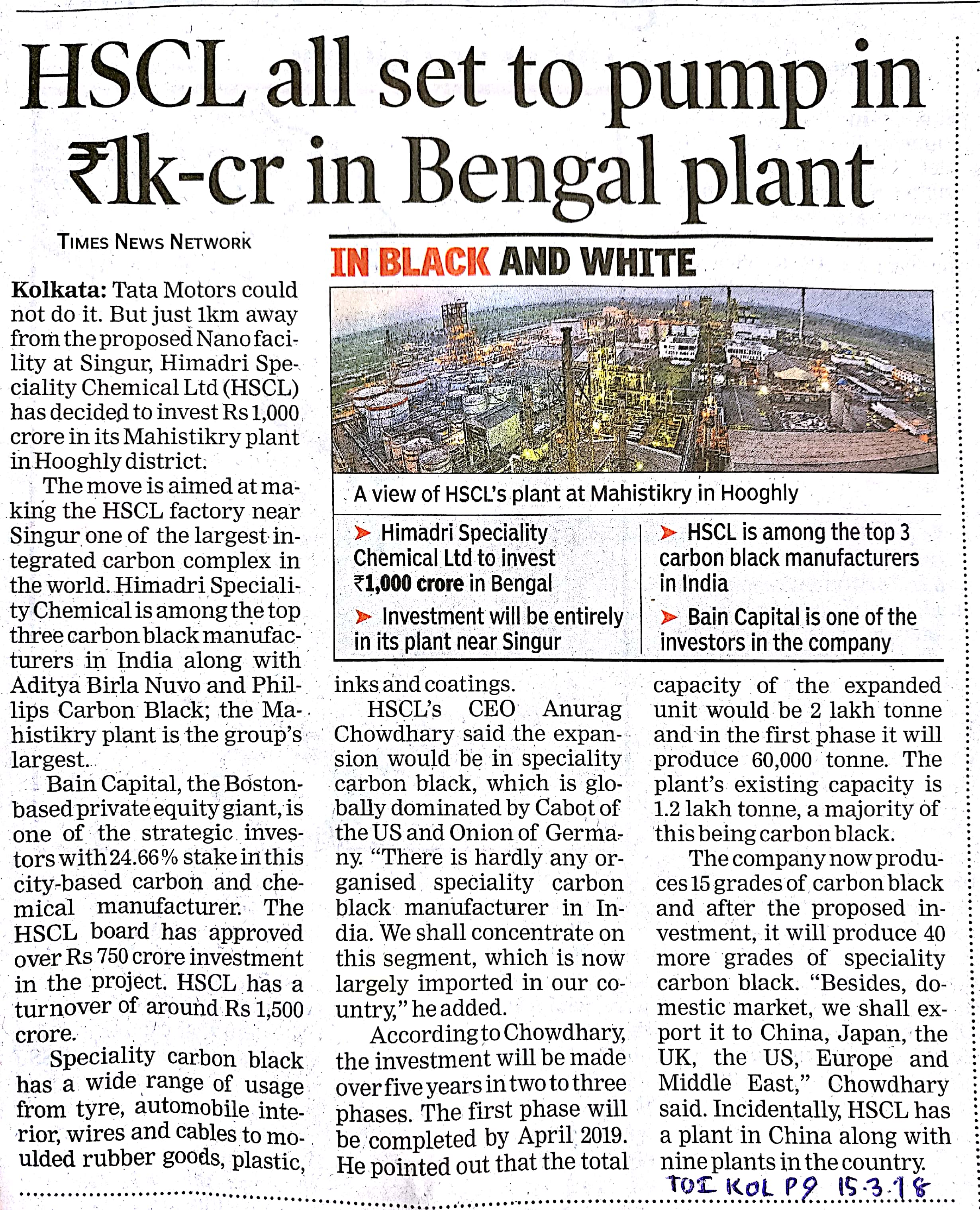

Himadri has come up with excellent Q3 results. Net profit of Rs.70.14 crores, as against Rs.20.11 crores in Q3’FY17 and Rs. 51 crores in Q2’FY18. EBITDA increased by 78% Y-o-Y. Also, has come up with a Capex Program of Rs. 780 crores. Here is the Investor Presentation: http://www.bseindia.com/xml-data/corpfiling/AttachLive/96161ce2-4c6d-47c8-a475-832f92950f91.pdf

3 Likes

Anti-dumping duty imposed on SNF. At about $200/MT and a 68000MT capacity, the impact on topline may not be too much. 15% is SNF’s current contribution to topline.

Disc: Invested

Unable to understand the recent under-performance of this stock, in spite of the excellent Q3 results, expansion plans and the bright business prospects. Anyone can please throw light on this?

I was thinking a lot of it could be due to LTCG - I have reduced my stake here by about 50% couple of months back. This has had a considerable run up from sub 20 levels to current and has been overvalued from the time it crossed 100. Even at current levels (> 30 P/E) it is expensive but I am thinking of holding on to the rest of the position until Q4 results. For me this was a play on crude oil price trend and Carbon. I am not sure how much steam is left in that theme now so I am cautious but will hold for a bit more (Q4 results as I mentioned). I think we might be near peak earnings as of FY18 and the new capex for 1k Cr could be a while to come online and I am not sure how they are going to fund it either and how the demand will be. The story will turn on its head if crude slumps in FY19.

3 Likes

i am unaware of the in depth fundamentals of this company…

But i bumped into the chart of this stock, and i felt worried, thats why this post to my fellow analysts…

This stock has had an incredible run i see in this chemical bull run we saw

But now the situation looks different, the institutional money seems to be changing boats…

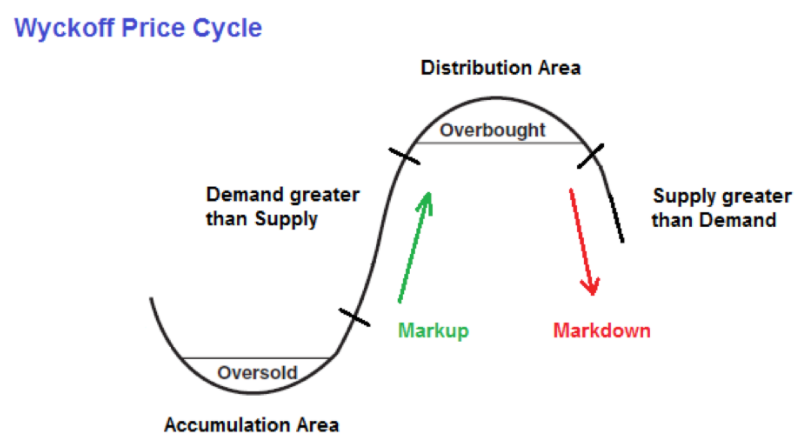

that leads to the common phenomena called distribution, where the institutions and operators off load their share holding to the retail… This is a slow and unconscious process to the fundamentals, and this is done in an artistic way so as not to create a sudden sell off, rather maintain the price at higher levels and create steady supply at good prices… colloquially called…“bull trap”

The opposite of this process is accumulation…

The concept roots from Richard Wyckoff’s PRice cycle, demostrated over a 100 years ago…

here is a schematic diagram…

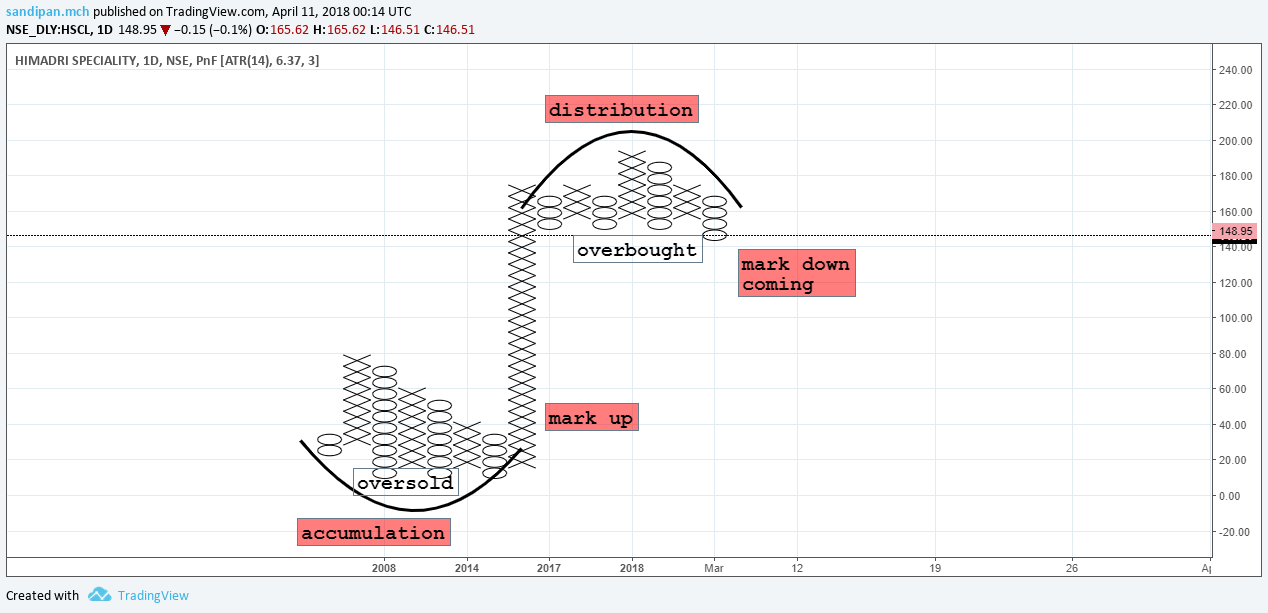

And here is how Himadri specialty looks on the charts, i have refrained from the price targets as it will not be fair to the house rules, but to least to speak, it is very uncomfortable one…

[PLEASE NOTE .: this is a point and figure chart which Wyckoff used to demonstrate the phenomena, which is a 1D chart, and dosent have a X Time axis, only The price …A distribution can go from weeks to several years, there is nothing definned about that, but surely is a long term process]

This is a cautionary message, nothing else…

This chart brought back to my mind , CNBC awaz presentations of this company, multiple times in the last few months and i completely failed to understand why would one buy this stock in such an expensive valuation as a value pot…!

Now it makes sense.

Disclaimer… Not invested, Not interested

4 Likes