I think the reason for Rain’s lower P/E or relative undervaluation could be due to the following reasons.

The product mix for the two companies is different. CTP is 73% of HSCL’s revenues and Carbon Black is 27% where as Rain Industries CTP & CPC contribution is 19% of their Carbon products revenue and 13% of their overall group revenue.

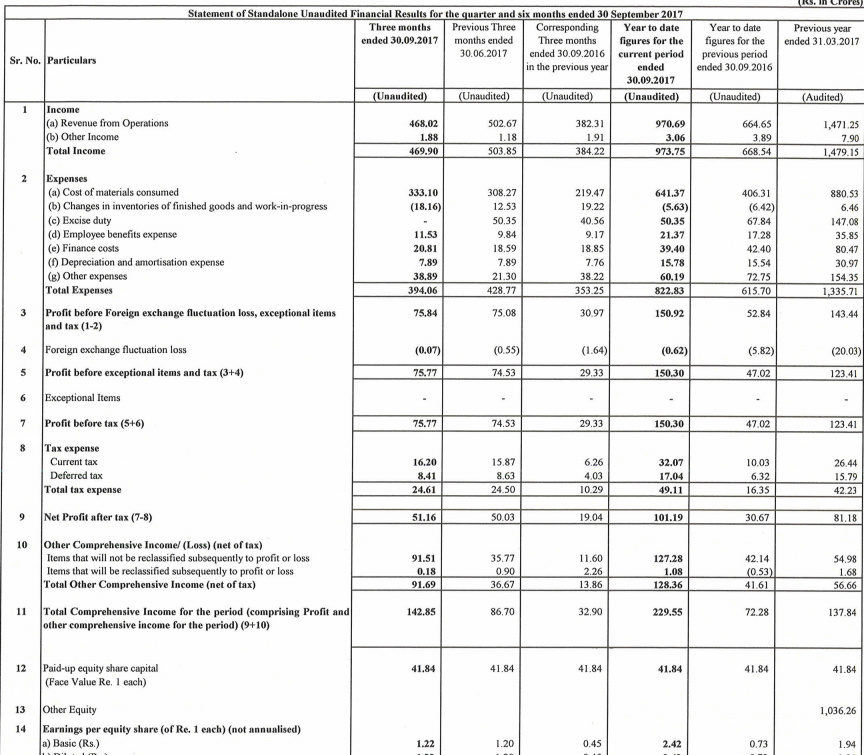

CTP and Carbon Black is where HSCL is seeing improved margins and the same can seen in their improved showing QoQ where their OPM is now at 22% where as Rain’s product mix doesn’t allow them similar margins. It looks like HSCL may have clients willing to pay higher for quality Carbon Black (from the concall) which is helping their margins. Latest quarter margins for Rain are 17.74% and HSCL are at 22.07% which seems like a significant difference.

HSCL has 70% market share in India for CTP and it looks like demand for Aluminium is higher in India and is set to grow from 2.75 million metric tonne from annum now to 4 million metric tonne per annum by FY19. Rain’s Asia revenues contribute 22% to their overall revenues and unsure about their market share here in India. So looks like HSCL has more to gain from Nalco, Hindalco, Balco and Vedanta’s growth than Rain.

Debt situation is very different for the two companies. HSCL’s D/E was at 0.67 as of May and they have further reduced debt in August when they cut their long-term debt from Rs.414 Cr to Rs.310 Cr. This should bring their D/E to under 0.50. Rain’s D/E as of June is at 1.8. This again is a significant difference.

Revenue and Earnings growth of the two companies as well are in totally different trajectories. Q1 FY18 Sales growth for Rain is at 5.24% vs HSCL’s 77.34% growth. Profit growth for Rain in latest quarter is at 12.54% vs HSCL’s 330%.

So overall I think market factors in these things when assigning a P/E. Thoughts welcome.

I might be saying something controversial here without facts to back my statements. So ignore if you like.

Its becoming increasingly difficult for us small investors to seive out the paid news and noise from actual impacting facts. Thats how the media industry is shaping up to.

I am sure if some of you have worked at startups or been associated in some form with one then you would be smiling reading this. Media treats paid news as a revenue source. Let me be blunt.

Unfortunately small, naive and guillble investors get so hyperexcited with such news - xyz had this portfolio and this abc conpany returned 7000% and these are unfathomable business metrics which will take alphabetagamma company straight in mangalyaan to mars, that they go and invest their hard earned money.

Join some whatsapp group and you will see the tragic fun. Or see the twitter handles everyone seems to be trying to get clients there!

My two cents. Moderators please delete if irrelevant.

Regards

Deepak

p.s. Not saying that this article is paid or not. As usual a small fish is only to be served on the shark’s plate.

To get some perspective on the valuation, I tried comparing it with Philips Carbon Black which is trading at around 25 P/E vs HSCL’s 34 P/E. Philips Carbon Black is a sole Carbon Black manufacturer with a capacity of 4.8 lakh TPA vs HSCL’s 1.2 lakh TPA. PCB’s capacity utilisation is close to 94% and they mention that de-bottlenecking would improve this by 5%. PCB is market leader in Carbon Black and has a market share of over a third domestically while HSCL has 17%. More importantly, PCB’s carbon black revenues mostly come from rubber Carbon Black which is used in tyre products. Their non-rubber Carbon black revenue is only 9% of Sales and they mention in their presentation that they intend to develop more non-rubber products where the margin is higher.

HSCL however has a variety of products in their portfolio and are not dependant only on Tyre industry for their Carbon black revenues and have several advanced Carbon black products. HSCL looks to be way ahead of PCB in terms of product innovation.

This of course is comparing just Carbon black business because that’s what PCB is into. In addition to this HSCL’s main contributor to topline is Coal Tar Pitch where they have a 4 lakh TPA installed capacity and have a market share of 70%. They have Aluminium grade and Graphite grade and also specialty grade used in warheads.

Then there is SNF with a installed capacity of 68000 TPA. Anode grade carbon (Lithium-ion batteries) could be a growth driver in the future.

Unfortunately, segment-wise revenue is not present anywhere in the AR.

The product mix and innovation sort of justifies why HSCL is valued the way it is.

They are talking of improving working capital cycle which would increase the cashflows which is a positive news.

Himadri’s core is currently Coal Tar Pitch (CTP) which constitues around 73% of the revenues.

There is a lot of dicussion going around electric vehicles (EV) and Li-ion batteries they would use along with

Li-ion application in other products like phones, laptops, power banks, etc.

This segment would not have much impact on FY2018 revenues.

From FY2019 onward, the game changer and new core for Himadri could be this advanced chemical space where they are talking of big expansion once 50 tonne / month is achieved.

This would become a significant contributor to both the top line as well as bottom line considering the

high margins this commands.

Since this is an evolving space, this seems to be a good stock for next 3-4 years.

Disclaimer: Invested around Rs 80 and constitutes around 8% of my portfolio.

This is not a stock recommendation, please do your due diligence before investing.

I believe it is due to hype surrounding advanced carbon, which is an important component for Li-ion Batteries. Share is being traded at P/E multiple of 80, which even after factoring in FY19 expected earnings, is too high. I think its unsustainable.

Hi @manmohit, As per my understanding, the last 12 months P/E is only 57. Also, if the company can just repeat its Q1’ FY18 EPS of 1.2 for the remaining 3 quarters of FY18 also, the forward P/E after Q4’FY18 can be calculated as 33, assuming that, the price just stays at today’s price of Rs. 158.

I think, there are two aspects to the rally which we are observing these days. One is, as you mentioned the hype (may be, half hype and half reality) surrounding advanced carbon and also the other products in HSCL’s portfolio. Second reason (a more generic one) is that, we are already in a strong bull market (as per my belief) and market is ready to take more risk these days, especially on quality micro/small/mid caps, hence willing to pay more premium. Why I believe so? I have tried to address that on the following discussion thread for another stock:

I beg to disagree with you. It’s a commodity business and there’s no doubt about it. Its performance can be solely attributed to the revival in the end user industries such as Aluminium where the capacity is going to increase in the coming years. The performance of Hindalco, and Vedanta is a testament to this fact. Their investor presentation explains all the points succintly.

Please have a look at this excellent presentation on commodity plays which says that PE should not be looked at in the case of such companies. comm-170930033445.pdf (145.5 KB)

Also, we cannot ignore operating leverage which comes into play at higher capacity utilization levels (expected to reach 90% this quarter for HSCL). Please go through this excellent write-up by Micheal Mauboussin to understand the power of operating leverage. https://www.valuewalk.com/2016/06/michael-mauboussin-operating-leverage/

I understand that chemical’s sector will grow in India very well, what I don’t understand is the trend of upper circuit in every other chemical/carbon stock, I don’t know weather to enter or not into any script at the moment because almost every chemical/carbon stock has moved 100% some even moved 400% in 3months.

Any advice from the experienced investors ?

HSCL to consider raising funds in its 2nd November meeting:

The Board of Directors of the Company at the ensuing meeting to be held on Thursday, 2nd November 2017 will inter-alia consider the following agenda:-

Raising of fund by further issue of securities by way of Preferential Issue/ QIP / FCCBs / FCEBs / ADRs / GDRs subject to the approval of the Shareholders and other authorities as may be necessary.