This thread is pure gem.

Blue Ocean Tools and Execution- Strategy Canvas, Attribute Analytics

As we discussed last time Blue Ocean stems from the idea that there are opportunities in each industry to move from ultra competitive battles around price and features (red ocean) into a new market reality where our competitors are either non-existent or irrelevant.

Great, how to go about it- Five steps

- Creating a strategy canvas template

- By raising an attribute

- By reducing an attribute

- By eliminating an attribute

- By creating an attribute

Step 1 : Build a strategy canvas

This is the fundamental cornerstone of Blue Ocean, this provides a overview of our business and products stack up against competition. As Kim says it serves two purposes. First we can know the current state of play . Second understand where competition is currently investing, the factors of competition and competitive offerings.

List the products or services, if a commodity or standard product we can segment like domestic, import. If niche product area list the name of competitors or even the product names.

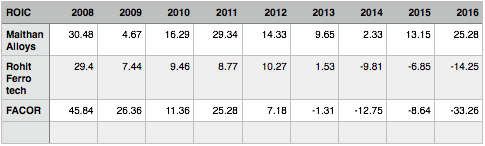

List the attributes or factors of competition on which industry is competing. I have attached a file for a commodity company Maithan Alloys (confession- invested and biased). You can include value proposition to customers like speed of service/delivery, quality etc.

Rate each competition factor for company and competition segments. This should throw up where you are currently stack up.See the file attached, I am appending narration to understand better. Don’t boil the ocean on exact numbers, if you understand the business better you should be able to spot the number easily.

Step 2 to Step 5

If you need to identify a Blue Ocean we need to look at four elements within existing strategy canvas.

Raise an attribute- enhance the standard of an attribute to enhance competitive edge. For example memory storage, camera etc addition to mobile phone.

Reduce an attribute- reduce where unnecessary or unimportant. This helps during time of disruptions. For example my wild imagination says after Reliance Jio the incumbents shouldn’t worry too much about the open network drama, practically its a customer support tool nothing more.

Eliminate an attribute- eliminate altogether, remove owned applications which are not required by incumbent tele operators not generating revenue. Or say SD card slot, it’s not game changer any more. Microsoft removed giving cd with software purchase.

Create an attribute- suppose you can choose your tyres and ancillaries while buying a car.

Commentary for Maithan Alloys (canvas attached in excel file). few more will update later, need to make it user friendly; more of abstracts now).

Strategy Canvas

Maithan Alloys. Strategy Canvas.xls (33 KB)

Mathan has able to manage move ahead in:

- uninterrupted power by taking grid lines from electricity board (comes with additional security deposit, superior cash flow gives head room).

- capacity utilisation is currently around 90% plus against domestic number of 54% (this is partially done by not expanding capacity further, backed up long term contracts than auctioning price, focussing on operations than selling raw materials).

- capital power (only company in alloys near debt free, high cash flow allows the timely management of working capital which is a significant portion of Industry)

Value element alignment of Maithan Alloys

Raising an value driver: Dedicated grid supply (easy to replicate once cash position improves for others).

Reducing an unwanted value driver: mix of backward integration and purchase than complete backward integration. Maithan is one of early player to tie up with small time raw material providers as on required basis rather leasing mine always. (dependency on import unlikely to reduce for all competitors due to high quality of ores available abroad). (time bound replication, building network require sometime).

Eliminate an unwanted value driver: None

Create an value driver: Custom tailored made product due to varieties of steel grade required (time bound replication as building prototype with different manufacturing processes, customer acceptance takes cash and money muscle).

Blue Ocean also includes heavy load section for putting strategy into work and the change management around leadership. But to my opinion more helpful for the execution of strategy than knowing “edge” of company which can protect earnings into deep future which is our sole aim. In case you are interested you can hole them out from their website for further understanding.

What we should be clear is :

- Prepare a strategy canvas (this is not easy unless you understand the business to a reasonable extent).

- Analyse the attributes and find out where your proposed candidate is demonstrating an edge.

- Spot the value alignment (what is the extra company is doing, the attribute…see above).

Competitive landscape with strategy canvas provides a deep insight to business model of company and helps in assessing future earning estimates and cash flows along with adjustments. This augments further whether financial metrics are reflecting the strategic advantage and document specific competitive advantages down the line. I will post the interconnected points of financial metrics, narrative based competitive advantage for this company as soon as I get done.

Good wishes and happy investing!

- Disclaimer- the understanding of stated company is for illustration purpose only based on my limited understanding of financials and business. I have not discussed with management and not necessarily reflect exact and true picture of company.

5 Likes

Practice notes on Competitive Landscape, competitive advantage and interlock business strategy

Few days back we discussed about how business strategy and competitive advantage are interlocked and an approach how an investor can unlock these concepts. Why are we doing all these things , basically to genuinely find out a company having advantage or edge over others. So that it can satisfy our basic requirement of sustainable growth and profit for a long time.

As times are evolving single method like Porter five force are inadequate though it helps a lot. A traditional five force doesn’t reveal new mega trends (as the identification process doesn’t depend on a market share and ROIC), or a uncontested market place for same reason. What I currently do for a company:

- Build a business model description (by using a canvas or abstracts what ever you feel right). But this must provide information on the entire value chain of company like a. the business and market segments b. value proposition c. distribution channels and marketing methods/CRM d. Cost drivers & structure (resources, infrastructure and activities), key revenue streams and partnerships. I like Business Model Canvas though I don’t think it reveals a lot about business strategy but nevertheless a good start. Don’t worry about a great deal of details, a basic understanding is required.

- Gather information key strategy assessment and those are a. market forces b. industry forces c. key trends d. macro economic forces. This is just preliminary information gathering.

- A strategy canvas (please refer to the post), this brings back focus to those key competition factors.One practice note I used in earlier post.

- Check whether industry falls under a growth trend or Blue Ocean even. Traditional five force like switching cost, entry barrier doesn’t carry a lot of relevance to Blue Ocean industries as these are created in new waters without having competition records or peer comparison. We did a value alignment last time which can confirm whether company falls under Blue Ocean or not.

- Blue Ocean companies created by expanding red ocean always prone to competition. Build a competitive landscape, and see the company positioning to landscape (this brings us back to Porter five force).

6. Identify the existence of competitive advantage, mindset of edge, and sources of competitive advantage.

7. How does the competitive advantage impacted the value chain and more importantly PL account.

8. Can we identify key business strategies that are taken by management which resulted a better value chain and PL.

I always felt by bringing in mega trend/Blue Ocean with a traditional competitive advantage identification converge both new and old world. Of course the challenge lies in spotting end to end chain of activities, no wonder it’s an iterative process and improve with more practice. Understanding a business , it’s edge and the strategy build around by management has become a pain for me over the years. Whenever I took short cut by identify few terminologies here and there it never assures. Of course at the end of day all these can go wrong, but not the learning. ![]()

Anyway my focus is point no 6,7 and 8, I have made them bold. This is my yesterday’s practice note for 6 and 7. That is a competitive landscape, source of competitive advantage, value chain and PL drivers. The point no 8 business strategy, a prototype I am building….will paste here once I complete. Example and disclaimer remains same- Maithan Alloys.

Competitive landscape of Maithan Alloys

A. Industry Map (please see attached excel file for the map)

Iron ore is raw material for steel making, when iron ore is feed to furnace alloys (like manganese is introduced as additive). The major three segments for Industry will be 1. Minerals and Ores (for iron ore steel manufacturing companies also own ore mines but for manganese ores its comparatively lower as it’s dominated by MOIL). In both iron ore and manganese ore there are many smaller players due to leasing by different state governments. 2. Alloys manufacturers (those who manufacture alloys by using manganese) 3. Steel manufacturers (end recipient of product).

In ferro alloys sector baring TISCO there is not much overlapping name who manage end to end. Though iron ore and steel manufacturing owners are common. A number of small players exist in each market segment. But a chance exist where steel manufacturers aggressively integrate backwards i.e. start manufacturing alloys as well.

The buyers/customers are big player (steel manufacturer) who influence the pricing , also due to a fact commodity type of product. However the cost of ferro alloys is barely 1% of steel need and a core requirement for production.

Despite of high number of suppliers, a couple like MOIL manage the bulk supplies, however with import available and auctioning price suppliers are not a major threat.

Although there is little barrier of entry, the negative margin and return on capital discourage new entrants.

There is no substitute products for ferro alloys.

The rivalry within industries is intense, this can be seen in lower profitability. The rivalry resulted lower cost to buyers.There is a high exit barrier, undifferentiated product making competition tough. Being a cyclical industry capacity often gets added in boom period leaving over capacity when downturn starts.

B. Identification of competitive advantage

The present capacity of ferro alloys industries in India is around 5.15MT with a 3.16 Million tonnes for manganese alloys. There are more than 100 manufacturers with no clear leadership. Hence leadership stability doesn’t reflect much as margins of lead are thin and fluctuating.

Industry return on capital is getting dismal with negative, post cost of capital it will be more miserable. Where as Maithan has demonstrated a decent number though it has fluctuated.

C. The Source of competitive advantage

Chances of captive customers- in absence of switching or search cost it doesn’t justify a strong case. What may make a case is value added products due to nature of different grade of steel. This may be binding customers.

Cost advantages- there is no technology or asset related advantage in industry. The cost advantages due to operational efficiency covered separately.

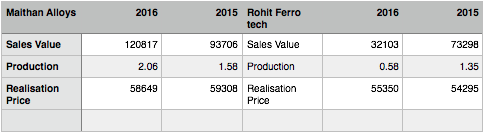

Economies of scale- 2016- 206178 tonnes, 2015-157920 tonnes. Operating cost has come down from 92% to 88.5% which is a major improvement.

Profit due to government intervention- Maithan has been availing direct and indirect tax incentives for it’s Vizag unit.

Maithan provides tailor made products, but whether that added to pricing power need to be analysed. Economies of scale is working in favour with value add product can work in favour of company. There is also temporary boost from tax incentive. Apart from this profit power may be coming from operational efficiency.

Mindset of Maithan Alloys

- Maithan has targeted to generate higher return in terms of capital and margin than producing more and more. Clearly the focus is on profits than having market share.

- Rather targeting best customer, Maithan has reached out in terms of diverse needs of customer i.e. tailor made product.

- The innovation can be seen when management has tied up with small vendors than playing in ore markets, buying power grid and making asset light avoiding captive power consumption.

Value chain and P&L of Maithan (please see attached excel file)

A. Relative Pricing Power

Though Maithan is enjoying a minor price advantage its not significant.

B. Relative cost power

Lower operating costs or using capital more efficiently including working capital.

Facor alloys though have a higher operating margin than Maithan and Rohit inventory can play spoiler.

On a working capital front Maithan is a clear winner with superiority over receivables, inventory and payables.

C. The Value Chain Analysis

The key areas of value chain leading to customer value will be supply chain management, operations and sales & marketing. This is why:

Supply chain management- all about procuring raw material in time and delivering to customer in time. Imperative to have a quicker delivery time both side either by getting close to customer location, vendor location or owning a strategic asset like mine for ores. No wonder most of alloys manufacturing stays close to steel manufacturers geographically unless you are an importer in high quality manganese ore which is not available in India.

Operations: despite a standard production process, quality and customisation plays a specific role due to alloy adds to quality of steel and different grade of steel requires different composition. Apart from this getting power in time points why operation is important.

Sales & marketing: although you have a specific customer base (only steel industry) the over capacity in industry coupled with direct imports creates a need for better marketing skills.

Maithan vis-a-vis industry value chain

Within scope of supply management Maithan has reached out small mine owners and partnered with them. The partnership cost them bit funding, knowledge transfer and robust cash flow supported them. Other key aspect is Maithan is not involved in raw material trading to garner speculative profit. I would say stay to core competency.

Tailor or custom made product is a major value enhancer as the different grades of steel are becoming diverse. This reduce the quality testing and further refinement by steel manufacturer reducing their cost. The custom made product again requires some time to get accepted by customers. This may work as entry barrier.

Maithan has focussed on long term contracts where both price of raw material and end product are speculation driven i.e. market based price. Though it has not brought any additional pricing power which saw in pricing analysis but they have been able to fill orders and use their capacity which in turn reducing the fixed cost per unit.

Power is a significant cost for the industry, due to power shortage on line supply most of manufacturers have set up their captive power plant. Maithan on other hand bought grid from power board and reduced capital spending and more importantly asset light without maintenance. We can see a significant improvement in power cost , Maithan is spending around 26% of sales as power cost against competitor spending around 40% of sales.

When you read together strategy canvas and value chain together it will clear how PL is connected with business strategy.

Attached a working file, let me know questions if any.

6 Likes

Excellent coverage. Easy to read, easy to understand, easy to work on and easy to implement. It needs great worth to put complicated topics in an uncomplicated words and manner. Sir you have achieved it. Let god give you immense energy to keep us updated and let you increase the value of this forum.

The Strategy of Having a Concentrated Portfolio

Moving away from bit of continuous stuff on stock analytics, this was something I was discussing in my group couple of hours back. Couldn’t wait more to share post meeting.

It has been an eternal debate whether to have a concentrated or diversified portfolio. One section believes diversification means diversifying the risk, hence it’s better off to manage a big carnage. On the other hand second section believes diversification stems from not knowing, if you know everything about a company (which is available at good valuation alongside better earning prospects) then why other company is required even? Chalo, at the worst case another 3-5-7 companies. And even with wide diversification how come 50 bad companies together create wealth? Approach to concentrated portfolio became a ran away hit term with time as Mr Buffet keep emphasising.

First and foremost no matter however we discuss we wont get a concrete answer to this question, the irritating and common excuse again is “specific to individual”. But I want to get in those attributes what one should be aware before thinking of a concentrated portfolio.

In common parlance we understand concentrated portfolio as:

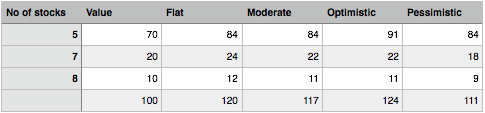

20 Shares market value- 100, 5 of them -70, 7 having -20 and balance 8 have 10 bucks market value. Basically we are saying the value of portfolio is focussed to few stocks. By doing this what happens?

See the below table:

This is a favourable outcome where we are expecting our big stocks (in terms of value) will out perform others. If price goes for all of them by 20% then it becomes 120, take this as base; 20% return for us. If big stocks appreciated by 20% and smaller ones goes up by 10% my return falls to 17%. If I take optimistically 30% growth for big boys and 10% for small then my return moves to 24%. If I become pessimistic with a negative growth rate for small ones and 20% positive for big ones my return fall to 11% but negative. The key message here is if a small number of stocks properly selected and out perform, even with so many mistakes with large number of stocks we can still deliver positive return. But the big assumption these concentrated stocks need to perform, now what happens if they don’t perform.

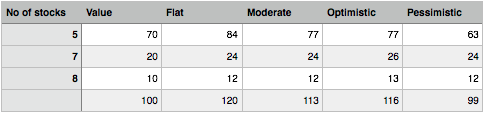

This is the table where small ones perform better than big ones, we can see even return can plunge to negative in a pessimistic scenario against positive return of 11% in the first table. That’s a whopping difference of 12%, this can do wonder as compounding marches on.

Fair, drawing fine lines:

- A concentrated portfolio accelerates CAGR in turn creates wealth faster. Easy and simple.

- Negative CAGR in market turmoil or even a carnage can be minimised when times are running bad. And this is a huge plus for long term investors who can minimise the negative CAGR.

- Pyramid becomes easier i.e. adding positions on shares which prices are rising. You need to allocate capital on few winners (rather having a large population) and this is very helpful for salary earners.

- Even minimum error in selecting a stock will push you to a negative CAGR. And every negative CAGR you need more force to recover next year making challenge higher. It break few people to lower down the expectation. Negative CAGR is one of worst thing than can happen to an investor.

But these are arithmetical probability of concentrated portfolio. What about scenario planning, we all know neither market is linear nor index is static.

Scenario 1: 5 stocks today have 70% market value of portfolio, after 3 months plunged to 30%. How you are going to react assume you don’t have to deploy additional capital? Are you going to sell profitable shares (smaller ones) and consolidate again? Or you maintain reduced percentage thinking they will come back, then where is value based concentration?

Scenario 2: the concentrated stocks fundamentals plummeted without a correction in price. It justifies value base concentration knowing fully concentration will collapse soon. The smaller ones are still fundamentally solid.

Scenario 3: Smaller ones prices are rising distorting the concentrated values. How you are going to react? By selling them and adding further positions to bigger ones.

Honestly speaking an investor having concentrated portfolio shouldn’t bother about these situations. But only after knowing what is concentrated portfolio. The concentration is not build around value which is a market variable subject to wild gyrations.

Key attributes of concentrated portfolio

- Circle of competence: one must develop a strong circle of competence before even thinking about concentrated portfolio. One of major signal of achievement when you can start saying “I don’t understand this business”. This is the first and key attribute of concentration. Once upon a trading stock became 13% of my portfolio due to price rise, immediately I removed the amount from calculation.

- Clear differentiation: You should able to tell very clearly the concentrated stocks are superior to other ones. Either a strong competitive advantage, super business catalysts etc. Once again the testing line would be you should be able to say “my company A is better than company B and I know why, documented as well”. Larsen & Tubro and Punj Lloyd both looked attractive once upon a time, which led me to doom.

- Period of differentiation: some differentiation exist for a longer term like network effect companies where as few enjoys a cost or regulatory protection for a shorter period. You must be able to compute prospective concentration for a specific period. E.g. till 2019 my 5 stocks will continue to be in concentrated, by 2018 I must replace 1-2 stocks. Symphony was a great stock for me, but this time I was sure of a s shut down point and move accordingly.

- Never ignore valuation: you might have great companies as concentrated portfolio but at higher valuation. This though is quite normal as my best companies should be fundamentally sound, who cares for valuation gap. This may impact your CAGR materially, people use a mix of value gaps and value rich but fundamentally steady. Gillette is a great company but I was getting Marico at better valuation.

- Treating growth stocks: catch 22 situations whether to include growth stocks in concentrated portfolio. One of major attributes of concentrated portfolio is less volatility as we are looking to long term. When Wim Plast was blasting away I thought what will this plastic company do, I never added positions. Wim Plast ran like a horse leaving my CAGR behind for showing disrespect.

- Never ignore risk: concentrated portfolio shouldn’t include stocks which are politically or externally risky.I haven’t faced such situations till date.

- Gradual vs immediate sale: when market going downwards immediate sale can prevent downside and free up funds for reinvestment or wait. This is always problem for me as generally I go for one shot sale. With high concentration it can create a benefit or loss, say if the market is going upwards.

I didn’t want to include the common acts like long term investing, good management etc. The concentrated portfolio requires more hard work and documentation, update. Please keep on adding, I may do few more once it hits my mind.

Recently I red a book called “Concentrated Investing” by three authors. This book focus on few investment philosophies of highly respected concentrated investors profile.

5 Likes

Peeping into Business Strategy of Company and connecting with competitive advantage (with Practice Notes)

Once again with no uncertain terms I am invested in Maithan Alloys. Around 4% (Currently a lower band stock ) of core portfolio is Maithan, and one of few stocks I am buying these days. If you find positive bias in notes make sure to discount accordingly. But my average price is 91 rupees with a holding period of 18 months average. The current market price may have factored some of advantages we are discussing apart from risk being I am terribly wrong.

Another important note- this may look like a lots of work to do, in reality its 1 page diagram and 2 page notes to crack the business understanding, a growth trend, competition and advantage. Another additional page noting down the company’s business strategy. As I am writing on a public forum, I am expanding the narrations for easy understanding.

Last time we discussed:

- what the competitive landscape of industry and positioning of the company (in this case Maithan alloys)

- how to identify competitive advantage and source of competitive advantage

- mindset of company in managing the competitive advantage

- the value chain of company and impact on PL Account

The last piece in this series is to know , “what are the strategies company is taking which achieved this competitive advantage?”. And in the process it helps us to know:

- how easily the strategy can be copied or imitated by others

- risk propositions while taking trade offs to move ahead in value chain

- too many competitive advantages are dangerous and may not be true. A decoupling activity, few activities of value chain support competitive advantage. So if a complement activity needs to be decoupled and fitted with another should be easy to do rather than dismantling entire value chain.

- consistency of strategy for few years

Business Strategy response by Maithan for value chain

Difference in relative price or relative costs that arises because of differences in the activities being performed. If a value can be delivered without a differentiated value chain its simply not sustainable competitive advantage.

Strategy means deliberately choosing a different set of activities a unique mix of value.

Test 1: A distinctive value proposition

Choices about the value company will offer to customer and whether choices are made consciously or not. Customer, needs and price for it.

Customer segment is steel industry for improving their quality of product depending unique grade of steel. Now is this defying a traditional demographic segmentation by customers? What I could spot is most of steel manufacturers are spread across near raw material need and accordingly alloys companies have positioned themselves. Hence Maithan is present both in east and south.With a commoditised industry price is seldom decided by negotiation rather more demand and supply from industry. Hence Maithan and other’s price positioning remain same and will continue to be same. But customers wanted specific ingredient than experimenting and re-work on standard product delivered. Maithan has been successful in delivering same.

The industry is notorious;

- Suppliers are powerful specially labour unions and power suppliers like government (apathy well known).

- Customers are powerful too as they themselves are struggling and price sensitive.

- Rivals fight on fixed cost and operational efficiency by using capacity.

- New entrant can jump in anytime and entry barriers are low.

- Substitutes are not a problem till date.

As prices are not negotiated much Maithan tried to position itself on customer’s need by offering customised products.

Test 2: A tailored value chain

A set of activities to meet customer need:

- The niche or custom products are not technological superior but additional cash flow is allowing to amend standard manufacturing process and deliver customised product.

- The cash flow is organic by taking few operational decisions such as purchasing power against captive power consumption. Avoiding trading in raw material. Fulfil raw material requirement through a mix of buy and own.

- A customised product requires multiple acceptance from customers, even with additional cash muscle competitors would require some time to replicate what Maithan is doing.

- My positive thinking comes from a fact if others are not able to do with same manufacturing process perhaps differentiated manufacturing process is also helping.

Test 3: Trade offs

The clear trade offs are here is 1. Buying grid power 2. Avoid trading in raw material 3. Amend a standardised manufacturing process for customisation.

So if power grid becomes a complete failure it can adversely cost structure, similarly a favourable raw material price can bring speculative profit. And if you can not cope with extent of customisation you may need to call back the entire process.

This trade off may be coming from:

- one set of alloys performance is poor than to others where customisation is helping.

- perhaps smaller plant at Vizag is created to cater this customisation rather than running a big size plant like Bengal one.

Barring acceptance of customers on amended manufacturing process other trade offs can be imitated.

Test 4: Fit

Let’s pick up tailored activities of Maithan.

- Customised product

- Mix of buying and owning raw material sources

- Buy power than own and create captive power

Though customised product shows up as a competitive advantage the other two activities like decision on raw material and buying grid power providing the muscle power to create advantage.

If we see clearly all tailor made activities are consistent with each other. If value proposition is a customised product then other two activities are not destroying but supporting it. The activities are complementing each other. Think about a reverse situation, we have small requirement of tailor made products and plant is accustomed to produce in large batch of productions!

Maithan has focussed on its core competency i.e. smooth production resulting to good quality and customised product. It has shifted away from owning mines , trading in raw material even captive power plants. Whether this gambit has played off, we need to confirm more from financial metrics (coming soon).

Now if a competitor needs to imitate Maithan then it has to create organic cash flow either by taking bold decisions or operational efficiency in a standardised environment to meet a customised product need.

By choosing not to trade in raw material inventory glut can be avoided in an industry saddled by over capacity.

Test 5: Continuity

By reading annual reports together with research reports company has adopted the tailored value chain at least since 2011. It may be helping:

- building brand and reputation and customer relationship

- helping suppliers for contributing to competitive advantage

- improvement within activities and build further unique activities

That’s bring an end to business strategy and competitive advantage. Ideally next step should have been to hunt these advantages and trends within financial numbers. Unless numbers shows up the strategy is meaning less and becomes prophetic not profetic.

But before relying financial numbers, I love to test two more things:

-

Business to accounting- most of cases we rely on the annual/quarterly accounts thrown to us. I am not saying discard them but let’s understand first whether accounts shows reflection of business. Whether key business processes having a financial impact has been accounted? This will further segregate what enforced activities (must do) and voluntary activities (good to do).

-

Creative accounting practices- accounting is a cauldron of realities. Ask any practitioners, it’s a myriad of situations and scenario planning. We should try to identify “adjustments required to financials” before relying on financial metrics and other ratios required going forward. I would like to emphasise here, creative accounting has little relationship here with forensic accounting. First creative accounting practices are within regulatory framework, second there is no mala fide intention of fraud, third the intent is not to hunt down for evidence which is a mandatory requirement for forensic. Hence if an accounting policy has changed even distorting financials wrongly it’s still not forensic accounting. Siphoning away of assets, policies adopted by management prejudicial to the interest of share holders (which are not allowed by regulators from first go), conflict of interest which over rides memorandum or article of association etc are few examples of forensic. Wrong accounting becomes a casualty of mala fide intention in case of forensic accounting. Frauds are not easy to be identified, requires special set of tools and analytics and more importantly access to abundant information from company (retail shareholders will never have). Some time down the line, I will use few forensic topics in one of my old thread (possibly few of my old consulting experiences in forensic assignment). Fraud, break down of internal control environment and forensic accounting are related subjects.

Once again thanks to valuepickr, I could able to complete few work which was pending for some time due to laziness. Appreciate the forum’s help.

2 Likes

First bit of apologies if some of these topics sounded academic heavy. I didn’t have a choice; rather than posting the summary I opted for disclosing backroom workings. I don’t mind to admit , I have been fairly criticised in my own group for some time going bit far. I am no way justifying every bit of analytics would influence a stock selection or judgment (after all we put money to stock market to earn more). But if you give me a choice to express I have always felt it’s ABSOLUTELY not easy to understand a business, more so with changing demography, delivery channels, customer preferences etc, the wheel of understanding has been circling too fast.

It took years for me to learn some of these things, some one stood like a rock and teacher (My revered Guru) to handhold a myriad of conflicting, boring and painful things. That includes even I was scolded, reprimanded and literally punished more than dozen of times (like no access to group unless you complete this. )

But today I don’t hesitate to say had that not happened perhaps I or others associated with my Guru possibly could have vanished from stock market (tormented, bruised or even financially killed!). Unfortunately for an average person like me I had no choice but to unlock these heavy hand approaches with efforts and patience over the years.

My guru has done a lot for me before departed for heavenly abode, I always felt an obligation to replicate even 1% of what he did. With no uncertain words reach out to me if you have questions, more than happy to answer.

Today I will try to get in:

- How to draft an accounting framework for company and compare with published financials

- Run a mini ERM- Enterprise wide Risk Management to understand key risks faced by business

This would help in spotting ratios, numbers and risk management which is a key driver of business and management performance.

Wishing you guys all the success.

6 Likes

Business to accounting

It’s the business which drives accounting not the other way round. So when we start with an annual report I felt lot of times building of a business story in mind in tandem with financials disclosed in accounts/AR. For example, once I saw purchase of trading goods is a big number in financials, but when I red the business and look at peers I wasn’t sure why this fellow is indulged in trading. It turns out to be jacking a big number of revenue to catch some eye brows, off setting the massive losses that has resulted from key revenue streams with trading of goods (with 60% plus related party transactions).

The inverse thinking or reverse engineering is once you develop a business understanding build an accounting framework. It’s bit tiring for non accountants, but easily doable. I would like to highlight few old posts which talked about meaning and definition of financials including key accounts and disclosures, principles etc.

Example and disclosure remains same, Maithan Alloys.

First the “seedhi” soch (straight thinking):

- Maithan needs raw material to produce alloys.

- Requires plant & machinery, land/building for production facilitation.

- The key ingredients other than raw material for production, quality check i.e. power, labour.

- A logistics system to deliver the alloys to customers.

- Corporate office for book keeping, HR, strategy and all other corporate function.

- Sales and marketing office to manage direct marketing if any.

If you see strategy canvas earlier we discussed, absolutely in line with key attributes. If you see the competitive landscape you will realise some competitors are doing differently. Their accounts will not be same as Maithan Alloys like trading in raw material (a big chunk of trading profit/loss you will find along with operational revenue). Now I leave a question for you on peer comparison.

Second the tedhi such or reverse thinking:

- what was the preliminary expenses that were written off to build the plants (difficult to get old ones, new plants like Maithan’s vizag should be easy.

- heavy hand of management, what is the opportunity cost foregone to build the business.

- advertisement and marketing expenses spend over the years which yielded results or non results (not expecting much being an intermediate products).

- was one time benefit like tax, fixed asset subsidy heavily build into business making? this would have developed a biased financials with incentive.

- few others like quality defect etc difficult to get, I am ignoring.

Third and last yeda such (orthodox thinking):

- How company is funding fixed assets and working capital?

- what are trade off available against key drivers (say for power buy vs own and generate)

- how I am managing margins short fall if any (absence of pricing power)? (say paid through additional capital?)

- are my asset maintenance heavy?

- have I ventured out like acquisitions and subsequently written off a great deal of money? This is actually positive, it could have impacted badly but management wont repeat again!

- am I subjected to high skilled employee requirement and why?

As I mentioned in my post, don’t worry about completeness. When you build prototype (meaning all dynamics infused and again challenged) likely gaps should come out before final product.

Now think about financials of Maithan Alloys:

Enforced activities (no choice, must to do):

- Raw material, power, labour, sales, logistics accounting.

- Asset funding, working capital funding accounting.

- Support/corporate expenses to the reasonable extent.

Voluntary activities (optional):

- Trade off decisions

- Business restructuring decisions (amalgamation, consolidation etc)

- One time decisions (discontinue product/operations)

Possibility of non disclosure:

- Expenses written off on various accounts (advt, preliminary expenses, R&D, promotion etc)

- Unsuccessful business restructured

- All wrong one time decisions

- Convention other than historical cost and other accounting practice (like land at cost value, decision not to write off inventory/debtors). This is what we need to hunt from creative accounting practices.

Non disclosure of information is the most difficult part to achieve. Don’t blow your head off for accuracy and completeness. An intellectual estimation or guess is all required than absence of estimation.

Can you spot some of the impact of these things:

- All the ratios you are calculating can be terribly wrong. For example inventory turnover where 25% of raw materials are obsolete and disclosed but not taken to financials. We must identify and adjust these big ticket numbers and that’s why I said earlier the objective is to find “adjustments required to financials”.

- Either over stated or under stated book value (land bought in 1967 never revalued) leading to gross mistakes in reproduction value of assets.

- Serious errors committed by management like failed business restructuring (I would like to see if it’s a hired hand he should be asked to march out).

- Auditor’s reluctant disclosures. Auditors are always caught between integrity and profit, they don’t want to upset client ; at the same time can’t compromise on certain auditing standards. Most of them they choose a middle path i.e. disclosures and note to accounts. These two unearth wealth of information.

Fair, lets get back to our work.

Now we know what Maithan’s account should have, lets get into 2015-2016 annual report and peep into it.

Maithan Alloys Balance Sheet and Profit & Loss

Share capital and reserves: nothing usual, a bonus issued in 2015. Long term borrowings: a foreign currency loan on mortgage of Vizag plant for the sam plant ( I guess cheaper cost of capital). Deferred tax liability (accounting treatment of taxes due to tax books and financial books).

Long term provision- employee benefit for gratuity. Short term borrowings - a working capital loan against hypothecation of goods, plant and other fixed assets (combination of rupee and foreign currency loan). Accounts payable- business as usual.

Other current liabilities- maturities of long term loan (why?) and others payables of 103 Cr (not known). Short term provisions- again employee benefit (may be bonus).

Fixed asset- a lots of tangible (land, building, plant, vehicle etc), intangible includes software and good will (indicating an acquisition of company). Point to note, these good will again are accounting treatment, seldom have no reproduction value.

Long term loans and advances include deposits , Current investments- mutual fund investments

Inventories- again big raw materials, spare parts etc.

Trade receivables, Cash and bank balances, short term loans , other current assets, revenue (only sale of products), employee benefit, power cost, finance cost, depreciation, other expenses (big ones include stores, repairs, freight, export expenses).

At first look nothing unusual to business but as they devil is hiding in fine details. The reverse thinking and orthodox thinking is a combination of business performance and creative accounting practices to unearth. Creative accounting practices, lets tackle it separately. I will rather focus on visible things for now, key points for consideration:

1. Bonus issued in 2015 (capital allocation decision)

2. Amalgamation somewhere and good will account

3. Foreign currency loan to minimise cost of capital?

4. Probe further on break up of other payables and classification of long term maturity within current liabilities.

That’s a very short and sweet list to start with. The possible financial adjustments will come by reading notes, directors/auditors report, and accounting policies. Lets cover that off in creative accounting practices.

For now, I will jump to Risk side.

Risk Profile of Company

Well these are business risks emanating from decisions taken on area of financial reporting, strategy, compliance to rules and regulations and operations of business. This has nothing to do with stock price risks.

A very good tool to know the risk profile is application of ERM or Enterprise wide risk management. But at same time next to impossible for a retail shareholder to do an ERM assessment sitting outside with minuscule information when company themselves are struggling to implement ERM. But an mindset towards ERM will help to have again best estimate on available information on the risk management capabilities.

Under ERM framework the objectives of company are split to 4.

- Strategic- high level goals, aligned with and supporting its mission

- Operations- effective and efficient use of resources

- Reporting- reliability of reporting

- Compliance- compliance with applicable rules and regulations

To understand whether company has fulfilled or attempted to achieve these objectives one needs to understand eight components.

- Internal environment- tone of organisation and set the basis for how risk is viewed and addressed. This include risk management philosophy, risk appetite , integrity , ethical values etc.

- Objective setting- a process in place to set objectives which support mission and risk appetite.

- Event identification- internal and external events affecting the objective must be identified. This can create either risk or an opportunity.

- Risk assessment- risks are analysed , with likelihood and impact. Assessment of both inherent and residual risk.

- Risk response- avoid, accept, reduce or share the risk.

- Control activities- policies and procedures are established to help risk response being implemented.

- Information and communication- information is identified, captured and communicate to people to carry out their responsibilities against control activities.

- Monitoring- independent guys assess the effectiveness of ERM and suggest for modification.

(For detail google COSO-ERM).

Under claus 49 of listing agreement all our companies are suppose to identify risks, quantify them, build response and identify failures, report and audit. And COSO_ERM was a suggested framework. But this never happened in true spirit, risks are disclosed as style statements and copy paste than reality.

But not everything bleak and dark. There is a limited way to crack this unusually complex framework. Of course to the extent what we require and to do that we need to know how a ERM is performed.

- The risk you see in annual reports are not some sort of casual discussions within management members and then paste it to AR.

- Every company should carry out a formal risk management plan , establish risk appetite and all other components of ERM documented. The documentation is called Risk register and controls identified against it are tested regularly for effectiveness.

- Every failure that resulted in risk register must be reported a host of people including auditors and regulators.

Now the problem is a lot of risks are subjective, regulators do not have band width for a water tight implementation. That leaves the auditor to hold the quality, I hope recent IFC will enhance the process further though a long way to go.

How do we spot key points for risk management for OUR NEED?

First it lies within the strategy value chain. Lets give it a shot for Maithan and compare what management has written in AR.

1. The biggest risk for this company is assured production backed by sales to cover it’s fixed costs. Or else within few years it will vanish. We can call at “UNUTILISED CAPACITY”.

2. Quality of product is poor. “QUALITY RISK”

3. Next is if you can not fund working capital and fixed capital for a company with high fixed cost again net worth will erode quickly. Lets call it as “CAPITAL RISK”.

4. Moving on one must stay close to customers and vendors here. “LOCATION RISK”.

5. A substantial portion of company revenue is exports, need forex risk to be managed. “CURRENCY RISK”.

6. With so many operational efficiency requirements, back up to key management members is important. “SUCCESSION PLAN”.

7. Unavailability of raw material and power can jeopardise the operations. I will call rather “INPUT AVAILABILITY RISK”.

8. Compliance to labour laws, internal controls, and tax laws. “COMPLIANCE RISK”.

From a strategic perspective substitute products, tailor made value chain we have already analysed earlier. Not repeating them.

Now lets see what management is saying:

1. Industry risk (sector volatility)- nothing but unutilised capacity

2. Quality risk (poor quality)

3. Competition risk (no entry barrier)

4. Currency risk

5. Geographic risk

6. Liquidity risk (capital risk to fund operations)

7. Compliance risk (covered generally in audit report, directors report and notes).

Pretty much on same line what we are thinking, except probably to me succession plan and input availability risk.

Have they managed to mitigate the risks, that’s part of performance management. Somewhere down the line for us to explore!

Next step is to sniff the creative accounting practices and that’s fun as well.

Good wishes and happy investing.

The highlighted ones are the only portion gone to my stock refresh document which I am doing simultaneously. half of a page.

4 Likes

An Important Note on Maithan Alloys

Yesterday Maithan has informed stock exchange regarding the AP floods and it’s impact on Vizag plant.

- Management states clearly the plant has been damaged significantly. The plant is insured. but question remains about business disruption.

- Management clearly says there would be again significant business disruptions.

As expected there is a knee jerk reaction to stock price, but I guess by the time I am writing this price has recovered. Anyway price is not our concern.

The reason I am writing is this is not stock proposition I am making to you, it’s part of a explaining a methodology i.e. a case study. Hence obviously no buy or no sell decision I have suggested. Saying that I do understand we spoke exclusively about business, competitive advantage, trade off which creates a differentiated value chain. More so I am yet to get into a proper bear case in this series, hence it appears more positive news for now. Hence important for me to clarify on a forum where people do rely other’s opinion with respect and regards.

- I bought Maithan Alloys around 170-180 (Feb 15 onwards) initially (pre bonus price, effective price now would be 85-90) and I stopped buying beyond 110. The price was paid basis purely reproduction value of assets discarding earnings growth to a large extent.

- Maithan went leaps and bound after bonus issue in fact went past 430. I sold off few post 360 basis a price excessive to reproduction value of assets.

- I still have no doubt on management, their edge. However needless to say this is what my analysis (not opinion!). The same reason again I started buying around 260-270 as the price looked good to me.

Important Point- the value add/niche experiment ,if part of Vizag plant with smaller production batch (this is my understanding) it will affect the competitive advantage temporarily as discussed.

- However considering a dud industry and natural calamity more so with management acceptance. Results may be affected and that’s what an indication from management.

- These days I am operating strictly on stop losses even for core portfolio with holding expectation. I will start off loading around 165 below till 140 if happens. But that would be nothing to do fundamentals of company and doesn’t mean I wont make another entry.

Last thing, have we not captured the risk, it’s part of location risk. But there is no way I could factor the impact to valuation for a natural calamities for the simple reason no company’s earning will look good if you factor a natural calamity (e.g. discount 70% of earnings in case of earth quake- you may wait 100 years with same assumption still earth quake may not happen and we need not get valuation). This is exactly the black swan we need to learn and manage part of behavioural finance.

Disclosure again: I am invested, now you know my buying and selling strategy. I hope my further declaration is in line with stringent requirement of the forum.

To reiterate my research on this company I am starting “creative accounting practices” now. By end of day will post, thanks.

@manish962 is this adequate?

2 Likes

Dear All

I have just reached the stage of creative accounting practices, to complete the journey we need to go through 1. Financial metrics against competitive adjustment 2. Analysis of growth, profitability and financial health 3. Quality of management 4. Special situations 5. Valuation. This is minimum gamut I want to cover.

Post the incident in morning (flood in AP) I am disclosing the extracts of analytics done during initial assessment of Maithan, currently I am doing a yearly refresh. This would help readers why I took the call then to buy. Period- Jan to Apr 15.

- Has the company ever made an operating profit?

Last ten years company has earned operating profit every year.

2. Does the company generate consistent cash flow from operations?

During last ten 10 years the cash flow from operations has been positive on 7 occasions. Once during last 5 years, the cash flow has not been consistent.

3. Are returns on equity consistently above 10 percent, with reasonable leverage? (at least 4 out of years, 15 plus ROE with minimum leverage is a good bet. Cyclical firms may buck the trend).

ROE has been above 15 in last 4 out of 5 years. Financial leverage is 2.72 which is volatility on higher side.

4. Is earnings growth consistent or erratic?

Earnings growth are erratic. 2011- 72 Cr, 2012- 45 Cr, 2013- 43 Cr, 2014- 11 Cr, 2015- 52 Cr.

- Financial leverage above 4 or Debt Equity more than 1- stable business, debt to assets trend, nature of debt.

Financial leverage is 2.72. Debt Equity is 0.66. Not good but also reasonable. Debt is long term debt and working capital loan.

6. Does the firm generate free cash flow? (Free cash flow by sales> 5%), check in tandem with ROE.

FCF is very bad which is way off sales, around 0.5-1%.

- How much “other” is there? (one time charges)

Other income is less than 0.1%.

- Has the number of shares outstanding increased markedly over the past several years? (stock options, issuing shares)

During last five years there has been no increase in outstanding shares.

9. Spot the points from 10 year cash flow, profit loss and balance sheet.

Covered in detail in investment document.

10. Hole the risks, legal issues, competition.

Covered in detail in investment document.

And all other factors related to competitive advantage, tailored value chain remains same. You can see prior posts for detail.

Please let me know if you need a particular detail, the original working file and document is bit voluminous. If I paste everything it will run to multiple pages.

Few more important lines then for decision making:

Allocated capital which has not resulted above average cash flow or earnings. However the company has performed better than peers, with a cycle uptick it may be the front runner to generate earnings.

Maithan is managed by owner operator whose family has been involved in most of key positions. The management communication has not been consistent, heavily centralized management.

The hedging risk has not been mitigated. Customer concentration is not known. All macroeconomic risks like interest rate and inflation affects business. Cash flow has been terrible where operational outflow has been managed via capital inflow. Company enjoys high ROIC compared to peers but not in best league to other industries.

The company is valued 40% over liquidation bet; hence it’s not a knock out safety. However reproduction value is hovering around 40% more than market value. The earning power at higher WACC of 11% confirms a bit of superior management.

Dear suvi,

pardon me if my question is inappropriate, but I am a novice who has just joined this amazing world of valuepickr. This is the first thread I have started reading as this seems to be filled with immense experience and knowledge.

However, before going further the first post of yours where have mentioned that you were advised to stay away from sick type of business includes automobile manufacturers. Can you please explain/elaborate more on the same.

I do understand it includes-

“presence of multiple producers” and “organised labour” as mentioned by you, however it also is a part of the “consumption/growth” story that has been an integral part of India’s economy.

Or does it mean it is just a relatively shorter cycle, ie. 5-10 years as compared to a Bank/Financial institution where money will also be required to lend or to borrow till there is time

P.S- I could be biased towards the automobile industry as I have holding in some Auto manufacturers as well as auto ancillary manufacturers.

and thanks once again to share this invaluable knowledge!

Hi

This is an important question, and thanks for raising same. The quest hunted me so much I am going back to 10 years of Indian history to deep dive into winners of Indian stock market. Preliminary indications absolutely goes in line with what you were saying or what we call cyclical are clear winner. Rest you can read here:

But wealth creation or buying a stock is combination of business, management and valuation. Hence if we buy cyclicals at good valuation or at time of uptick trend it can create good wealth and that’s what has happened in India. So lets get a fact straight you can create wealth still by buying any type of stock.

The thesis here was made on “good business quality”. Commodity type of business will suffer from non-differentiated products, economic cycles (both up and down), lesser entry barriers. Now imagine a company with differentiated products with a brand can sustain earnings for a long time. Problem lies here in india is two fold 1. There are very few companies exist 2. the valuations are steep for such companies.

The best test for you is to see the valuation impact of auto and pharma during economic downtick. Though I would like to request don’t go by growth story much. Growth has to be backed up by economic profit (profit generated by operations minus cost of capital for funding such operations). If growth comes without economic profit it will destroy economics i.e. shareholders, company and banks ; everyone connected with value chain.

Hope it provides some clarity.

Also, the post “the jewels of India” where the mention of luck seems to be really important. have read only the 1st post and thanks for sharing the same. [quote=“The_Confused_Consult, post:74, topic:4814”]

The best test for you is to see the valuation impact of auto and pharma during economic downtick

[/quote]

this definitely makes sense.

Thanks for the clarity. This forum is amazing!

Creative Accounting Practices

Accounting is a reflection of transaction that is recorded by company having a financial impact (note here no financial impact no accounting). A transaction is recorded only when an activity of a business process is initiated, processed, recorded and authorised. Business process is a combination of tasks or set of activities lead to the product or services are delivered by company. So we are saying a lot of activities are grouped to a business process of homogeneous nature. All business process may not trigger financial transactions directly like HR or legal department. Some are directly linked like sales and marketing, procurement etc. The business processes can be out sourced or managed in house. To monitor business processes we need to have board, auditors, regulators and so on.

I spoke about a purchase transaction in past i.e. which stage it creates a financial entry and which stages are not. It also covered the difference between management accounting and financial accounting, who sets the rules for accounting, it’s principles and so on.

Not repeating them again let me get into the nuances of creative accounting:

- The mother concept of financial accounting is a journal entry. For every plus there has to be a minus. The nature of posting has created more complications:

- with advent of ERP and other systems routine process like Sales, Procurement etc accounting entry is linked to business process. That means unless you create a PO and receive goods entry won’t be posted, with security features around direct manual entry is prohibited. But still I can create few similar accounts and post it directly bypassing all that PO/Goods receipt etc.

- Some processes are still not linked to accounting as a single platform, like software revenue (project management tool, expense booking, billing/revenue) still managed through different systems. This results to lots of interfaces and again possibility of direct posting.

- A bunch of journal entries are meant to be posted directly to the ledger like manual journals on adjustments, consolidation, provisions etc. There are suppose to be controls built around it but no guarantee though.

- Balance sheet reconciliation and review processes is an evolving area for lots of companies more in the space of smaller and mid companies. This means account balance is reconciled with source and reviewed at different layers to ensure correct balances are appearing in financials.

- Internal controls is an area by itself having a wider scope, things are improving but subjectivity and materiality drags down the assurance level. Same is the story with statutory auditor. For example for an auditor 50 Cr is a material amount for misstatement of financial reporting. Well I may not agree with it, but financial statement assertions (assurances) are build on auditor’s assertion not me and you.

- Second area is standardisation of accounting practices against business process.

- Accounting standards are globally debatable and have no uniform approach.

- Every business transaction is prone to multiple interpretation. One area of interpretation where management have the decision making power say like treating an expense as capital expenditure or not. This decision making comes either from the flexibility offered by standards as to what is capex and what is not which has open interpretations and of course the complexities of certain area like software revenue recognition (like fair value accounting).

Let’s discuss some areas which are prone to accounting harakiri and the places and tools where we can find them. Where there is a disclosure we can compare and estimate something. If no disclosure have been made only way left to reconcile, analyse different statements and information to sniff again best guess estimates!

First lets understand motive behind creative accounting practices, it’s two only. Either I overstate (inflate) earnings or understate(deflate) earnings. There is nothing else.

Rather than targeting bottom up lets do a top down. What are the scenarios when accounting can be manipulated or window dressed, do remember some of these may have been done with an intent to create a fraud as well. But as discussed earlier we need to investigate separately with management provided information, something not easy for retail shareholder.

- By applying inconsistent accounting standards due to the flexibility allowed.

- Reclassifying Profit & Loss to balance sheet or vice-a-versa (e.g. capex/opex decisions, patents charged off to PL directly).

- Reclassification within income or expenses account (one time sale shown as revenue from operations, actual expenses twisted as provision to improve above the line profit).

- Adjusting expenses with income or vice-a-versa (very common practice when multiple revenue practices are allowed. Say one company has project accounting and sale of services. Shift the expenses to project as its done basis percentage of completion which can be deferred!)

- Play around periodicity of expenses or income, assets or liabilities (shift a future expenses to current expenses like writing off R&D, amortise costs too slowly so that current expenses shifted to future).

- Use balance sheet to cover up (creating reserve and postpone profits to future) where it couldn’t be done under reclassification.

There are multiple ways to cross check and unearth. For a retail investor I could think of something which may be easy:

-

Auditor’s and management notes: this should be our first place to see if there is confession if any. If management has identified with impact our job becomes easy. A lot of times I started without ignoring obvious, after 2 days I realised it’s already disclosed by auditor/management.

-

Accounting Policies Comparison: Every company has to formulate it’s own accounting policies which is in line with the accounting standards issued by regulators. You can see them just after schedules in financials and first section of notes to accounts. Plot accounting policies for 5-6 years, it will open up if they have been applied correctly. If see inconsistency important to understand the impact of financials e.g. depreciation method changed from SLM to WDV.

-

Common size balance sheet and profit & loss account: this is done by listing key items of PL and BS over few years and then calculating a percentage to a common base. Say R& D expenses was around 2% of sales and suddenly went up to 20% one year. This becomes an alert.

-

Reconcile with cash flow: every balance sheet and profit & loss account have a relationship with cash. Unless we receive or pay cash it cant be shown in cash flow statement , subject to a big caveat the bank balance what appears is correct! (apparently for Satyam it wasn’t correct). So what we can do if accounts receivable has been rising faster than sales then sales are booked without cash being collected. Now this can be due to aggressive sales tactics by extending credit period to customers or over book billing as sales and then pass reversal entries next year. Every element of PL if paid /received as cash will have an impact on cash flow. You can reconcile same.

-

Compare quarterly results: quarterly results are abstracts of financials and given quickly from reporting date. Apart from good earning member there is no sufficient time to do all the good window dressing. Add three quarter results and compare with annual figure proportionately. You will see the amount of sales and expenses that gets booked in last quarter, March quarter needs to be best quarter :). But a caution, this may not work for balance sheet, a good amount of entries like employee benefit provisions, estimates are done on a yearly basis.

The above are generally ways of hunting down, few specific example so that we know what is happening “normally”, meaning the areas where creative accounting practices applied. By using the methods mentioned above you should able hunt them down for quite a few.

Few practical experiences, please do read “Financial Shenanigans”, you will get most of examples. I am including a few customised to my approach.

- Check price per unit if sales are going down. There is a chance of rebates and discounts applied at an account level when prices are constant and rising.

- If related party transactions are high with high margin business big chances of revenue big over stated. Even cash flow comparison wont catch as bank transactions between known people are not a big thing.

- When we have high intangibles and reserves. Non cash entries get posted for bogus transactions to strengthen book value. Intangible I am not referring to purchased or developed software but more goodwill, patent types (not acquired).

- Loans included in related party transactions vis-a-vis revenue movement. Reclassification from revenue to loan is common.

- Extremely lower rate of taxes without tax incentives.

Actually I want to go on and on. I think to do justice lets talk about forensic and creative practices separately in a thread. There can be simulation to millions of situations.

I do have a piece of analytics done for Maithan, don’t have courage to use in public forum and you know why. ![]()

If you feel to have a discussion on further on this subjects, please ask specific questions. There are many people to answer it.

Thanks!

- I will move to financial metrics to see the competitive advantage confirmation and simultaneously we can do an analysis of growth, health and profitability. They are linked to each other, this is the core part of financial analytics including key ratios etc.

3 Likes

Developing a Investment System

My new mentor Mr P seems to be more impressive than my initial assessment and I am not surprised. I am pretty sure now India has thousands of maverick investors not used as trump cards when it comes to education!

Part of my recent interactions and learning (which still continues by the way) we spoke about developing an investing system. It’s pretty much a flat concept which includes a combination of research, money management and behavioural finance. But the gold rush is in finer details, here they are:

He told me how do you know:

- To protect capital when market goes against you?

- When to take profits?

- How much to buy or sell when you decide to do so?

- Is there a single method that works for all stocks?

He rightly prompted people make money in market by unleashing their potential and getting aligned with market. Investment is about 83% behavioural finance, money management and 17% research (though this number can vary for a casual investor).

Today I just want to cover the questions one must ask (whether new or old investor) before even thinking about creating a investing method or system.

- How much capital do you have (one time and recurring)?

- How much money you need to survive every year?

- How much money or profits you are expecting from market?

- How much time you can devote to investing or trading?

- Are there too many distractions?

- What are your skills in business strategy, behavioural finance, mathematics, finance etc?

- What is your edge in investing?

- How much money you can afford to loose?

- Can you work yourself day after day?

- How will you know your system will or is working?

We spoke about conceptualising a system, infuse theory of probability for risk management to money management and much more. I will come back and update them.

Also will try to get back to study of financials soon.

4 Likes

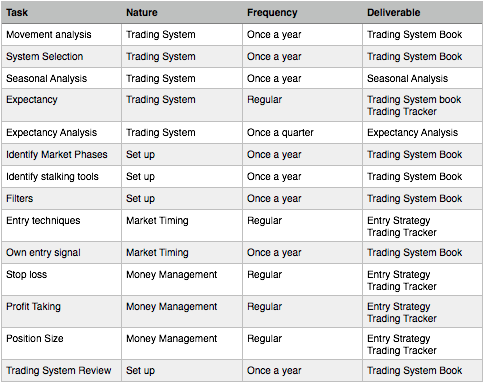

Building a investing/trading system

As the name suggests it targets speculation (you can call it technical analysis) with an attempt to break market data to theory of risk management and probability. The end game is to address uncertainty with more reliability. Some of the noting here you may apply to investing (long term) as well.

Before getting into specifics, this is a customised approach I have been working with my mentor and well wishers for a month or so. My mentor in turn is heavily influenced by Dr Van Tharp. But nothing sounded to rocket science after a hard work of one month or so. Yet I never implemented a bunch of them may be due to my predominant lenience towards traditional value investing.

Broadly we looked at following areas:

- We started with behavioural finance which include the holy grail, biases, and set customised objectives.

- Setting the seedbed for system namely key concepts that is required and criteria for selecting including theory of expectancy.

- Dissect key components of trading system including set ups, market timing, stop loss, profit taking, position size, opportunity cost.

I went through more than a dozen books in this period but one book which I would like to give 9 star 10 star even out of five is this:

This is my customised end result:

- Creating a trading system

- Drill down a stock universe

- Apply entry techniques and timing

- Trade management

- Continous improvement

Still I am building a complete plan, you can see a current abstract of it here:

But this is not important rather to understand key terminologies and concepts behind a system (I may not be anywhere close to a robust system with limited testing so far).

You would get detail in Dr Tharp’s book and lectures, let me write down the abstracts which were eye opener for me:

- People make money in the markets by finding themselves achieving their potential, and getting in tune with markets.

- For a successful trader psychology plays 60% role, position size 30% and system development 10%.

- Analyse winners and losers, intellectually estimate what made these movements, a first set of criteria what I have defined are:

- waves and pull backs

- nature of trend (sharp, gradual)

- Long or short consolidation

- Sputtering or non sputtering

- Volume/price relationship

- Level of speculation

- Level of participation and trade size

- Impact of management announcement (expansion etc)

- Fundamentals (accelerated earnings and low debt etc)

- Worst case scenario for every trade

- Expectancy- how is your position size, trading investing style, stop loss determines a higher return. I think this is the biggest take away which I was never so clear.

- Understanding of different phases of market phases and use them as set up.

- Developing your own entry signal.

- Different types of stop loss and profit taking strategies with respect to risk multiples.

- Decide the amount of investment based risk appetite.

Dr Tharp’s lecture and book pretty detailed and self explanatory. I am not going repeat them all, but it require 3-4 readings to create a plan and put into action.

I strongly recommend/request you go through, it may change the way you think at some of area like position size and expectancy forever.

Do let me know questions if any, I have clubbed the performers analysis to jewels of India. The moment I finish will post the results.

1 Like

Decide the LESSON you want to learn: applying behavioural finance

Few days of extreme volatility, experts are back with a long list of advices. They are all over television to telephone, news paper to New Delhi! Though I stopped reading news paper and watching television for sometime now, something caught me. While these financial wizards (at least they claim so) trying to sooth our nerves I was gathering few common factors pointed out by these gentlemen at the time when balm is required to relieve pain. Here they are:

Risk appetite management: invest according to capacity, diversify your asset class. It goes with rhetoric and irritating comment such as” don’t put ALL your eggs in basket” and this is called as age old wisdom. Does this work for everyone?

In first place what is relationship between risk appetite and diversification? Appetite means desire to eat food, sometimes due to hunger. Risk appetite is tolerance the level of risk an object (organisation or individual) is prepared to accept. I have 300 rupees to invest a. I pay 100 bucks to underworld b. Another 100 to black marketeer c. 100 bucks in gambling (race course/game) . What wonderful diversified assets are, well I am diversified boy.

If you are 20 plus something it’s assumed your risk appetite is higher and if you are 60 plus then you should read holy books and go for pilgrimage after keeping money in fixed deposits. Throw the 40 years of experience in stock market to trash bin!

how do I determine my risk appetite, I need to ask few psychological questions and decide the asset allocation. Now take a question do you have life insurance policy? No man I don’t have one; oh my god are you crazy? How can you survive without an insurance policy? So what I am Warren Buffett or Mukesh Ambani? Still life is risky, I need to insure. Similar concerns for mediclaim insurance without even knowing how many claims are getting rejected? Majority of insurance policies are not valid after 60-65 where you need the most.

you must buy a flat on EMI even if my economic profit is negative. So what, I buy a house at 23, buy the time I retire it requires 50% of cost as maintenance! So what even if the real estate doesn’t go anywhere in last ten years.

Biggest fallacies you can find within risk appetite simply because it’s a complex subject needs customised approach.

- If you know ONE asset class stick to your expertise which will reap benefits. Knowledge is built over the years, so if you are good at equities don’t waste it by diversifying, same goes for real estate. Losses from asset class can be managed through MONEY MANAGEMENT not diversification. Diversification adversely impact return on investment, what bigger joke it can be, to avoid uncertainty you jump into an area where you have no clues!

- Insurance may not be solution for all, if you are 40 year old and have 40 years of net worth days…all you should be concerned developing a plan which ensures your money move faster than inflation. Shut down the damn insurance policy!

- Don’t make house on EMI as emotional decision. Real estate is nothing but an asset class, if it doesn’t offer you adequate returns don’t mind to look for alternatives. For example upmarket properties in Bangalore has fallen into abysmal rental return of 1.5% or even less per annum! Can you imagine your payback period is 70 years?

-

Tax benefits: You know you get tax benefits on dividend, or even long term capital gain on shares (actually they are tax free now). Similarly you buy a house , you get tax breaks! Why so much insistence in saving taxes, well I don’t know what the govt is doing with my taxes? Valid question, by paying 70 bucks for a petrol (which includes hefty excise and sales tax) you even don’t know what the govt is doing with your money. If one earn simply pay off taxes, or get ready to fight govt in courts. There is no third solution, use tax benefits like usage of credit cards. If a tax benefit and sale of asset coincides then use it or else ignore!

-