Can someone help in quantifying the impact of concern raised

I guess that the impact would be mainly on numbers mentioned in “Product Related intangibles”

I understand that these exits will have considerable impact on topline / bottomline in coming future as well. Hope they are protecting / improving their margins with these exits. We have Q2 results call scheduled in next week & hopefully we will get answer to floating doubts

I agree that management have been talking rosy things coming out from these JVs in long term. But not much really translated into actual business on the ground. The Omnichem JV was going nowhere for at least last two years. All this started when suddenly they lost a big client who was main customer for the product from this site. The China JV was yielding some profits but if you listen to to last earnings call (or Q1 FY 2019-20) the MD had clearly stated that they were not expecting any business from the JV in this quarter because it was closed because of environmental clearance needed from authorities. No one knows how much time authorities would have taken to give clearance (if they would have at all).

I have two observations to make

IMHO if an asset is not churning out product and just depreciating then it is better to sell them off. Of course the sell should not be a distress one.

Granules had over expanded its business. A JV in IN, a subsidiary in US, a JV in CN, besides multiple facilities driving core business. Top it with expansion of facilities, and venture in Onco, and self labeled FD in US…a lot was going on. Taking off some of these which were not working to double down on the ones which are yielding results seem to be move.

I can understand based on management previous comments about exiting Omincom JV. The JV wasn’t going anywhere. Also, the terms of the deals were one-sided in my view (based on the QIP document). Granules have invested the plant, but there was no guarantee or commitment from the JV partner about taking out the supplies from them. As promoters, they must be feeling optimistic and hoping that it would turn one day, but unfortunately, the day did not arrive. So I think it was a reasonable decision to take a step back and move on.

The CRAM space looks attractive, but it is hard to crack, and I have read other players like (Shilpa medicate, I think) also exited the CRAM JV.

In the case of Bio cause, the decision is a bit surprising, as they had not given any hint in their earlier communication. May by there is sudden changes of circumstance which would have compelled them to take the decision.

Either way, I think it is a good decision, as it would allow the management to focus their energy back to core business. Or it may be (just a wild guess) that the management is seeing more opportunities in the ANDA space hence creating more space by exiting the JV which is not focused area going forward.

The fact that they are retaining the commitment of around 300 cr PAT for the current year is good and bad. Good in the sense the management was not expecting meaningful profit contribution from these subsidiaries and also a subsequent reduction in debt. I think the debt reduction should be significant around 170-200 cr(I am assuming) after exiting both the JV.

However, the management is publicly committing to deliver on 300 cr PAT. History tells us that once the management committed number publicly, they are likely to make up the number. I hope this is not the case for Granules, but only time will tell.

Agree. Coupled that with 15% tax on the new manufacturing capacities would be an exciting proposition.

I am sure they must be thinking of it expansion now as they have completed the most prominent expansion plan in their history. However, the current expansion plans have not started yielding results and, it probably will take next year before they see the increased result.

But I won’t be surprised if they announce a new capacity expansion in new 3/4 quarters. So far, Granules has thrived on capacity expansion. But if they see an increased return on their ANDA portfolio, things could be different, and they might become conservative in capacity expansion.

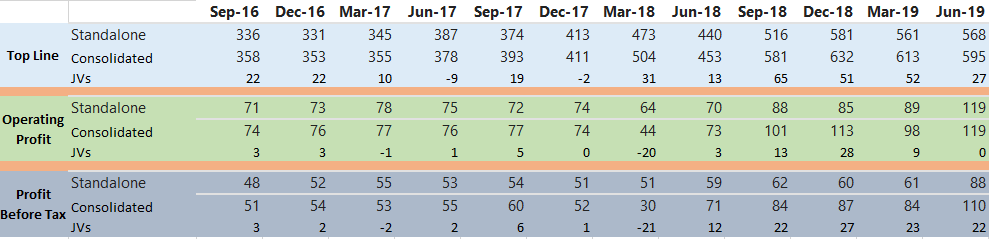

; As per their 2019 AR, their total borrowings amount to 930 cr, assuming a 10% interest rate ( similar to peers) their annual interest outflow should be around 90cr. However if you look at the income statement the finance expense is only 28cr for fy 19, what happened to the rest? They have been capitalized and the cash outflow will be under " cash flows from investing" in the cash flow statement. The difference 60 cr or so optically adds to PAT.

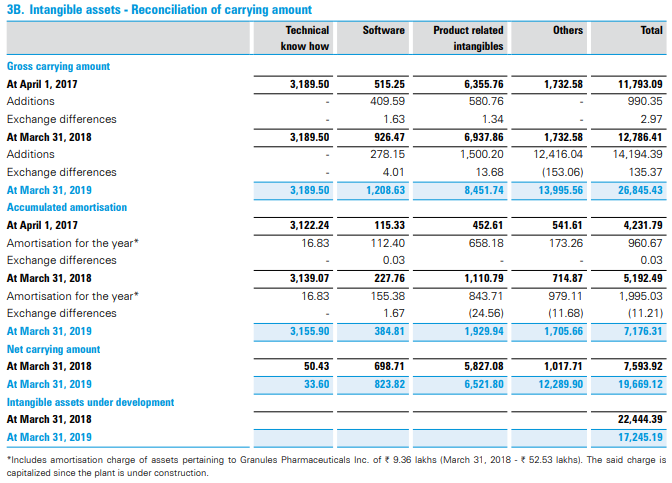

; The balance sheet shows a total of 368cr in " intangible assets" and " intangible assets under development", a very high number in relation to their 745cr PPE. These intangibles as explained by them in various calls are filing expenses and staff costs for numerous DMFs and ANDAs filed over the years. This should ideally have been expensed ( as they are starting to do now) as pharma is hit and miss, no guarantee that all of these filings will be successful. so far other than their core 5 molecules they have not announced any major successes. This cannot continue for long, either revenues need to increase from new molecules or write offs need to happen.

Many investors have been wondering why Granules doesn’t see much buying despite optically low valuations, what I mentioned above could be a core reason, this would be something professional investors would look at for sure but may escape retailers.

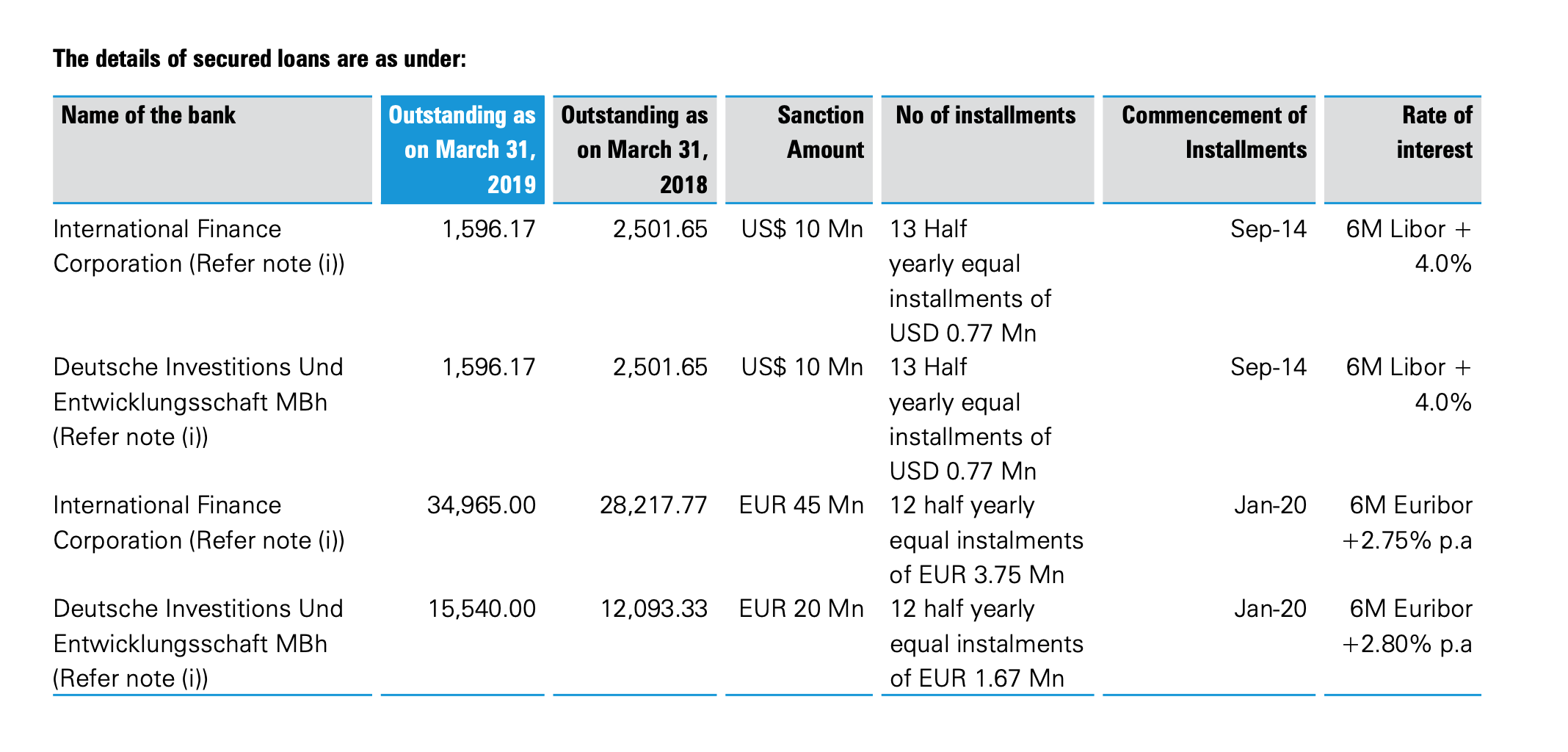

Do not assume 10% interest because they do not pay 10% interest - see their AR where they have mentioned about how they borrow - they borrow thro libor linked rates which are much lower

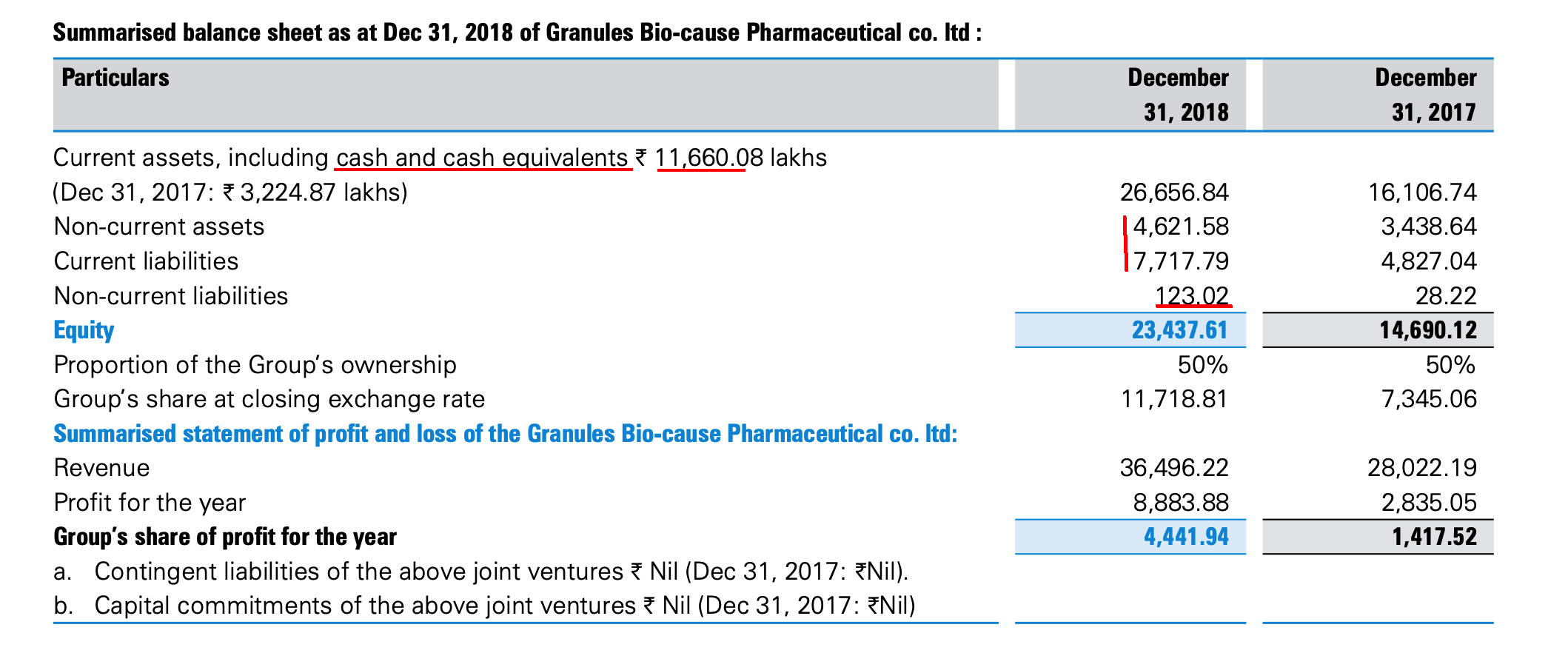

From the AR, the Bio-cause JV has cash and cash equivalent of 116cr and short and long term liabilities of around 80 cr. So looks like very cash rich business with no or minimal debt on the book. And the business has generated 88 cr PAT last year.

Even if I assume that the PAT was higher due to high prices of Ibuprofen API last year, the JV was very profitable for Granules. So Granules shall receive around 120-150 cr for this JV, which could help in further debt reduction.

Granules revenue growth in the past 10 years was at 22.95% CAGR. This was mostly from the basic 5 molecules. Now they filed ANDA and moving up the value chain. Why do you think that they won’t be able grow? Granules has been able to sell whatever they produced from additional capacity. So demand doesn’t look like an issue for them and they been consistently capturing the market share from their competitor’s.

Wait for the market’s to help in deciding if you celebrate with champagne or coconut!!!

Even I was looking formarket size & impact of this but couldn’t find recent info… Long back (approx a decade back) Fexofenadine drug market was approx 452 Million USD. The new development is that it is available OTC now. Other players e.g. Dr Reddy’s are already selling it in US markets and Granules being new player… would need efforts to get a pie of that.

This drug is a bioequivalent generic version of The Allegra-D 12 Hour brand, which had annual US sales of approximately $49.8 million recently.

I think it is Allegra and not Allegra D. D version is a combination with pseudoephedrine. Allegra is used for running nose, watery eyes, itchy eyes and sneezing. Not very large volumes drug.

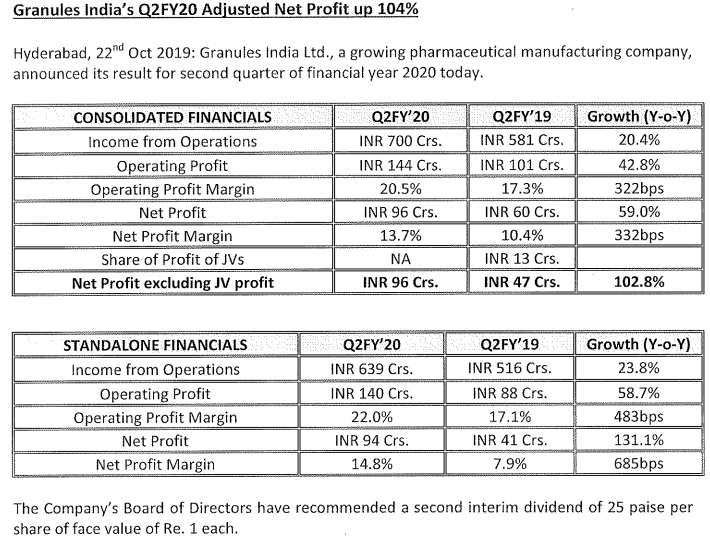

“l am happy to share with you that our growth momentum has continued in the second quarter and we reported an adjusted profit growth of 103% over the corresponding quarter of the previous year. This is the result of operational excellence and a vigilant watch over our margins via optimal product mix, capacity utilization and minimization of our expenses. Our unwavering focus on the regulated market at a contribution of 73% (North America and Europe) and a shift towards PFls and FDs at 69% of the total revenue has enabled us to achieve this growth during the quarter.

During the quarter, we have filed 2 ANDAs and received approval for 1 ANDA by the USFDA. We have also filed two dossiers in Europe and the UK to expand our global presence of our core molecules and to reduce our concentration risk. We are well on track to fulfil our commitment of higher return on investments and improve the leverage position of our Company. With improved cash flow our net debt position is now at a comfortable level of 1.6x of EBITDA.”said Mr. Krishna Prasad Chigurupati, Chairman & Managing Director of Granules India Limited.

Granules has classified approx 194 Cr as JVs assets (Granules OmniChem Private Limited and Granules-Biocause Pharmaceutical Co. Ltd) held for sale

Granules Omnichem Private Limited (Entered in 2012), Book value of investment as on 30 June 2019 was 50 Cr. It has been sold to JV partner for 109.85 Cr

Granules Biocause Pharmaceutical Co. Ltd (Entered in 2007), Book value of investment as on 30 June 2019 was 143.65 Cr. Realization value of sale of assets to JV partner is yet to be ascertained.