As per today’s announcement, sale price of JV is 109.85cr. Hope they will utilize this amount to reduce debt further. Expecting around 140cr reduction in debt.

Net Debt at end of Q1 FY20 was 865 Cr

(compared to 930 Cr at end of Q4 FY19).

The company has stated that any cash proceeds from divestments will be used to retire debt and this 109 Cr should be going for debt reduction as business is now yielding free cash flow as well.

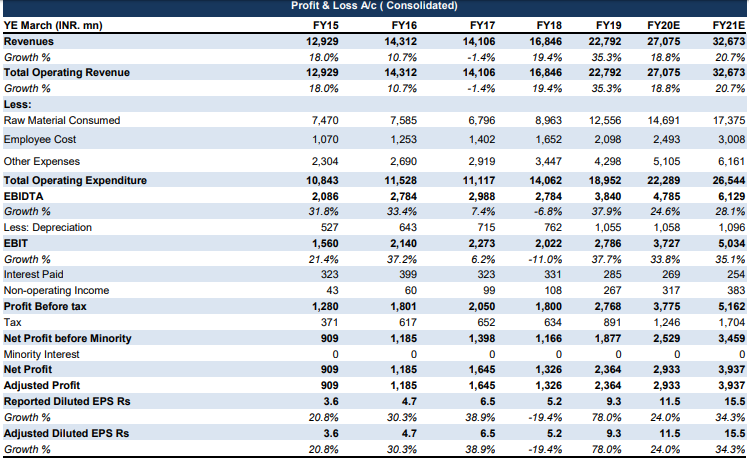

EBIDTA of 600 cr looks too ambitious to achive. Q1 FY20 EBITA was 119 cr approximately which has increased 21% compared to Q4 FY19. Management has guided for 25% profit growth (Last year EBIDTA was 384 CR). The revenue from sold JV won’t contribute this year.

Can you please share the details on how you have come up with EBIDTA figure of 600 Cr? Most of the brokerage report indicates EBIDTA in the range of 470 to 500 CR

I stand corrected, yes expected EBIDTA for FY20 is 500 Cr.

Got mixed up.

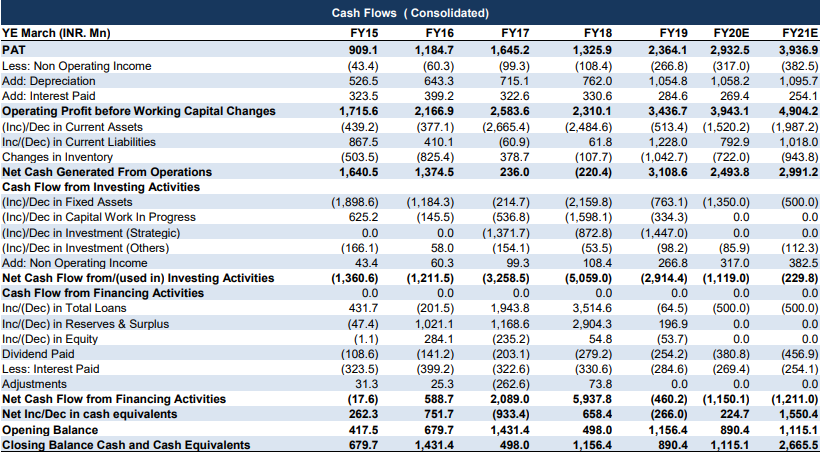

So FCF will be 90 Cr.

EBIDTA% at 20% is very much doable.

GPI is seeing a good scale-up in its formulations of Methacarbomol & Metformin ER.

Granules is guiding for GPI revenues of 250 - 300 Cr this year. Lets see where they endup.

Even if you take 500 crore EBITDA, my view is that you are mixing P&L no n cashflow no without factoring working capital to arrive at FCF. Why I am highlighting this is because it’s a heavy working capital business with high receivables . If one looks at EBITDA/CFO ratio of last 3 years, it’s just 35% . So , on a 500 crore EBITDA , the actual CFO comes only 170 crore . Now if you are considering capitalised R&D then it should get captured in CapEx (m not very sure but assuming this is how it happens ) n if it is in P&L it’s already captured at EBITDA level , so, we need to find overall balance sheet CapEx n reduce it from 170 crore unless one is very very sure future ENITDA to CFO is going to be much higher than 35%

Saurabh- the numbers quoted by you for CFO/EBITDA are not matching with the numbers listed by mrai74. Are you looking at only Standalone numbers? Please clarify.

I agree with the business being heavy on working capital. This was more evident in the past 2-3 years when company was going through CAPEX. When newly expanded facilities turned up they were not immediately ready to ship to the marquee clients in US (and other developed countries) because they needed to be approved by FDA and other authorities. Instead of not selling at all Granules decided to sell the products from thesefa expanded lines in other markets and possibly at more lenient terms. This might have been the root reason behind high receivables. If true then it would be at least partly addressed with now the expanded facilities getting FDA approval. I could be wrong, but I interpreted some of this from the last 2-3 earnings call.

Keeping the number crunching aside for a moment, the big picture for me is the move of company from API to FD. I also want to re-iterate there are many triggers in place for Granules- 1) New FDA approved facilities 2) New self branded drug launches in US 3) Onco APIs facilities coming up in near future 4) Good ANDA pipeline 5) Reduction in debt (and indeed it getting reflected qoq) and 6) Commitment from management to bring pledge to zero (and indeed it getting reflected qoq).

The key risk is if company would be able to create value for its brand in US and sustain it, the actual reduction of debt and pledge, high crude prices and maintaining margin in highly competitive environment.

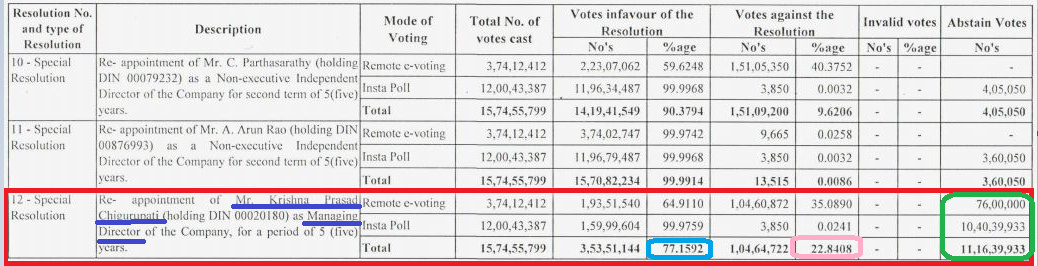

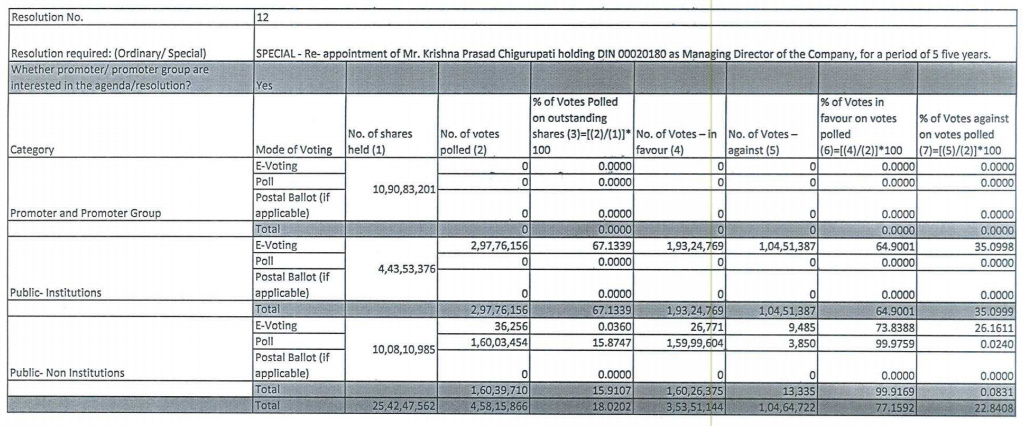

An interesting voting pattern in recent AGM of Granules, where promoter / promoter group didn’t vote (may be Mr KP can’t / didn’t want to vote for himself… not sure about legality… if promoter is barred from voting for himself) for resolution to allow re-appointment of Mr KP as Managing director.

This becomes critical as 35% public institutions voted against Mr KP’s re-appointment.

Is it something personal or Granules shareholders don’t like KP for his professional acts?

Although its good till he gets himself elected by getting anything above 50% but image gets dented with such instances.

Won’t it come under manufacturing company under 17% tax. But I see effective tax paid is lower. its 30% recently considering research expenses and investment expenditure exemptions

17% is only for companies which are starting new in India. For existing full tax paying companies it’s 25%.

I think i jump the gun on taxes here.

Before in the thread, I read that Granules was paying tax at full rate but getting some R&D benefits;

But looks like effective rate is around 27% only, so they will get benefit from new structure but may be not 10% but may be 2-3%.

For me Granules is the story which does not have demand side problem but more a financial side problems of high debt, high pledge etc. And those seems to be getting solved with every Govt + RBI action.

a rough calculation shows that Granules will save ~28 Cr in current FY due to tax reduction. If they can monetize 109 Cr from their JV sale and utilize these in debt reduction. The cascading effect of this on interest outgo & debt reduction shows promising outcome in next 4-8 quarters.

Although promoters have attempted well on pledge reduction but seems Mr KP has gone a bit slow on this front. Promoter Pledge remains at 36.99% (They committed to bring it down to 32% by Q1 end, in May’19). He used to walk the talk but he is set to miss his targets set for Q1… even Q2 is almost over.

Few of these had invested earlier and seems they moved out. Looks like management is attempting again & it could lead to next cycle of expansion plan. Its pure guess based on earlier concalls & we have to wait for outcome of these meetings for more concrete actions / decisions.

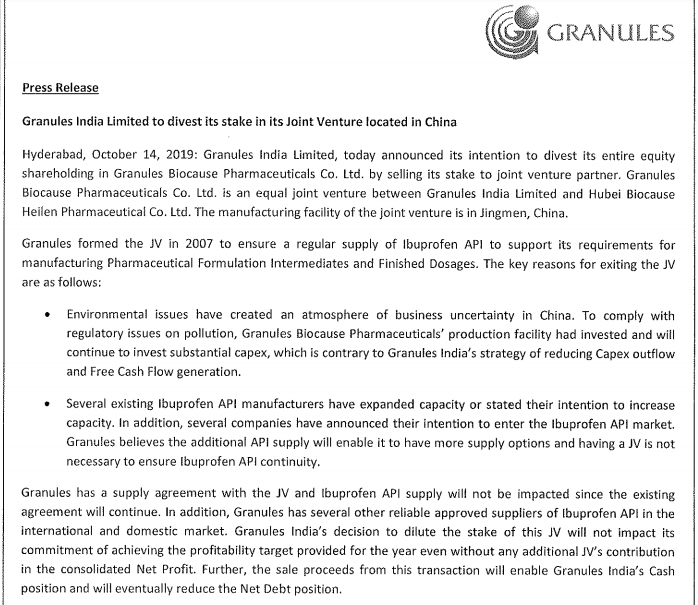

The Board of Directors at their meeting has approved to divest the entire stake of the Company in Granules-Biocause Pharmaceutical Co. Limited, an overseas Joint Venture Company situated in China. Conclusion of this transaction is subject to fulfillment of certain closing conditions as well as applicable regulatory approvals.

Environmental issues have created an atmosphere of business uncertainty in China To comply with regulatory issues on pollution, Granules Biocause Pharmaceuticals‘ production facility had invested and will continue to invest substantial capex, which is contrary to Granules India’s strategy of reducing Capex outflow and Free Cash Flow generation

Financial impact based on latest Annual Report

Granules-Biocause Pharmaceutical Co. Limited

The Share Capital of the Company as on March 31, 2019 is 3638.06 lakhs. The Company achieved a turnover of 36,496.22 lakhs during the year under review as against turnover of 28022.19 lakhs in the previous year. Profit after tax for the year under review is 8883.88 lakhs as against 2835.05 lakhs during the previous year of which Granules India Limited reports 50% share in profit from Joint Ventures/Associates.

Recent sudden JV exits are not positive for the business. Management had given no such hints in the last con call, in fact they were talking positively about the long term potential of these JVs.

Investors need to remember the significant intangible assets in the balance sheet, all these by right should have been expensed.

Any sudden write off of these assets will come as a nasty surprise.