Where it this number mentioned? I could not find it in announcement.

It’s in the balance sheet assets side as assets held for sale as 193 crores.

Per what I understand, that would be the investment cost lying the balance sheet and not the expected sale consideration. Is it mentioned anywhere that 194cr is the sale consideration?

1 Like

Notes from the Q2-Con Call.

- Expecting 4 to 5 ANDA approval in the coming two quarters. On target to add 4/5 ANDA in the current year taking the number ANDA filed in the rage of 10-12.

- Exiting the JV to generate FCF. It looks like Because was demanding a lot in term of CAPEX, hence the decision. Not expecting an excellent price for their part.

- Biocause- The price is not yet decided, and they are working on it. Hopefully, they will know more about it Q3.

- Want to exit and receive cash from both the JV by Q4.

- The money received from the JV will be kept in cash/FD. They are not expecting debt repayment. Instead, they focus on earning treasury income by depositing the cash in FD. This is a bit puzzling to me. Granules cost of funds at least 5%, and in the short term deposit, they are not likely to earn more than 6-6.5% per annum. Plus the interest earned will incur tax, effectively the net earring from the treasury will be 5- 5.5% per annum. For such a tiny (0.5 per cent) they are working on something which is not their core operation. Or maybe they do not want to share the use of funds at this moment, which looks plausible to me. They might have some other use in their mind, but they would prefer to have cash in hand instead of going to the bank for additional money.

- Pledge share- 37%. In the process of reducing it further and the pledge shall come down in the next few days.

- Raw material prices are stable.

- Gross margin of 48% is sustainable in the long run.

- Oncology block. Expecting some revenue next year and major contribution to come from FY22. This to me a looks like a long shot as Granules has no experience in Oncology so far as it is not their core molecule as such. Also, Oncology blocks are a bit difficult to get operational, so it will be interesting to see how this progresses.

- Current year and next year not planning major CAPEX. However, they cannot grow without CAPEX. If they see demand or shortage of capacity in the next 18 months, they start looking for CAPEX. Based on their current capacities, they have sufficient headway but looks like they shall resume CAPEX in FY22.

- Every $1 increase in revenue shall result in $0.40 improvements in bottom-line.

- Very confident of 300 cr PAT for the current year.

5 Likes

After the recent shareholder patter, today’s call and 3-year guidance, the stock clearly deserves a far higher price.

God knows if the market will actually reflect a fair valuation. For some reason the stock is always depressed.

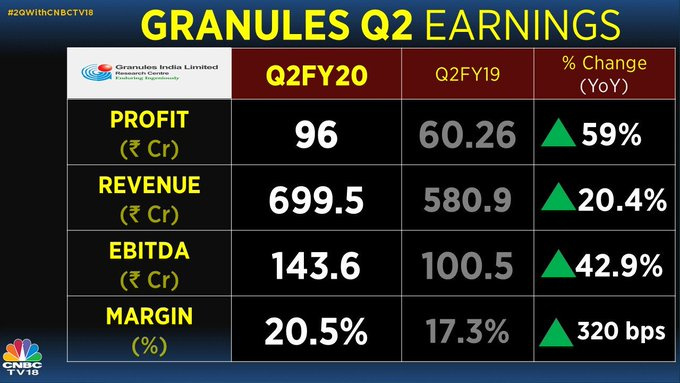

Q2 Concall notes

Q2 FCF : 35 cr

Net debt reduced from Q1-928 Cr to Q2-826.5 Cr

More improvement expected in net debt to ebitda ratio with improving ebitda

Omnichem JV exit process will close by Q4

Biocause jv exit - valuation discussion about to start - plan to close by Q4 - tough to get better value as china is going through stricter environmental regulations & frequent shutdowns are expected at plant

Biocause(JV) contribution to PAT of last year - 44cr / last year shutdown required money for environment clearance … again plant was shutdown due to new environment regulations… we can’t run business with uncertainty -

Biocause - granules still has a supply arrangement despite JV exit / Procurement prices will be lowest

Tax outflow of JV divestment - 18 cr investment in 2007 in biocause - long term capital gain (15%) will impact actual realization

Cash utilization of JV exit - will put money in FD & improve treasury, no capex plan as of now

JVs will not contribute anything to PAT/bottomline/topline in future because assets are shown as assets for sale - Although full exit will be possible by end of current FY - Closed from that perspective as per auditors accounting regulation / suggestion

Pledge - down to 37% - more reduction will come in next few months

Inventory days reduced by 4-5 days & trying to improve further

Margins of 48% is sustainable (fluctuation is due to sale in India / us)

Litigation settlement realization of approx 4.2 cr during Q2

Every rupee increase in topline will contribute to 35-40% of bottomline

Net margin from GPI-US has not increased due to hiring more resources / Q3 onwards will get full benefit of expanded facilities

Q1 had JV income included / Q2 doesn’t have / current FY PAT will cross 300 Cr

25% growth in PAT is easily achievable - management will try to do better

Oncology - discussion for contract manufacturing in process - next FY will start contributing / ramp-up of new setups in India - will become functional by next FY & fully contribute in 2022

Granules-US has 35% of us market of ibuprofen

Guidance of 25% CAGR for next 3 years

22 ANDAs under approval - 80% of GPI products (current & pending approval) have 3-4 competitors only

Enough capacity left underutilized… wish to utilize it first & plan capex once we see that we may utilize 100% facility in next 18 months - during next year we may revisit plans for capex as we foresee that we can stretch by FY 22 without capex

comfortable with 1.5x debt to ebitda… wish to bring it around 1… & that could be next trigger for further capex

Core portfolio of 8 products (added 3 more products in core molecule portfolio) contributed 83% to sales… and it was almost 100% 4-5 years back

API contribution percentage will come down by 5-10% in next few years

4-5 ANDA approvals expected in next 2 quarters

4-6 ANDA will be filled in next 2 quarters

Extra working capital needed for US as there is change from re-seller to direct sales to distributors

Note : Please consume at your risk as I might have overheard or incorrectly interpreted few facts. Few notes may be duplicate as shared by @paragbharambe. Certain details can be verified from attached investor presentation / transcript. Incase of duplication / ambiguity, details in presentation/transcript override above details

Q2_invetor_presentation.pdf (1.4 MB)

Granules India-Q2FY20 Earnings call Transcript.pdf (213.2 KB)

7 Likes

Nice summary @mrai74

I believe Granules can be Dark Horse among all API players and may get Rerating soon.

Promoter walking the talk on reducing pledge & Debts.

Growth Visibility is very much clear.

Major Capex done, may yield better for Q3 onwards.

Expecting over 50% returns in a Year’s time

1 Like

I have observed that when the stock price reaches 52 weeks high, a churn in investor happens.

An existing shareholder who have been holding stocks for some time, find the new high price tempting and sell out their investment. After all, they have seen the share price much lower and believes that the share price reflect the fundamental of the company.

At the same time, stock reaching new high - 52 weeks or lifetime high- attracts a new set of investors. Along with momentum(I am not an expert on this filed though), they believe that something is happening well in the company which is causing the share prices to reach a new high.

As a result of the struggle between buyers and seller, if the company continues to do well, it reaches new higher as the higher prices attracts more investor. Some time, their investment amount is also higher (if they are institutional).

I reckon something similar shall playout for Granules India. However, when it plays out it a million-dollar question, but I (and many on this forum) are hoping that it plays sooner rather than later.

Higher prices will also help the promoter sell some share in the market (they did in the past) to reduce their pledge holding, boosting the sentiments towards the stock.

Note- Holding the stock so view are biased.

4 Likes

You are right but here the situation is a little different. Granules messed up in the last three years as they became over ambitious and bit more than they could digest. Fortunately they seem to have realised their mistake and are deleveraging and gravitating towards their core strengths. They should progressively reap the benefits of metformin and other capacity expansion over the next two years. Provided they do not get diverted once again.

1 Like

I am not sure if I can say that Granules has messed up. Granules has started capacity expansion 2-3 years back, and if I go through their earlier con call and QIP document, they were clear about capacity expansion. Moreover, they completed the expansions on time and on the budget. However- as with any other capacity expansion- the approval from the US FDA was delayed, which was not in their hand. They were expecting the approval sometimes in the second half of FY19, but they received it in Q2-FY20. They did what they can from their side, and I cannot fault with them.

Metformin capacity was approved last quarters, and it was the first quarter where they reaped the real benefit of back integration.

Oncology block has recently started validation, but it will a while before they can reap the rewards for it IMO. I think the second half of FY21 when they may get approval from USFDA for it. Oncology, in my view, is a big risk/gamble for them as Oncology is not their core competency so far. After going through reports from different oncology focus companies, I concluded that oncology is a bit difficult nut to crack, so I think Granules will take some time to reap the rewards. The approval may even go into FY22 if it goes in metformin way USFDA approval is delayed, but that is sheer speculations from my part.

One thing I am by concern is optimistic management comments. As an entrepreneur and owner of the business, I am sure they are very optimistic, and some time gives optimistic expectations such as sometimes indicating in 2017 that 2019 was a game-changing year for Granules. Looking back, they were not wrong, except the game-changing year was 2020 and not 2019.

The big difference in new Granules (current version) as compared to the old one is ANDA/FD focus and migration toward high-value addition products.

In the past, they did not have ANDA and focus solely on manufacturing. However, with more than 34 filed ANDA so far, they are well placed to generate decent profit from them. Moreover, only a third of their ANDA is approved, so there is a huge scope for profit improvements. Agreed, not all of their filed ANDA may be approved, but even 70-80% approval rate will give improve their profitability considerably.

To summarise, the worst is behind them IMO, and they are on the verge of reaping the benefit of operating efficiency by utilising existing fixed assets more efficiently. Sales from FD by newly approved ANDA will be the icing on the cake.

I won’t be surprised if more research bourse comes up with a buy report on the stock as it reaches a new high.

Notes- Invested and views are biased.

2 Likes

@mrai74 - Looks like the report is behind the firewall (which need subscription). Do you mind listing key points from the article (if they are not mentioned in the above discussion)?

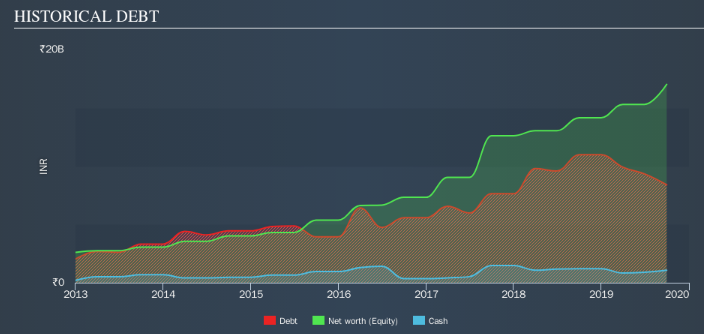

Granules India had ₹8.40b of debt in September 2019, down from ₹11.0b, one year before. However, it also had ₹1.07b in cash, and so its net debt is ₹7.33b.

The latest balance sheet data shows that Granules India had liabilities of ₹9.60b due within a year, and liabilities of ₹5.11b falling due after that. On the other hand, it had cash of ₹1.07b and ₹7.83b worth of receivables due within a year. So its liabilities total ₹5.81b more than the combination of its cash and short-term receivables.

Of course, Granules India has a market capitalization of ₹31.4b, so these liabilities are probably manageable. However, it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company’s debt relative to its earnings, its net debt is divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we get both the absolute quantum of the debt, as well as the interest rates paid on it.

Granules India’s net debt to EBITDA ratio of about 1.5 suggests only moderate use of debt and its commanding EBIT of 23.9 times its interest expense, implies the debt load is as light as a peacock feather. In addition to that Granules India has boosted its EBIT by 73%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Granules India’s ability to maintain a healthy balance sheet going forward.

A company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Granules India saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Based on above Granules India is not finding it easy conversion of EBIT to free cash flow, but the other factors considered give us cause to be optimistic. In particular, we are dazzled with its interest cover. Considering this range of data points, Granules India is in a good position to manage its debt levels. But a word of caution: debt levels are high enough to justify ongoing monitoring.

4 Likes

Thanks @mrai74 for laying out argument for debt and cash flow, and I could not have agreed more.

Granules has been reducing debt by 30-40 cr each quarters, which is a good thing. However, I am puzzled by management’s comments to use the proceed from JV divestment for treasury gain.

Their cost of funds is upwards of 5% and how much more treasure income they could get? Any idea?

1 Like

The elaborate analysis does make one dive deeper…my comments:

-

The current assets also include 1.13 Bn other current assets which haven’t been considered in the analysis. These are convertible in cash as well.

-

The long term debt was taken on as we know for capex. During the previous years, the company was high on capex cycle. Since the assets’s monetization had not kicked off, negative FCFE was obvious. Besides, thereafter the company was hit by input costs escalations and lag in passing the costs to customers. Historical FCF trends may not be the right indicator for the future. FY19 and H1 FY20 saw positive OCFs. The management is conscious about capital allocation and cash flows.

-

The analysis talks about liabilities outstripping assets (convertible into cash) and the back up from market cap…the debts were taken on for capex in anticipation of higher future revenue. Matching of all liabilities against assets-convertible-into-cash is relevant only during liquidation of a company; at this stage, the non-current liabilities are to be paid by asset monetization (and maybe JV sales proceeds).

-

My understanding is that the cost of debt appears optically low due to capitalization of interest costs related to capex. The management had however indicated that their foreign debt carries low interest rate and it is beneficial to not repay those debts now, rather pay thru asset monetization.

-

At this point, the stock deserves a substantial re-rating due to improving/ positive FCF, pledge being brought down, topline and EPS growth, consistent dividend payout, improving balance sheet/ ROE and very cheap current valuations.

-

Regarding the sales proceeds, if I remember correctly, the management indicated that until a clear plan is chalked out, the money will be kept in bank deposits.

Granules has been a case of a good company but a bad stock due to its history of a debt-laden balance sheet and no profit growth. However if the the recent past is any guide, the stock deserves more. This is my personal opinion; the recent price moves seem to however indicate otherwise.

6 Likes

Very good analysis. I have not understood a few of past management actions :

- Why did the management issue warrants to themselves and then convert them by taking personal loans against share pledge. What was the objective ?

- Why every concall spends approx 80% of time on trivial issues.

- What was the need to push the company into a rather precarious negative cash flow situation ? If the market had turned negative or FDA inspection gone haywire at that point of time ?? Apparently the company needs to evaluate risks better, before making investments.

Research report from Axis Capital

Granules - Initiating Coverage - Axis Direct - 07112019_08-11-2019_08.pdf (2.2 MB)

He’s just calculating based on 10 PE! so there’s lot of scope for good upside assuming PE re-rating as pledging and debt comes down

1 Like

1 Like

New plant operational from this qtr, results set to improve.

Debt & Pledge also coming down gradually.

Rerating candidate

1 Like

Can you share more details on this?

As per recent concall, Granules shared following

1 Like