The story of Granules India is in transformational stage, no doubt, but the real benefit (if at all) would start to flow in only after 2 years (i.e. from FY 19 onwards).Going by Management commentary it is clear now that they would be in high investment mode in coming 2 years (including current one). So, instead of analysing it on quarterly basis , it has to be analysed with minimum 3 years time frame. If at all an investment hypothesis is to be developed in Granules India, it has to be made by keeping FY 20 in mind. Any investment hypothesis with shorter time frame may not work here.

So, I am considering a base case of Rs. 3000 cr estimated Revenue in FY 20, with a profit margin of around 14-15%. At 15%, it would give an estimated profit of around Rs.450 cr. Now, any one can derive estimated Market Cap by applying whatever P/E he expects ( I would not like to speculate on P/E at this point of time).

So, as an Investor I am constantly trying to challenge my own investment hypothesis and try to answer the following questions?

(a) Can they achieve Rs. 3000 cr sales by FY 20

As regards as Revenue is concerned, I think going by their track record , they should be able to comfortably achieve 20% CAGR in 4 Years (majority of growth expected back loaded) . Following points should support this assumption:

• Aggressive capacity expansion plan for base line (core) products i.e. Metformin ( by 7000 ton)

Paracteamol (by 5000 ton) Guaifenesin ,(by 2000 tons) and so for other products also .

• Filing of ANDAs (including from Auctus)is expected to gather momentum ,

• Incremental Sales from OTC segment (to retail giants)

• Scale up of Omnichem JV (CRAMS)

• Revenue from at least 1 product from 4 products in licensed from USpharma – Windlas

(b) Can they command 14- 15% net margin by FY 20?

The story of Granules so far has been that of expanding EBITDA margin (from around 12% in FY 11 to 19% in FY 16) primarily due to operating leverage and rising contribution in sales from high margin Finished Dosage business (from 0% in FY 08 to 34% in FY 16) and the same trend is expected to continue in future also. Margin in OTC segment, CRAMS and marketing of in licensed product is expected to be higher.

I am not considering the upside if any of the 4 Products comes up with limited exclusivity.

Key Risks / Concerns:

(a) Any negative news on FDA front(or any other regulatory authority in other countries): Probability: Low (due to B2B Nature, past track record) Impact : Higher (>60% business in regulated markets)

(b) Pricing pressure due to declining raw material prices (as witnessed in recent quarters). This is a high probable event due to absence of niche products presently.

© Very High Compensation to Promoter Group plus increase in their salary surpassing their business growth. I am still breaking my head as to how to treat this. Would request Seniors to help me on this.

(d) Other interest of promoters, I think it is ignorable so far business delivers

(e) Impact of currency fluctuations. (will require more work )

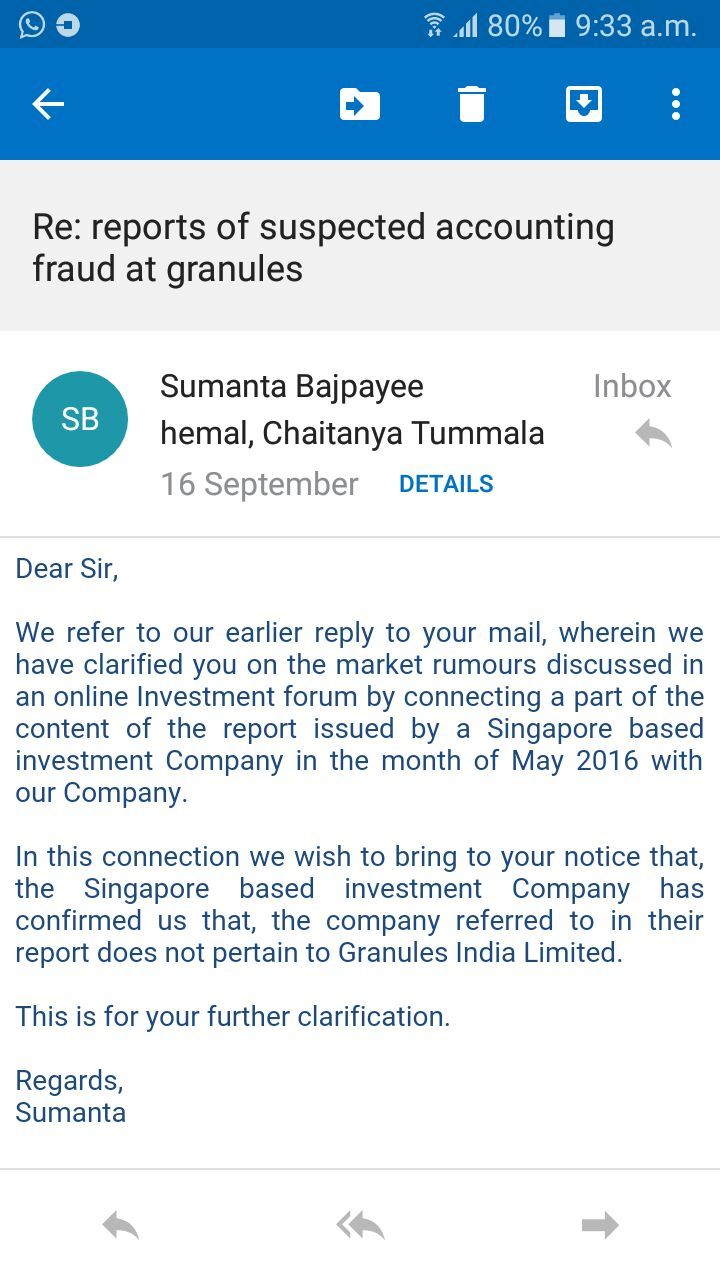

(f) Constant rumour on corporate governance issues.

(g) If they resort to further acquisitive growth , it will come up with its own challenges (including integration, goodwill issues)

(h) Debt levels although in comfort zone now, has to be key monitorable

Disclaimer: Invested >10% of PF and constantly reviewing the assumptions