Granules India to file 2 ANDAs in US, 4 here this year

Expects easily 200Cr PAT for FY18.

Granules India to file 2 ANDAs in US, 4 here this year

Expects easily 200Cr PAT for FY18.

I think 10-15% top line growth guidance was for FY 17 .I don’t remember exactly but it should be for consolidated numbers.However, I don’t read too much into this guidance of top line because I don’t have much expectation in sales growth for at least 2 years.

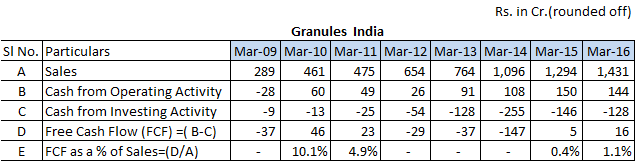

Of late, I have been trying to think over the various factors that may put our investing thesis in Granules for a toss. Obviously, the first factor that comes into my mind is the consistent lack of free cash flows in the business as is evident from the following:

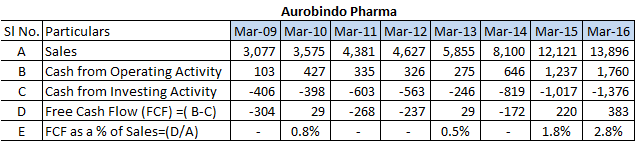

So what I did recently was to try to find out the Free Cash Flows of comparable (not necessarily similar) businesses which are of higher size in terms of Sales, Profit and obviously have already achieved higher Market Cap. So, in that direction I figured out the Free Cash Flow from FY 2009 to FY 16 of Aurobindo Pharma as reproduced in the table below:

(Data Source: Screener.in)

From the table given above, it is clear that even Aurobindo did not generate any significant free cash flow all these years and that has not stopped its Market Cap rising to around Rs. 47,000 cr over the said period.

Obviously the above re rating has also to do with so many factors, my point is that if Management of Granules is able to execute their plan well, the lack of free cash flow may not be a limiting factor to the re rating of the stock, but obviously it has to start generating free cash flow at some point of time.

So, in my view the call that is to be taken in the Granules Story remains the Management Integrity (Governance/Ethics whatever one calls) and of course their Execution ability.

Now someone may argue that why I picked Aurobindo only and not others, the answer is that I find it more suitable to compare Granules with Aurobindo since Aurobindo has also undergone a transformation from being a predominantly API supplier to a leading formulation player during all these years .

I also invite the views of seniors on the subject

Thanks

Granules Q2 Presentation

http://granulesindia.com/documents/investor-presentation/Q2FY17.pdf

Q2 Concall Transcript

http://granulesindia.com/documents/Earnings-Call-Transcript/GranulesIndia25Oct2016.pdf

excellent comparison.similar to cash flow a comparison of margin expansion and progressive market cap movement for the same time period makes the comparison very appropriate.

Centrum Research report on Granules post quarterly results & concall

http://www.moneycontrol.com/news/recommendations/buy-granules-india-targetrs-190-centrum_7886081.html

The PAT for FY17 looks optmistic at 202 Cr. Granules in H1 FY17 reported a PAT of 80Cr. Mgmt has reiterated 10-15% growth in revenues for FY17 during the Q2 Concall. If I consider lower end of 10% ( as Q1 and Q2 had a muted revenue growth), it would mean a topline of 1574 Cr for FY17. H1 FY17 revenue has been at 712Cr which would mean 862Cr for H2FY17. EBIDTA margin has been steady around 20% for last few quarters. Assuming 11.2% NPM ( same as Q2) Granules would report a PAT 96Cr during H2 FY17, taking the total PAT for FY17 at 176Cr.

Below is the another one from KRChoksey. They expect PAT of 162 Cr for FY17.

http://www.moneycontrol.com/mccode/news/article/article_pdf.php?autono=7835021&num=0

All said, a PAT growth of 30%+ looks easy for Granules for next 3-4 years. At CMP, trading at 16x FY17E nos., looks very attractive.

Disc: Invested and views may be biased.

Thanks for your effort on comparison! I think it may not be right to compare at different time horizons. Please check biz composition at 1500cr sales for Granules and Auro. I checked screener and Aurobindo achieved sustainable 20% EBITDA margin at sales of 3k cr + while Granules is doing at 1500cr. Superficial comparison suggests absolute investment seems to be much higher than Granules. Granules seems to be ahead of Auro purely on manufacturing excellence largely due to scale in few molecules. It remains to be seen if they could build and replicate IP intensive segments like Auro. This will be critical for rerating

Pat 200 crore is for fy-18 not fy-17 check ?

The whole idea behind the above exercise was not to compare the two as such, but to find out whether lack of free cash flow in the capex phase can be a key bottleneck in the re rating of the stock. I believe every stock has a story of its own and no one factor can singly influence its valuation !

I avoided direct comparison between margin expansion and market cap movement because I believe Market Cap/ Price of a stock at a given point of time is a function of so many things including prevailing market sentiment / perception etc. Hence , I think such comparison may not lead us to right conclusion.!

Although there will not be any answers but the sheer lack of upward movement in Granules share price despite the market moving sharply in the last 7 months is baffling. To be fair, from performance perspective, the Co. has not done very badly - margin and PAT has been steadily moving up . Revenue has been muted due to reasons well documented.The only consolation is for last several years it had moved up so may be taking a long breather before performance moves it up again.

disclosure: invested 17% of my portfolio

Patience, Sir. Markets can ignore even the better earnings for years. Berkshire Hathway did not move from highs of 1998 till five years. Stock price of HDFC Bank remains stagnant for 5-6 quarters despite assured and predictable growth in Revenue/Profits and growing market share.

When I bought Eicher Motors in April 2012, for 6 months I was in negative but kept on buying more. It is 12 bagger now.

Please do not be envious of the victory songs on twitter, whatsapp and forums. How many of these have seen 2009? or 2011 or fully invested and then Aug 2013? Have conviction in your theory, please.

What I have learnt is that it is enough to just track the growth in the financials of your stocks and not bother about price. Granules may be yielding lower than expectations but is consistently improving efficiencies and has not given a negative quarter so far. Management is committed. Opportunity is still there.

Patience & Persistence.

Also, Prayer, for to enjoy all gains, we need His blessings ( aka Templeton).

Tata pharma fund has introduces granules in its oct portfolio. 2.8%

Granules filed for 3 DMFs during Q2Fy17

Dimethyl Fumarate (branded name Tecfidera)- Treats multiple sclerosis. Tecfidera had quarterly sales of USD 946mn as per below link

http://www.wsj.com/articles/biogen-profit-climbs-helped-by-stronger-sales-of-tecfidera-1461240080

Pirfenidone for the treatment of idiopathic pulmonary fibrosis (IPF). Brand name- Esbriet, Innovator Roche, CY15 sales were CHF 563mn. Drug was approved in 2014

http://www.roche.com/dam/jcr:5931e6ad-22f1-4e5e-858a-3748f6e425c8/en/med-cor-2016-01-28-e.pdf

Fexofenadone hydrochloride- Fexofenadine (trade names Allegra, Fexidine, Telfast, Fastofen, Tilfur, Vifas, Telfexo, Allerfexo, Flexofen) is an antihistamine pharmaceutical drug used in the treatment of allergy symptoms, such as hay fever, nasal congestion, and urticari. Fexofenadine has been manufactured in generic form since 2011

Another submission was done in Feb 2016.

CETIRIZINE HYDROCHLORIDE, USP - Cetirizine is an antihistamine that reduces the natural chemical histamine in the body. Histamine can produce symptoms of sneezing, itching, watery eyes, and runny nose

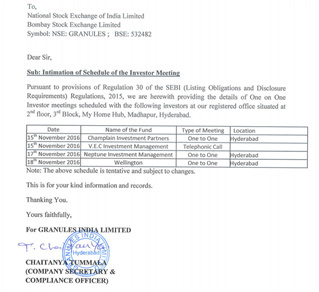

Schedule of investor meeting

Granules OmniChem facility completed U.S. FDA inspection with 7 observations.

Good development that it got inspected though it will take sometime to clear it completely. Should not be a challenge given their record in handling regulatory issues.

Disc: Invested

GRANULES: The Exchange had sought clarification from Granules India Limited with respect to announcement dated 04-Jan-2017, regarding appointment of Dr. V.V.N.K.V. Prasada Raju as an Additional Director and designated as Executive Director on the Board of the Company. On basis of above the Company is required to clarify following: 1. Disclosure of relationships between directors (in case of appointment of a director). The response of the Company is below.

http://www.moneycontrol.com/stocks/reports/granules-india-limited-5725961.html