Also other relevant number is depreciation which is 52.7 Cr in 2014-2015

Sorry no idea on this. I just highlighted Granules, could not identify the others

Thanks for posting this. Their reports are pretty good . So Granules investors need to take notice and investigate more.

Disc: Not invested. Tracking .

@darshit ,

I doubt there are many API manufacturers who are cited as 100x baggers, more so those where certain key numbers match. That is how I concluded it is Granules India.

I do not track this company and therefore I stated as much in the post that ‘I am not able to tie up certain numbers but the overall story seems to add up. Those with a position in the stock, please take care’.

There are some key numbers and yes on a consolidated basis, I cannot find related party loans/other payables. But that should make us look deeper and appreciate the method, instead of dismissing the approach outright.

And if we were to verify each and every item we post, well, lots of third party reputed research reports would not be posted here

2 Likes

@mpbajaj53 The posting has been simplfied by @darshit quite well…While I agree I cannot see the issue, the thing is there are red flags in the company-relatively unknown auditor, Hyderabad based company(I’m not racist but there are several Ahd/Hyd based companies which have conned investors  ), complex accounts, complex industry(Pharma), standalone accounts inflated by merger of WOS into parent.

), complex accounts, complex industry(Pharma), standalone accounts inflated by merger of WOS into parent.

Hi Darshit,

I doubt there are many API manufacturers who are cited as 100x baggers, more so those where certain key numbers match. That is how I concluded it is Granules India. And I have read the article

I do not track this company and therefore I stated as much in the post that ‘I am not able to tie up certain numbers but the overall story seems to add up. Those with a position in the stock, please take care’. This is not a random post. Some key numbers below, which will not proving related party tunnelling/capex over spend at consolidated level, however may indicate some issues at standalone level.

Hi Anandh,

agree it may be with ref to granules india, but his point of related party trans with respect to corporate guarantee on loan taken by jv company is grossly wrong. It is recognised as a contingent liability only, not sure y his software sends a red flag for this, by dat way majority of Indian companies will be a red flag. Parent company giving corporate guarantee on loan taken by subsidiary compny is a natural thing, (parent nahi dega toh kaun dega) it cannot be treated as a liability in Parents books as per accounting unless the auditor finds it very probable of subsidiary defaulting on it.

3 Likes

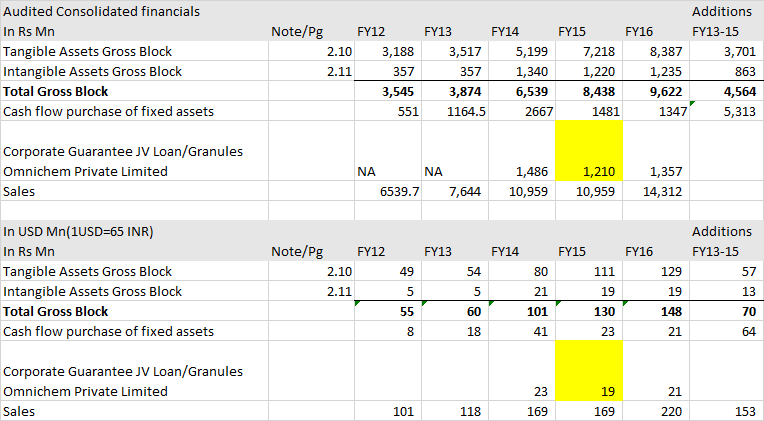

Point taken on the Corporate Guarantee, but the following is just a coincidence?

Between FY12-15, new additional sales

created were US$78.7m, which eerily matches the following

cash outflow: total cash outflow in capex; related party loans

(US$15m); other payables (US$4.4m); intangibles (US$17.8m). Based on tunnelling analysis, the cash outflows from relatedparty

loans or related-party investments/capex are re-routed

back to the listed company to artificially inflate sales.

I can’t figure it out. ![]() Or does the answer lie in what @kv1 posted - “depreciation which is 52.7 Cr in 2014-2015.” ?

Or does the answer lie in what @kv1 posted - “depreciation which is 52.7 Cr in 2014-2015.” ?

Disclosure: Invested

great find. Sold my positions today.

all this is meaningless - let this firangi confirm he was referring to granules and let the company clarify if someone forwards it to them - shooting in the dark as this is not behoving for a forum like this more so when a)we are unsure if the co is granules since the numbers do not match and b) specifically whats the issue in question - i see nothing wrong in the corp guarantee at all . as for the other point i am unable to understand it . Personally I rate granules mgmt quite highly and feel its highly unfair to have discussions as this without giving the co an opportunity to clarify.As a forum we need some responsibility since reputations are built over many decades.

3 Likes

“During FY13-15, the Indian pharma firm added US$41m in gross PPE but reported US$89.6m in cash outflow from capex addition.”

At exchange rate of 65, this means Gross PPE addition of 266 cr, while cash outflow from capex of 582 cr.

There seems to no number which is exactly matching these ones. The closest seems to be consol capex of 531 cr.

As can been seen, 3 year capex (531 cr) is higher than Gross PPE addition (403 cr).

However, here Capex is Purchase of Fixed Asset & fixed asset also includes Intangibles here. And since, they have increased, capex looks different than Gross PPE addition.

But if we look at 3 year Net Fixed Asset Increase, which also includes Intangibles and then add back D&A expense over the three years, numbers seems to be nearly ok (505 cr v/s 531 cr).

Anything wrong you guys find with my calculations?

P.S- I am not an accounting expert, so feel free to correct me if I am making a mistake in calculations/ conclusions.

1 Like

I also sold my small tracking position today. As per my limited understanding; the cash flow spending on fixed assets should account for the increase in fixed asset less depreciation. That does not seem to agree in this case. Cash spending 148.1 Cr, fixed assets increase about 71.6 Cr. Adding in depreciation cash spending to cover the increase in assets should be 124.3 Cr. There is still a large discrepancy in my opinion, and hence I exited. There are some small sale of assets etc. that still don’t account for the differences. These are all numbers just for FY 2014-2015.

Hello All,

I actually have a query beyond the issue. Assuming that there indeed was a back-ploughing of funds, the company would have had to increase the sales significantly higher in the immediate next year to be able to show the growth that they have been doing. Few things to quickly check might be

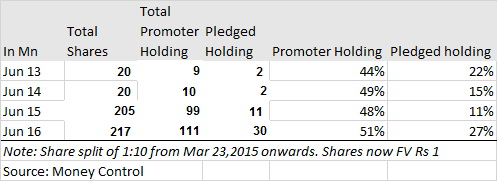

- Has the promoters or associates sold any significant shares in the mentioned period? Unlike that they would want to jack up price without benefiting from it.

- Is there any such discrepancy observed over multiple years or is this just a one time occurrence?

- Every year there seems to be equity dilution. Is it preferential allotment? Is there a need to dilute equity when debt is constantly falling?

I agree with Darshit. Inferences drawn from reports from third party, not regularly investing in India, should not be posted here. What if it turns out that this is not Granules at all or points highlighted are inaccurate? Are we not creating speculation with may be a malafide intention?

Thanks for asking Granules investor to verify but you cannot straight away blame a company without your checking the facts and validating thoroughly. Else it is just a rumour and must be condemned in this forum.

Disclosure : Invested

4 Likes

@darshit-As per proportionate consolidation principles, JV is consolidated line-line to the extent of parent’s ownership interest which is 50% in this case. The balance 50% debt is off balance sheet

@reacher-The corporate guarantee is to a 50% Joint Venture and not to a wholly owned subsidiary. Therefore, we cannot quite ignore. And nowhere in the annual report can I see the breakup of the amount of debt/ being consolidated, although they state that it is included in the consolidated financials. **Also yes the company could be asked to comment, but given **

@jk321 Even my table shows that the capex and cash flows roughly match which is distinct from what @kv1 has seen. The issue is not free from doubt and I would exercise caution.

@Yatharth-The company is undoubtedly Granules India-I post the link to their website where unlike the quarterly report they have stated "We also avoided an Indian pharmaceutical company supplying active pharmaceutical ingredients (APIs) in paracetamol/analgesic/pain, ibuprofen/analgesic/arthritis, metformin/diabetes etc that is touted as “the next 100-bagger stock” by a brokerage house. …"

We may disagree with the analysis but not with the company or the intentions of the poster-if you read his blog you would realize their value investing passion. And they do invest in India as their portfolio breakup by country shows. In fact, they have a much wider view having seen frauds in Singapore, China etc.

DisclosureNo positions in the stock.

The analysis made by the author of the note can’t be substantiated with facts and figures as we also did a deep dive into Granules about an year back and had similar apprehensions. I have never invested in Granules but it has got nothing to do with the analysis shared by @andy161161 of Kee Koon Boon.

It is a note on Granules I prepared more than a year back and shared with few friends to decide if it’s investment worthy in Aug 2015 at about Rs. 120/- (appx) … (reproducing verbatim)

My take on Granules is …

-

They are focused on OTC and high volume, large market drug segment where their scale, efficiency and established track record with customers like Glaxo Smithkline (Panadol) and Mylan etc would give them clear benefit over long period of time.

-

Auctus purchase is also to mine the API they (Auctus) has in large volume OTC segment.

-

Omnichem JV is a front loaded investment bet. They expect revenue of Rs. 150 - 175 cr by 2020 with 25% margin … So, 50% would come to consol books. Nothing much to add in next 2 - 3 years as nowadays FDA approval etc have a much longer gestation period. I differ from India Nivesh here, they seem to be over optimistic.

-

Their new Gagilpur facility is extremely impressive … Tablet capacity is utilized only about 35% - 40% … Even though FDI approval has come but customer approval / customer disengagement from their previous contracts are still due. I don’t think it’s an easy task and also possibly they need to invest again for API facility to make FD.

-

PFI is a word they invented … It is nothing but adding other non-active (excipients) substance to the API for making it consumption ready and next stage is Final Dosage (FD) preparation. Entire process is automated … Hardly 100 people in the shop floor in 2 plants (Gagilapur & Bonthapally). I am unable to figure out why they require 2000 employees … I am told most people are in loading / unloading / inspection / administration / housekeeping / FDA compliance / record keeping and purchasing.

-

Fixed asset break up is

Gagilpapur PFI and FD facility ---- Rs. 410 Cr.

Bonthapallu API facility ---- Rs. 45 Cr.

Gedimetla API and PFI facility — Rs. 120 Cr.

Bonthapally (II) Intermediary ---- Rs. 7 Cr.

Granules USA Virginia ---- Rs. 25 Cr (the facility they purchased from Valiant Pharma)

Granules China ---- Rs. 40 Cr.

Granules Vizag — Rs. 20 Cr.

-

Coming 2 - 3 years they plan to invest heavily (as also mentioned in India Nivesh report) … But if you see past 5 years also, they invested heavily and Free Cash Flow got eaten by Fixed Asset Purchase … To me unlike other typical pharma company, Granules struggles to generate free cash flow in any real sense and their loan book is always growing. The largest plant in the world of Paracetamol at Bonthapally has only Rs. 45 Cr. gross block. So, it is the low margin, high volume, high asset turn money spinner for GIL. Here they seem to have no traction over pricing power or payment terms with their customers. But margin will improve when FD capacity utilization goes up.

-

Problem with Auctus is their plant is FDA approved but the APIs are not … Unless they get these APIs approved, making use of the plant for US / Europe sales is difficult … They have to get API manufactured elsewhere and can use customer DMF to start manufacturing from Auctus facility which seems a farfetched idea for me. But they can continue to sell locally from Auctus facility (as you can see their domestic revenue growth last year was much higher than export growth)

-

Related party transaction — Large sales is done through US subsidiary and the receivable from them is also quite high (refer excel file attached) and it sales at no profit basis to capture market share by circumventing local distribution. I am not sure how much success can be possible … We need to see it unfolding…

-

Corporate Guarantee of Rs. 120 Cr. given by GIL to Omnichem JV for the loan taken by the JV. They plan to share the guarantee 50:50 with Omnichem but not yet successful

-

Subsidiary loan of Rs. 60 Cr. taken from banks at LIBOR + 400 … refinance being pursued at LIBOR + 150… It is not a intercompany loan.

-

Granulles China makes no profit but company objective of having this set up is to ensure Raw Material supply and I think it’s OK.

-

Auctus intangible of Rs. 88 cr. is depreciated over 45 years as per present book keeping … A minor but mentionable point!

-

Promoters have other interest in Vineyard etc… Unlike most other pharma promoters http://krsmaestates.com/

Overall, It has entrenched position in what they do and can’t be dislodged. But the scope is almost constant. To get out of it, I think company is trying many things but it will take time for these to materialise… till date it is an investment led growth story… Going forward they can transform to a real pharma company but according to my understanding will take more time than the market is thinking. And this constant increase of related party sales / receivable and continuous increase in FA purchase is something I find hard to neglect.

Not an investment worthy idea for me at present. Will check again next year (2016).

End of note

Encl.: My working on Granules. I am indebted to @dd1474 Dhiraj Dave for reconfirming my finding on the company numbers.

Mandatory disclosure: I am a SEBI registered investment adviser (regn. No INA 100004814) and run a webbased advisory https://aveksatequity.com. This stock has not been recommended to paid advisory members.

GIL CF Working August 2015.xlsx (25.2 KB)

20 Likes

- The numbers show that the promoter holding has been increasing via open market purchases between Jun-13-Jun14, and further via a preferential allotment last year. While the MD was accused of market manipulation in 2002, he was acquitted by SAT and they don’t seem to be playing the market.

2)The article is a multi year analysis over 2013-2015. We need to watch for 2016 onwards

3)The data shows dilution majorly only in FY 2015-16 probably to increase the promoter stake beyond 50%-which is legitimate

Fair enough, but which company will clarify/admit wrongdoing on accusations against it? Anyways, the reason I posted on this thread is that for folks like @aveekmitra and others who have analyzed this threadbare, it is a pointer for them to look at. This will be a learning for all concerned. And it is good to know what others think, since these reports sometimes move the market.

Your numbers are wrong because the conversion rate you used is wrong. Rupee was around 48 on avg in 2012 and in 2013 it was around 53-54 but moved to 65 as you pointed out in H2. If you do that your consol Capex = Cash Outflow

1 Like

The discrepancy between the ‘Purchase of fixed assets’ in the cash flow statement and the additions to gross fixed assets which is being highlighted is explained by the capital work in progress.

Taking the example of FY13,

1)Purchase of fixed assets is 11,644.61 lakhs

2 )Addition to gross tangible assets is 3,377.15 lakhs

3) Change in capital work in progress over the previous year is 10,880.24 - 2,929.63 = 7950.61 lakhs

2+ 3 comes up to 11327.76 lakhs which is almost equal to 1.

Any company which is really cooking its books is unlikely to do it in the blatantly egregious manner the person is suggesting leaving huge unexplainable discrepancies in the financial statements.

2 Likes