Thank you very much Ankit. Much appreciated

As granules is foraying into b2c through its OTC basket, i wondered if that might bring some extra margins. Anything around 30-32 % in 7-8 years would be pure delight if at all possible. (A 26% sales growth would convert to 35% profit growth if that could happen). Also, its FDs proportions would increase to 65% in long run which are again higher margins.

Would need the help of @Rokrdude@amitayu

PS: Maybe one should ask this in the earnings concall?

FY20 target of 5000cr looks far-fetched now. My rough estimates suggests we can expect around 2000cr topline by FY18 and close to 3000cr by FY20. There could be potential upside to the numbers if they get lucky with one of the 4 molecules they in-licensed from USpharma - Windlas (like Torrent and Alembic got lucky with Abilify as some of the other players who also had approvals faced problems just at the time of launch), do some other acquisition or can ramp up CRAMS business at a very fast rate.

The opportunity to supply directly to retailers like Walmart in OTC market would mean they can fetch better margins compared to what they are getting supplying via Perrigo, L.N.K but according to my understanding it will still be less than 20% for most of the products atleast in the initial few years. Remember it will still be a B2B business and not B2C and pricing power will remain with retailers to some extent. I believe going directly should be looked more as getting more as well as consistent business (at a slightly better margin).

Most of the margin expansion above 20% will come from changing the product mix among FD itself (rather than changing mix from API to PFI and FD) as well as scaling CRAMS business which is a slow and gradual process. I will be more than happy if they are able to maintain margins between 22-24% for next 5-7 years. You need to understand that the company is trying number of things at the same time, and some of those things/plans won’t work as expected. Lastly going by their recent interviews and actions it looks like Granules wants to follow Perrigo model where 50% of company’s growth comes from acquisitions, which has its own set of risks.

Thanks a lot again Aman. Whats your thought process in the fact that in intial few years the margins would be less than 20% for OTC? Is it because of smaller order size? I thought that Krishna Prasad was claiming that since there were only 2 other (major) players in OTC market (one being perrigo), the margins would be extremely attractive regardless of pricing power. My thinking process was that initially, the margins would be low due to smaller order size. But once granules starts getting larger orders, it should get a substantial increase in margins until more players start entering. The reason I think this should be the case is because retailers are also fragmented. Walmart might be a gigantic retailer but I guess KP would be aiming to sell to many more retailers.

But, this is just my amateur guess. Please correct wherever you think I made some errors or omitted some factors.

PS: Given your estimates on sales by FY20, which is very reasonable and 22-24% terminal margins value, the company looks like a 24-26% profit compounder for the next 4 years without major surprises.

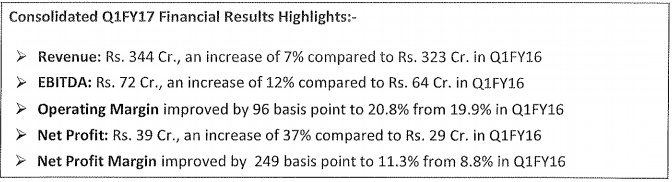

Looks like a changing accounting method from IGAAP to IndAS made us believe a modest revenue growth, which otherwise was a robust 20% YoY (416cr vs 346 cr).

When asked about the long term vision for the company during the AGM, the CMD replied that they intend to be recognized as a global pharma company that is well respected and known for its highest ethical standards! Quantitatively, he replied that they obviously intend to be at a lot higher level than where they are now but didn’t provide numbers.

I attended Granules conf call. my conf call notes:

The lower revenue in Q1 FY 17 is attributed to rationalisation of product mix, lower API pricing leading to lower revenues due to linkage in raw material prices. lower revenue was also due to change in accounting std. revenues from omnichem JV were not added in consolidated financial statements. only the profit was reported in ‘share of associate’

The management indicated that they are concentrating on margin improvement rather than sales growth.

The management mentioned about US FDA approval of Ibuprofen Rx. The revenues from the same were

Rs170mn in Q1FY17.

Granules has entered into an agreement with Par Pharma, US, to market the generic version of

omeprazole and sodium bicarbonate OTC product in the US from July’16.

Granules plans to file 7-8 ANDAs from India and US in FY17. The co has filed two ANDAs with US FDA in Q1FY17. The company has five approved ANDAs and one pending ANDA with US FDA.

Granules plans to increase API capacity of guaifenesin by 2,000tpa and paracetamol by 3,000tpa to meet additional demand.

Omnichem JV and Biocause JV generated revenues of Rs420mn and Rs310mn, respectively,and profit of Rs40mn and Rs30mn, respectively. The management expects Rs1.8-2.0bn revenues from Omnichem JV in FY17.

any idea what’s the current size of their OTC products (volume/$) business that they do with walmart and one more retail chain? How is it that the management sees this as a game changer with significant gain in traction in 2018-2019?

A leading Asian value investing firm has analyzed Granules India, and they suspect some accounting fraud there. While they have accused(without naming the company but it is obvious from the description-100x bagger, business model and certain numbers tying up)…Page 9 below http://www.8iholdings.com/media/ref_investmentupdate2016.pdf

I am not able to tie up certain numbers but the overall story seems to add up. Those with a position in the stock, please take care We also avoided a listed pharmaceutical company with business prospects that looked promising on the capex rampup. However, our accounting fraud detection system alerted us to the inconsistency in a larger divergence between Gross PPE (Plant, Property, and Equipment) addition reported in the balance sheet and the capex figure reported in the cashflow statement. During FY13-15, the Indian pharma firm added US$41m in gross PPE but reported US$89.6m in cash outflow from capex addition. Between FY12-15, new additional sales created were US$78.7m, which eerily matches the following cash outflow: total cash outflow in capex; related party loans (US$15m); other payables (US$4.4m); intangibles (US$17.8m). Based on tunnelling analysis, the cash outflows from relatedparty loans or related-party investments/capex are re-routed back to the listed company to artificially inflate sales. This corresponding match of increase in sales and cash outflow in unusual items should not happen since revenue is recorded when there is a sale of products, not when money is lent to one another or when a new plant or production line is set up. Furthermore, it made a corporate guarantee to related parties that was perhaps improperly reported as an off-balance contingent liability under Indian GAAP instead of reporting it as financial liabilities under FRS 39. As a result, this entity’s net worth would have to be reduced downwards from Lakhs 3,610 (S$7.3m) by Lakhs 12,096 (S$24.5m) to become negative. We all know the risk implications when loan guarantees turn sour, with the prominent case of banks seeking out repayment of loans taken out by colourful Kingfisher beer tycoon Vijay Mallya, chairman of United Breweries. Mallya allegedly personally guaranteed US$900m in loans to Kingfisher Airlines, which stopped operating in 2012.

Don’t waste your time with this company. They are a Singapore based company that claim to make millionaires out of everyone for a certain fee. Enough said.

Please do some research before posting random stuff.

Kindly avoid posting articles without verifying the authenticity of the article. I am writing this coz i got this link in few watsapp groups mentioning accounting fraud in granules India posted in valuepickr, which infact the article perceives to be in a leading pharma company. Kindly read the article before posting anything. This seems a foriegn fund , firstly does it mention Granules India, secondly does it mentions a Indian Pharma company in it, then how u did u conclude its Granules India-is it the only pharma company globally doing capex. Assuming its Granules India, did u verify the numbers they are talking in the article, except the sales number and other few numbers nothing correlates to the company. On rough approx numbers the cash outflow from investing in FA is close to 520 crs frm FY13-15, while the addition in gross FA in granules from FY13-15 is roughly 470-480 ccr (including 98 crs recognised for Auctus pharma acquistion in FY14). Also did u check the networth the article is mentioning of 3610 lakhs or 36.1 cr, its netwoth was 275 crs in FY13.

When asked about the long term vision for the company during the AGM, the CMD replied that they intend to be recognized as a global pharma company that is well respected and known for its highest ethical standards!

First a disclaimer. I have been invested for last 3 years so my views will be biased. I’ll try to be as objective as possible.

The post that @andy161161 highlighted is definitely regarding Granules India. It says “the Indian pharma firm” and the Gross PP&E and CFO also matches perfectly in USD. Regarding share capital of Rs 36.1 cr, it is the share capital of Omichem JV (see 2015 Annual Report)

Now commenting on the whether we should believe it or not, I don’t think we can totally ignore it since the CIO (Kee Koon Boon) maintains a blog https://bambooinnovator.com/ and if you go through some of the articles on the website, it seems there is a good process and rationale behind each of the companies that have been analysed on the website. So I think it is upto us to do further investigation.

Aman bhai wat u want to analyse, who ever this kee kaa is…he is saying that whatever capex (cash outflow in capex) granules did in fy13-15 (520 cr or 89 mn $) , plus $1.5mn (90-100 cr ) related party loan (which infact is a corporate guarantee on a loan that jv company has taken, so its just a guarantee by granules india, not a loan ), plus any intangibles (which again is recognised for auctus pharma acquisition) is all fraud and they all are equal to additional sales figure from fy13-15. So by that thesis, Auctus is only on paper, So basically kee kaa is saying Granules took money from bank for capex n all, did only thoda capex, and rest all is money going out from granules and coming back in the form of additional sales !!! He has a great accounting fraud detection system which itself seems a fraud system. But i like the confidence with which he says

" Based on tunnelling analysis, the cash outflows from related party loans or related-party investments/capex are re-routedback to the listed company to artificially inflate sales."

As Aman said, the burden is on Granules investors to rigorously check the weight of accusations by the report. We cannot simply brush it off. There is an asymmetry of harm involved here. If the accusation is right, there is a good chance of huge loss of capital for investors. If it is a false alarm, then its business as usual. We should thank @andy161161 for bringing this up irrespective of whether this turning up to be a false alarm or not.

From the 2014-2015 annual report, in 2014-2015 about 148.1 Cr was spent on fixed assets.

On the fixed asset side on the balance sheet we see an increase of about 71.6Cr in fixed assets from previous financial year.

which itself seems a fraud system. But i like the confidence with which he says

which itself seems a fraud system. But i like the confidence with which he says