Can you please elaborate how Granules is going to benefit? Will they manufacture the product and sell and pay some kind of royalty to the company with which they have inked a tie-up?

Thanks in advance

1 Like

Here is the the ET interview video:

Pledging 11,10,000 shares (out of his total holding of 7,92,30,610 share) constitutes only 1.40% of total holding.IMO Small amount of pledging means literally nothing.

This might help

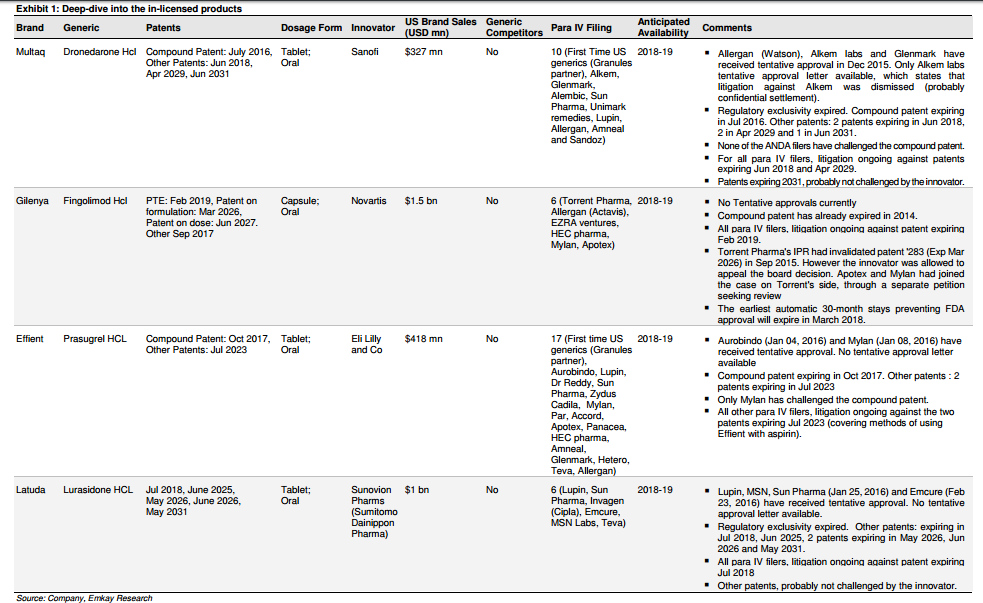

Source http://www.emkayglobal.com/Uploads/EmkayResearch/Granules%20India%20Event%20Update_100616.pdf

3 Likes

Again Krishna Prasad Pledged 33.9 Lakh Shares On June 28th

can somebody through light on " why this pledge?". My limited understanding is that it is not a good sign. Pledging may lead to uncertainty and volatility in stock price. Conservative investors should not buy shares of companies where promoters have pledged shares. Is my understanding correct?

His pledged shares are about 16% of his total holding - even though not ideal, I wouldn’t be worried just yet.

But further disclosures on reason for pledge may change my opinion.

-

There was an investor meeting today(04JULY2016) with few Mutual fund houses. How can we know the highlights of todays meet.

http://www.granulesindia.com/investor.html … Under Notices&Disclosures

Direct link given below

http://www.granulesindia.com/documents/Notice-disclosures/Intimation%20-01.07.16.pdf -

The website is redesigned. Looks appealing.

-

He has again pledged his shares. Any idea why he keeps pledging his shares ?

I know he finances the debt requirements of the company. But Is it primarily to increase his stake to have an even bigger pie… ?

If so I can recall what Peter Lynch said about promoter increasing his stake

Does all this point to a new beginning of something big that we should expect ?

I’m confused, isn’t he decreasing his stake by pledging the shares and facilitating debt?

And what did Peter say exactly? ![]()

1 Like

Peter Lynch said there could be many reasons, why promoters reduce their stake and not necessarily because the outlook is poor. But there could be only one reason why a promoter increases his stake.

1 Like

2016 Annual Report is out http://www.granulesindia.com/documents/Annual-Reports/Annual%20Report%202015-2016.pdf

Highlights from my reading:-

-

The report highlights how the PFI business (which incidentally was conceptualized by Granules only) provides benefits to the customer which in turns lead to more customer stickiness for Granules

-

How the company has over the last decade moved up the value chain- Started with OTC Monographs (Paracetamol), moved to OTC ANDA (Ibufprofein,Metformin and others) and finally moving to RX Generics and RX Innovation with launch of molecules like Abicavir. GRAN has been able to change product profile from 66% API to 44% API resulting in margin improvement from 12% to 19% in FY16.

-

Number of triggers are lined up for the company over next 2-3 years are:-

-Expansion of capacity of Metformin and Guanfenesin,

-Scale up of CRAMS from Omnichem JV with possible USFDA approval in FY18

-Foray in OTC market as a direct supplier to the likes of Walmart directly (2006 AR which can be downloaded from Granules website is a good read on understanding the OTC market)

-Development of newer complex molecules from Granules USA

-Marketing tieup with Par pharma for Zegrid OTC

-Possible USFDA approval of the 4 Inlicensed molecules from Windlas Pharma could lead to significant addition to topline in FY19-FY20

One of the negative thing I found in the Annual Report is the very high remuneration of the management which is currently at 16% of net profit (Although according to annual report it is within the ceiling as per company’s act) Remuneration at the maximum permissible limit according to companies act. Over the years remuneration has grown at CAGR of 60%/64% in last 5/3 years compared to profit CAGR growth of 41%/53%.

Disclaimer Invested so views are definitely biased. Do your own research.

16 Likes

Thanks a ton Aman for the highlights. Will definitely give 2006 & 2016 AR a thorough read. Btw, what’s the ceiling value on renumeration of the management as per the company act?

Hi Nishant,

It is normally stated as 10% of profit calculated as per the section 198 of companies act. The thing is profit reported is mostly not the same as profit calculated as per the company act. I tried to read more about the same and also read other annual report. But there is wide discrepancy in the stated method of calculating it. Moreover the management can always take permission in the shareholders meeting to bypass the limits.

1 Like

As er AR - "In the year 2016, a huge portion of patent drugs, amounting to USD 150 billion are going to expire worldwide. As a result, the Indian Pharma companies shall get rights of manufacturing drug formulations that were previously licensed to only the patent holders. Thus, the scope of earning more revenue and profit is expected to be witnessed as demand for those medicines are on the upper curve."

From where we can get verified this info and also which are the possible companies will get benefit of this in near future.

Thanks Aman . One more point which need to be watched is how Auctus performs in this year Fy17 . Auctus products are mainly complex molecules which Management are banking to convert into FDs in U.S. and in Europe by themselves possibly with some partners. Real margin will be coming from there. They expects there will be a healthy bottom-line and top-line from Auctus in this year that will lead to increase the share of FD’s part in total revenue (Currently 34%).

Granules India Limited has informed the Exchange regarding a press release dated July 14, 2016, title “Granules Pharmaceuticals, Inc., a wholly owend subsidiary of Granules India Limited, entered in to an agreement with USpharma for acquiring its stake”.

Link: https://nseindia.com/corporate/NSEBSE_14072016100709_025.zip

I just wondered that given the structure of the company and its strategic plans for the future, would it be possible for the operating margins to touch 28-30%, 5-6 years down the line if the company executes what it intends to do?

Is it too much to expect or does it look feasible?

@Rokrdude @pikrohit @ankitgupta @crazymama does the business model for such b2b pharma companies in general allow to attain such levels of operating margins?

I am just trying to figure out the best case scenario given everything gets executed as intended. This would be helpful to get a upper bound expectation on OPM.

Hello team,

Below are my observations and some doubts after reading the Annual Report 15-16.

Observations:

Long Term Borrowing Decreased by 24% YOY comparison

Short Term Borrowing Increased by 29% YOY Comparison

Company focouse on Vertical Integration

As US Patents will Expire in 2016 many new Companies can come in which can result in Decrease in Margins

Started construction of 7,000 TPA Metformin and 2,000

TPA Guaifenesin API block at Bonthapally plant

Started construction of 3,600 TPA PFI block at Gagillapur

plant.

ANDA Approvals in FY 17 from Varginia .

This will increase the business for Granules in coming years .

Some Doubts i Have.

Not able to understand CRAMS business

High Court Case on GIL Lifescience Pvt Ltd

Share Warrants

Altough Long Term Borrowings came down but Finance cost increased by 18.52%.

Also while computing some ratios , i found Ratios like ROCE etc are stated wrong on websites like moneycontrol & screener. I always trusted them but now i doubt .

Disc: I am Invested in Granules also will hold for some good gains as i beleive earnings will improve with New Plants and OTC products.

Fellow boarder will be graetful if you guys can help Thanks in advance.

Rokrdude,

I digged into previous posts in this thread . Do you think this target of 5k crores revenues by fy2020 looks a little too ambitious now?

On Fy2016 base, it ends up being around 36-37% sales cagr.

Warmest regards

Hi Nishant,

I dont have much idea about Granules as I havent studied it but I think achieving an operating margin of 28 - 30% is tough for a b2b players (doesnt mean that it cant achieve). But there are companies which have such margins like Gland Pharma. However, these companies are into niche segments like oncology, injectable etc.

1 Like