Have added to my position after recent fall at ~228 levels. Soda Ash Price has been sky-rocketing globally, along with low valuations, GHCL could be a cyclical multibagger. I expect risks of over-supply in textile segment to continue, and have also initiated a short position in IndoCount limited to hedge some of these risks and express this view (IMHO ICIL valuations don’t price in cyclical collapse)

Dear sir I do not find any news of hike in prices of soda ash? Could you please share the source of news.

Refer following link for various commodity prices. U will get daily, weekly and monthly prices

soda ash is up 37% since first aug. Company can show better results in coming quarters however it depends on the contract to suppliers. Any idea how are the rates decided? What is the correlation between spot prices and GHCL sell prices of Soda Ash?

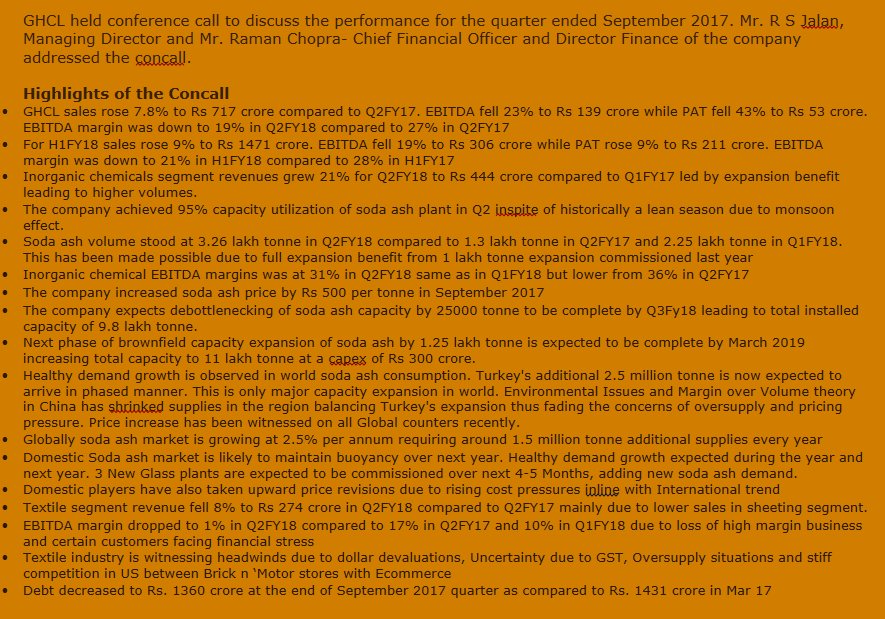

Disclosure: source of concall transcript is from internet so need to verify its authenticity.

This could be one reason

HDFC SEC RECCOMENDED UNDER TRADING IDEA YESTERDAY

Ghcl again recommended by Anand Rathi securities for target of 272. Unable to understand what is happening in this counter.After a massive loss in textile business, why such securities are recommending it? Senior members are requested to come up with some insights.Is it cheap valuations of ghcl which is the why it is being recommended or something else?

Following are few reasons:

- Soda Ash rates have appreciated and company has hike its prices in September

- Additional supply for Turkey will be coming to market in incremental fashion

- Higher capacity utilization levels

- Lower single digit valuation

@malayruparel these are all known to the market for quite sometime now. Nothing new. The question is why its being recommended immediately after a very bad quarter with a huge upside by many analysts/brokerage houses now?

Disc: Invested

Regards,

Suhag

As market continues to stay high, lack of available opportunity having favorable risk reward may be the other reason. I too was tempted to sell on result day but didn’t as felt that risk reward is favorable at CMP.

Disc: invested.

At every time majority of info is known to everyone, its just when and how you interpret it.

I am no expert to tell why brokerages are recommending now, my guess would be due to lower valuations and considering all points mentioned by malayruparel are valid … Brokerages are trying to find value in this overheated market and included this in their recommendations.

Caution : Considering the past of promoters, I wont rule out any foul play either.

With current cash flows and even if i keep future growth projections at their minimal , I am ok holding it for next couple of years… Hope some day in near future they demerge Chemical and Textile business to unlock the value ( that will be bonus )

One should anyways refrain from commenting on a) stock price movements which are largely random and are inexplicable and b) brokerage recommending it cause they are in general recommending everything to buy and have many ulterior motives. Yes, results on a consol basis have been very bad and when something hits a rough phase, it doesn’t just come out of it in one month, business, in general, suffer from inertia - both positive and negative.

Now coming to soda ash prices, I think it is level 1 thinking (as howard marks talks about level 1 and level 2) which is basically a perfunctory analysis of the case - first of all soda ash prices in any case cant be high for a long enough time because outside India, it is pretty much a commodity and supply always increases if demand is increasing (and there is no reason why the demand should sustainably increase at a higher growth rate - its not lithium that suddenly all electric cars need it). To me, it looks like some temporary supply side disruption which has increased the prices in the international markets in the short term but is unlikely to stay that way coz fundamentally, supply is increasing because of Turkish capacities while demand sources are more or less the same.

Moreover, has anyone cared to investigate the fact that GHCL reports such a smooth pattern of EBIT margins in Soda-ash over the past so many years - this means that they barely fluctuate the prices of soda-ash to their customers and are in essence working under long-term contracts and prices - because if the soda-ash prices as supplied by GHCL were to increase inline with global prices then it should have crashed many times in earlier quarters also resulting in wildly fluctuating EBIT margins in soda-ash segment which hasn’t happened - so I don’t think this temporary aberration of soda-ash prices globally is going to have much impact on their domestic soda-ash business, please correct me if someone has spoken to management and has information to the contrary.

This time they have revised the prices, this can make some difference in coming quarters as they do operate on long term contracts.

Soda Ash - Rs. 500 per MT in Sept 2017

RBC – Rs. 400 per MT in Sept 2017 and

Rs. 700 per MT in Oct 2017.

Source : Investor Presentation for Q2 results.

Considering volume in last few days and price movements it appears to be close to a breakout if sustains 270+ on closing basis in next few sessions:

Target could be length of the pole from breakout region if market and Soda ASH price supports in medium term.

Pros :

- Strong Soda ASH price and recent capacity addition.

Cons :

Weak textile business

DSP Black Rock micro cap mutual fund has done bulk deal for buying GHCL at 272 for 950528 shares.The stock has not performed in last 1.5 year. Lets see how prospect of GHCL will change in future especially after q2 with headwinds in textile sector.