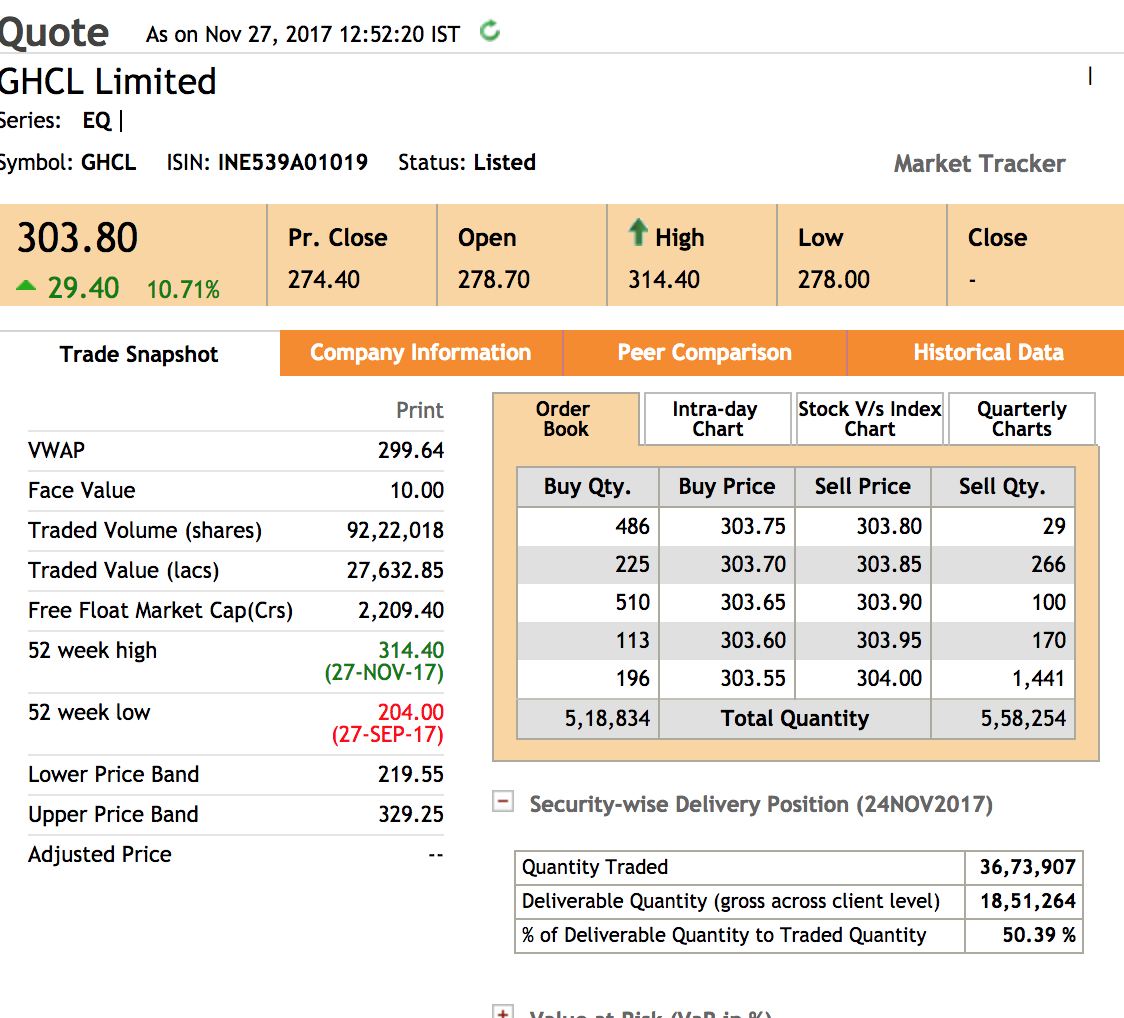

Price of Soda Ash is cooling down, I hope textile unit performs this time ( Quarterly numbers on 31st Jan). Or else it may go into consolidation again.

![]()

Source : Sunsirs.com

Disc : Invested

Textile continues to be a pain point, but Chemical performed well.

Q3-FY18 numbers:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/123a9427-8aa9-46c0-82e2-bc0f680afc6b.pdf

Any idea what was the other income of 20 Cr? Also, the power and fuel cost seem to have gone up sharply?

Loss of 7.87 crore in textile segment as compare to previous quarter loss of 6.04 crore, however inorganic segment is performing very well. Textile segment becomes continuous loser.

How Raymond is able to give stellar results and Ghcl is still laggard.

Sudden increase in fuel,water and Power cost of about 10 crore is unthinkable.

I will welcome all senior member to throw some light on future prospects of Ghcl.

Disclaimer: holding 3500 shares of ghcl at price of 252 for almost 2 years.

I was looking at Fuel cost as percentage of revenue over last few quarters and this is on rise:

I could think of two possible reasons:

-

Increase in Crude Price. Since they have their own raw material mines, hence fuel could be considerable expense.

-

Though textile is not doing very well, still the input costs are increasing even though its yield are low. Hence it increased the Power and Fuel cost as percentage of Revenue.

@ayushmit Sir, I am not aware of “other income”, we have to wait for conf call and can ask about this :

Friday, 2 February 2018, 16:00 hours fST

Please dial in at 15:55 hours IST

Dial-in numbers

India: (+91 22) 3938 1079

http://www.bseindia.com/xml-data/corpfiling/AttachHis/234c37a1-c6c5-4c65-b17f-cb75e64f7c5c.pdf

Guys, I wont be able to attend this as I will be in office around that time. Hence if anyone joins please ask about the future of textile business, Other income details and increasing Fuel Costs.

Disc : Invested for more than one year and no transactions in last 3 months. Views Invited.

Company presentation

http://www.bseindia.com/xml-data/corpfiling/AttachLive/264ca6a3-b202-49ec-88a4-2bbf0a07d57b.pdf

Here too they gave some hint around Power expense being high for Textile:

EBITDA for Q3 FY 18 is impacted due to low wind season (Impact: 7 Cr)

I was listening to the recording of Conf call and here are some notes based on my understanding. You may either listen to call recording at researchbytes or wait for transcript to be made available by company in few days.

Chemical :

- Chemical business is doing very well and would continue to do so.

- Capacity utilisation for last 9 months at 97 % ( too good)

- They are adding further capacity in this.

- Turkey Capacity already there at 1 Million tonne and would reach 2.5 by Q1 FY 19.

- However the impact of Turkey expansion likely to be reduced due to Dumping Duty and strengthing Euro.

- China not considered a major threat at this time.

- 1st Feb they increased price for Chemical product ( Soda Ash) by 2 %.

- Inspite of Capacity addition and good utilisation, they have not compromised on margins and they have increased as compared to Q1-FY 18 and Q3-FY 18

Textile:

- This took majority of questions from Analyst and other investors on the call

- Headwinds to continue for next few quarters

- They have got two major segments, Spinning and Home Textile

- Spinning is doing well however Home textile is the one under pressure

- Though they mentioned Spinning constitues the major chunk however while giving revenue breakup he said

Home Textile : 800 Cr

Spinning : 400 Cr

- Major investments are also going to Spinning only

- They are coming up with some innovative product by March-18, which is made from recycled polyester. Hence would be environment friendly.

- They feel US consumers, who are concerned about environment, would like the product and give some relief to textile devision.

- They procure the major raw material ( Cotton) for almost for complete year. Current Cotton stock would last till Nov-2018.

- Hence any short term spikes in Cotton price would be taken care of

- They agreed to their margins being lower as compared to some competitors and they are working on it.

Here is the report from Emkay ( their analysts was present in call and asked few questions). This too covers few details from the call with some number projections.

20180202_GHCL-Limited_21_QuarterUpdate.pdf (561.3 KB)

GHCL’s FY19 numbers should be better than FY18’s: RS Jalan

Capacity expansion of 1.25 lac MT of soda ash schedule to be completed by March 2019 will result into major increase in revenue of Ghcl. Is this the reason why RS Jalan is saying that profit of Ghcl will increase by next year or anything else?

All views are invited and welcomed.

My understanding with Ghcl is that it can be holded by atleast 1.5 years from now onwards in order to take advantage of capacity expansion which ultimately will reflect in shares prices

Please correct me if I am wrong at my thought processing.

I was attending akshar chem concall, you guys might wanna chk out china and prices of soda ash…

Saying this because they said east china has already started production…

I think they mentioned caustic soda as major RM for dye intermediates…not soda ash. GHCL is into soda ash.

Ghcl has posted quarterly results for q42018.Inorganic segment has performed very well.Textile segment has reduced it’s losses on quarter on quarter basis.Rekoop brand has been launched in textile segment in which great interest is shown by customer as per management.Overall 10 crore PAT has increased qoq basis,however it has declined on yoy basis due to lagging performance by textile segment.Requesting all to share their views on future aspects of Ghcl.

More information on Rekoop

Results are on expected lines, Management had already told that Textile would take few more quarters to recover. One has to be little patient here as the story would take some time.

Overall I am bullish on this company from FY 2020 prospective.

Disc : Had to reduce my position due to another better opportunity, but I may increase it in coming quarters as textile starts showing signs of improvement.