I don’t think the issues with the Soda Ash division and Textile divisions are the same. The management clearly said that the Turkey capacity expansion will force higher cost players to close down and that the Turkish producers would be weary of flooding the market with excess capacity because it is them who also stand to loose from a lower price. A similar situation has played out in the past with the Chlor Alkali industry, where high cost Western producers are forced to close down. Since GHCL is the lowest cost producer in India (?) I wouldn’t be too worried about the next 2-3 years.

The textile division seems to have a much shorter cycle than the Soda Ash business and the textile cos that I’ve looked at (Indo Count and Welspun) seem optimistic about a recovery by FY2019. Of course, its still not clear what is behind this slowdown (cotton price/stronger currency/pressure from retailing clients/pressure from end users).

I’m also uncertain where GHCL’s textile division is placed relative to Indo Count and Welspun. In increasing order of value added products and forward integration, I believe the order is GHCL, Indo Count, Welspun. Maybe this has allowed GHCL’s textile division to increase margins while the latter two had lower margins?

Invested almost 1.5 year ago with 3521 shares with average price of around 252 rupees…Till now it has not given any positive returns…But I am going to hold this for more 1 to 2 years from now keeping in mind of turkey expansion of capacity…But one thing is sure market has not rewarded this company…It is highly undervalued…All suggestion are welcome…

I am not sure why textile reported loss , this was surprising. Maybe more info will be provided by company in investor presentation and the conf call scheduled later today at 4:30 PM IST

Unfortunately I wont be able to attend due to some urgent meeting. Incase someone attends please do check about the bad state of textiles and way ahead.

The only good thing i see in the results is upward price revision of Soda Ash and RBC in Sep & Oct 2017 and the upcoming additional capacity. Not sure how much that can compensate for subdued performance of textile segment.

Textile capacity utilisation is at 77% and with additional of new capacity, it will come down even further.

I am trying to understand textile sector better and last few quarters results of IndoCount & GHCL are definitely worrying however as per below article recent changes in GST will help Textile sector both export and domestic consumptions.

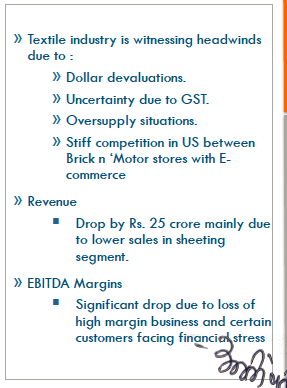

The thing is GHCL lost high margin business and their main clients are facing financial stress as per company presentation. How much GST reliefs can help when you are losing business that’s the question we need to ask.

Not to worry, even Soda Ash price has increased in last month or so… However company’s performance is dragged down by Textile hence we dnt see much price action here.

Valuations r giving comfort to hold on till textile turns around…