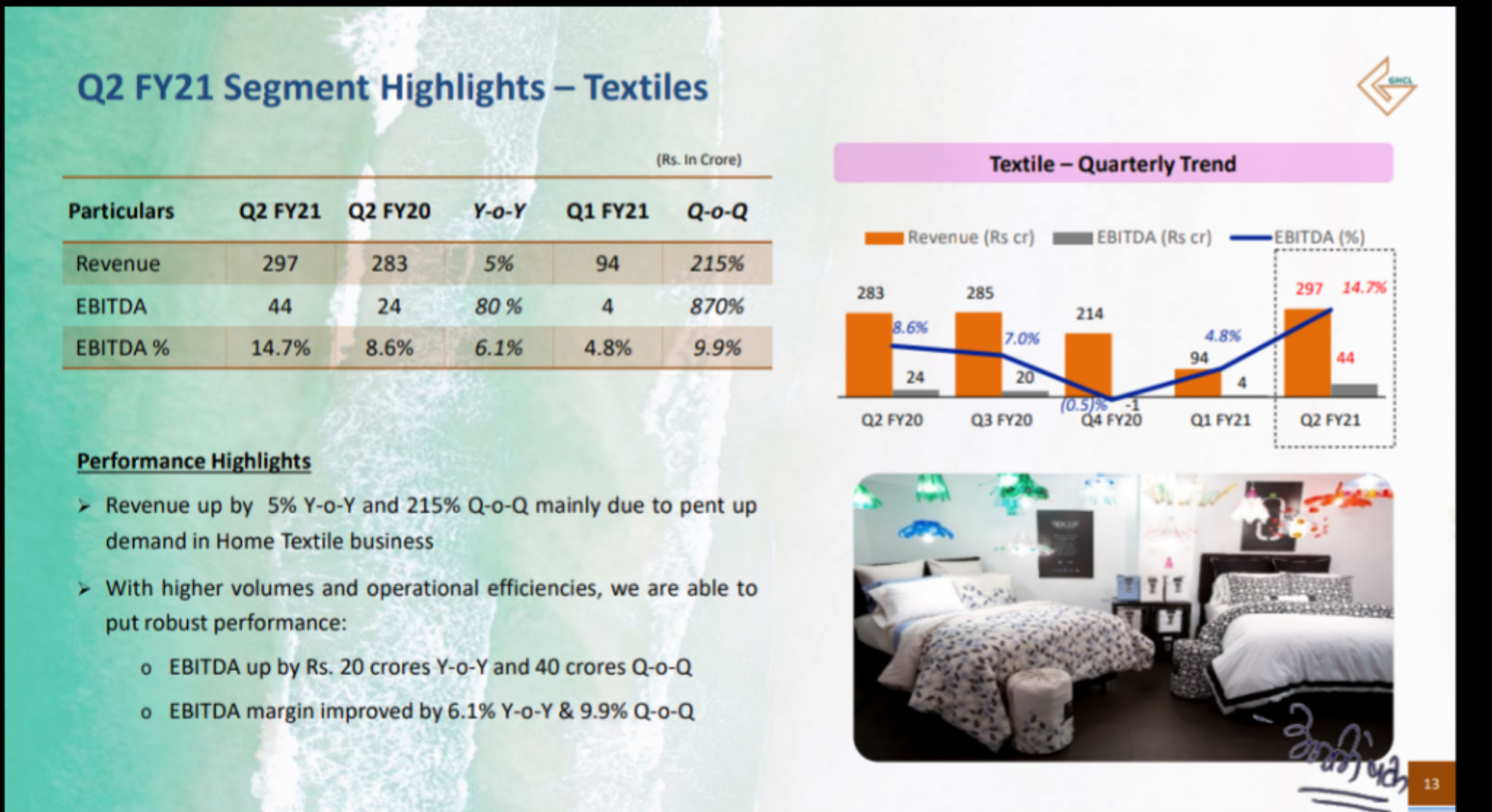

Frankly speaking… textile segment was a surprise this quarter… I hope the trend continues though the company says pent up demand from US and Europe. More important is the acceptance of its products for me …

Was it the best quarter till date for textile or close?

Can anyone investing in this one for demerger arbitrage share thr views abt potential value unlocking. Below are my rough back-of-the envelope estimates : -

FY21 figures : -

Soda Ash

Textile

Sales

1887

961

EBITDA

489

157

Value of stable Inorganic chemicals + Salt+ other = 7 X EBITDA = 3423 crs.

Value of textile segment = 3 X EBITDA = 471 crs.

Total = 3894 - 605 (Total Debt) = 3289 crs.

Current Mkt Cap. = 2365 crs.

As per mgmt concall the process will complete by Nov-Dec implying an IRR of 60-70%.

The risks are the usual mkt crash risk, Soda Ash fall in prices ( minimal), any other impact on textiles biz till Nov - Dec

Views invited.

Disclosure : - Invested from Demerger arbitrage perspective. Traded in last 30 days.

Textiles topline has been more than1000 crores for last 4-5 years. But EBIDTA margins have been quite volatile. The margin assumed above seem to be peak margins due to increase in spinning spreads. More sustainable number could be 9-10%. Inorganic chemicals topline should be more than 2000 crore annually. Was depressed due to low sales in Q1 FY21. Net Debt could be higher probably around 675-700 crore by the time of seperation.

Yes. Taking into account volatility of textile margins, I adjusted the EBITDA multiple. If debt of additional 100 crs. is adjusted & further adjustments are taken into account & that drags the IRR down to 30%, still a worthwhile bet IMO. Wat say

Agree. Also given its long track record of 20%+ RoCE in Soda Ash business, integrated and low cost operations could get someupside in Soda Ash business. I think the biggest factor dragging the stock is low promoter holding.

I see low promoter holding as a good thing esp for both businesses after demerger. A hostile takeover bid may happen ala L&T - Mindtree types. Lots of PE & estd players will find both businesses as a reasonable takeover target.

I had asked them a question during the last concall. on whether post separation would the promoters want to exit one business and raise stake in another. … Unfortunately the response was -ve. Though they were indicating each business could do own tie ups and related strategic decision.

Hostile takeover was a possibility even now (such low valuations for a consistently high ROCE player) but none happened till now.

All m saying is that probability of Hostile takeover will increase post de-merger bcoz :-

Dedicated Focused businesses vl be in play

Thr will be sm forced sellers in either of the businesses

With unlocking, the sale with fetch higher values so you never knw who\how many vl be tempted

Basically, coming bk to my original discussion point, how the present investors value both the businesses? How mch they agree/disagree with my valuation? How mch are they expecting of the value unlocking part?

Hostile takeover due to demerger unlikely. If any one wanted they could have bought the company as it is and then disposed of the part of the business they didn’t want.

Forced selling-Textile part may see some but it is a small part. If you study the funds holding it there don’t seem to be any who would be forced sellers due to size restrictions etc.

Valuation wise no doubt about the attractiveness. Apart from EV/EBIDTA, one can see Replacement value. The last soda ash unit was set up by Rohit Surfactants (Ghari Detergent). They spent 4216 crore for 0.5 MTPA unit. While GHCL has 1.1 MTPA capacity. My understanding is that GHCL is more integrated than Rohit Surfactants.

Got your point. The difference in individual opinion is wat creates value opportunities. So much for Efficient markets . The ‘any one’ from my viewpoint will not have bothered to go thru the selling the unwanted business exercise themselves & would hv very much preferred taking over the focused established business esp considering the promoter is doing that separation effort on their part.

Anyways, good to hear your views regarding the valuation. Keeping aside the hostile takeover part, I blv this will fit as an arbitrage bet in my basket of such investments. Invested & might increase allocation to it till Nov.

The stock can double from here. Sizeable debt reduction both in the Textiles and the Chemical segments. Demerger could lead to value unlocking not only for chemicals but more so for the standalone textiles unit where with the considerable reduction in debt the standalone debt for the segment is now around 270 crores and ideally should continue to head south.The Chemical segment with debt of around 450 crores is likely to be a contender of a rating upgrade and as per the recent management guidance was operating at 95% capacity. Stock has the potential to see quick upward price trajectory as we head closure to the demerger post Q 1 results announcement.

Though the prices of soda ash are improving it is the business that is showing no improvement in revenue and profits from the last few quarters…the cyclicality of the soda ash with excess capacity is suppressing the margins of the business…the company is not having any pricing power/ competitive advantage other than some captive raw material. Though the demand is expected to increase in near future raw material costs and power costs may impact the profitability.

There is chance that company may not get re-rated even after demerger.

Moreover, promotors are selling the shares in open market when they are already having low promotor holding issue, is matter of concern.

. The ‘any one’ from my viewpoint will not have bothered to go thru the selling the unwanted business exercise themselves & would hv very much preferred taking over the focused established business esp considering the promoter is doing that separation effort on their part.

. The ‘any one’ from my viewpoint will not have bothered to go thru the selling the unwanted business exercise themselves & would hv very much preferred taking over the focused established business esp considering the promoter is doing that separation effort on their part.