Total price hike by 12% for soda ash done by GHCl.This will majorly benefit in next quarter.As per management, Soda ash is in upswing with china now becoming a net importer of soda Ash.

Textile division is at its best. Registered one time loss of around 4 crores due to tautae cyclone.Demerger is on the cards.

Disclosure:Invested from 166 levels and still considering it’s at dirt cheap valuation on comparing with it’s peers.

All two engines of Ghcl i.e. Soda ash demand & textile segment are on fire. With demerger on cards and looking its cheap valuation in comparison to its peer, I think Good time for Ghcl are ahead.

Demerger will unlock the value lets see how fast management responds for demerger process.

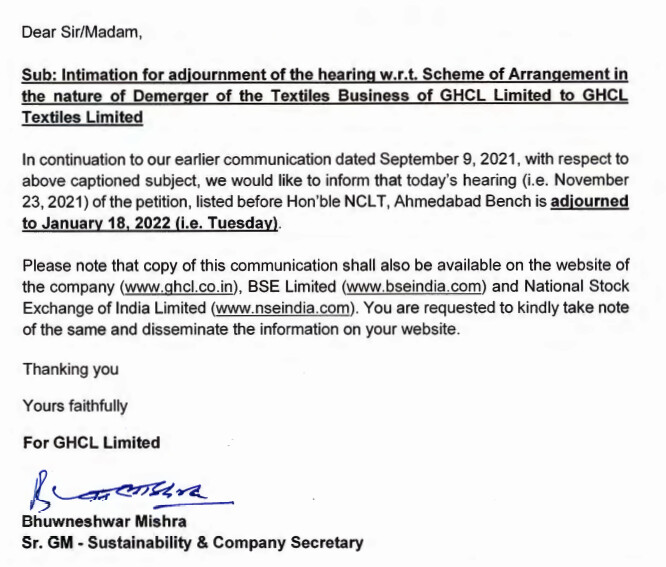

Final hearing at NCLT is at 23 Nov 2021.I think both entity will trade separately from 1st week of December.Imo management of Ghcl has delivered on the time frame of demerger. PLI scheme for textile sector will further strengthen the Ebita margins of company.

Great avenues are opening for Ghcl which has largest soda ash plant at single location in india. Use of soda ash in lithium ion battery for EV theme, flat glass in PV solar cell in renewable green energy & use of sodash in flue gas treatment for pollution control can be a win win situation for Ghcl and other sodash producers.

Dis. Invested from 166 levels and continues to hold.

Asking purely from portfolio allocation POV, if u dont mind disclosing, how mch %age of ur portfolio is allocated to this stock?

Also, based on few recent developments including the one u posted above, Why/Why not are u considering to average up on the stock?

As disclosed earlier, I am holding this stock purely from demerger arbitrage perspective & a cpl of drivers after my initial buying have made me to consider averaging up. The IRR becomes better if we move closer to demerger & the stock remains undervalued which seems to be the case here.

My portfolio is highly concentrated. Ghcl is major part of my portfolio. I have avg. Buying price of 166. There are other opportunities in market like Marksans which is also deeply undervalued in which i want to deploy my cash. This is just to avoid further concentration of portfolio.Because at the end of the day you are not running the business and you donot more about the company more than promoter. If it is not major chunk of my portfolio, I would definitely employ my cash at Ghcl looking at present scenario and future growth drivers.

Thanks for the clarificatn. For me, this is one of the rare cases whr m thinking to keep\add the chemicals business once the demerger plays out. The business prospects certainly seem promising as for now.

1)Ghcl able to maintain Ebita margins despite inflation in RM cost.Superb performance of textile division helps in achieving that.

2) Price hike in soda ash has already been taken place in this quarter which will realise 50%percent in q3 and full realisation in q4 due to long term yearly and six monthly contracts.

3) Price hike can be easily passed to customer due to demand supply gap. Demand supply gap is due to lesser production in china and increasing demand in glass of solar cells. Kindly note that soda ash is main raw material for glass industry.

4) Imo there will be upswing in soda ash cycle which will continue to exist for atleast 2 years. The same was also confirmed by management in the concall.

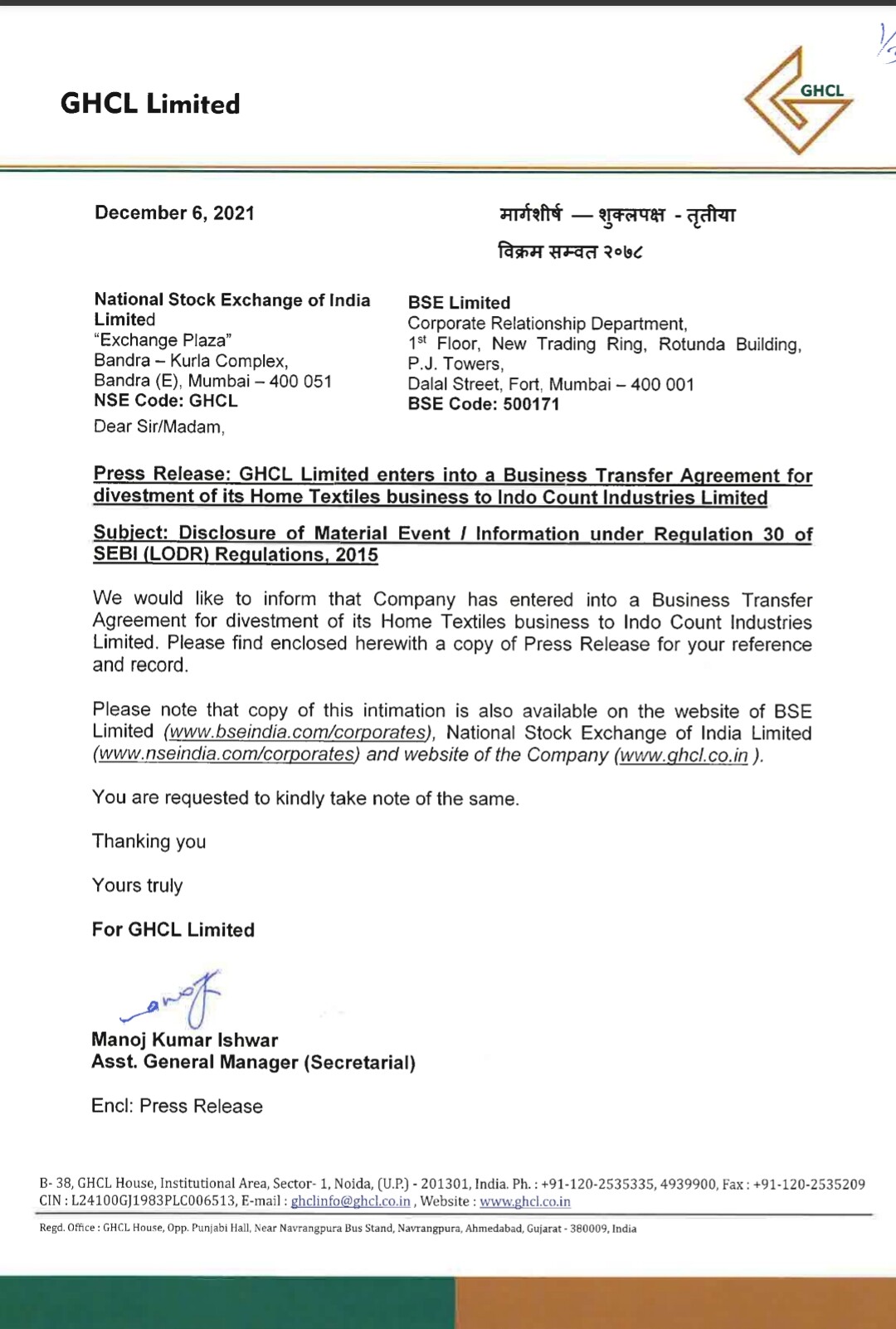

This changes the dynamics of demerger arb now. Wat will the mgmt do with the proceeds from sale? As new demerger scheme is to be filed, is the IRR from current valuations justified to play this out?