All as an investor I want is GHCL to be a business which generates high ROE, ROCE and pay high dividends which also makes a business sense. It doesn’t make sense to me to invest in a business with 10-11% ROE when the player has a business with 20%+ ROE. Valuations will automatically adjust to reflect the financial numbers.

A classic case is DCM Shriram where they have reduced their bulk fertilizer and Hariyali business since it didn’t make any sense to run them.

1 Like

But Still promoter holding is 19% this is the only thing that keeps me away from this stock

1 Like

Another quarter of stable performance. Despite the softness in demand and soda ash prices, the company has posted ~30% yoy growth in PBT this quarter. The operating margins came in stable at about 23%. The company generated a FCF of about Rs. 280 cr in 6M-FY20 and the debt was reduced by ~Rs. 180 cr.

Regards

SJ

4 Likes

India Rating & Research - December 2019 - Rating A+/Positive. Rating reaffirmed and Outlook revised to positive from stable.

Latest Credit Rating report gives good insights in Soda Ash sector and Textile sector and also gives good short term earnings visibility of company.

Soda Ash Segment

-

GHCL is the second-largest domestic soda ash producer in India, with an installed capacity of 1.1 million tonnes per annum (tpa); the company meets around 25% of the domestic requirement for soda ash.

-

GHCL has integrated operations, with captive availability of all key raw materials, making it one of India’s most cost-efficient producers of soda ash.

-

GHCL increased its capacity to 1.1 million tpa from 975,000 tpa in the latter half of FY19.

-

Global soda ash demand growth remained flattish in CY18, driven by weakness in demand in China. Turkey’s new supplies were absorbed during the year without any significant price disruption due to the production constraints in China. However, the global economic slowdown is likely to weigh on demand in FY20, with weakness in end-user industries such as auto sector. Demand in China continues to be sluggish, while production has recovered in recent months, resulting in a drop in export prices.

-

Domestic demand grew by around 5% in FY19 and is likely to grow at similar rates of 4%-5% in FY20. However, the domestic market is likely to record an oversupply of around 200,000-250,000tpa in FY20 due to commencement of production from Rohit Surfactants Private Limited’s 0.5 million tpa greenfield soda ash plant as well as GHCL’s 125,000tpa expansion, which came onstream in 2HFY20. This combined with pressure from imports after the removal of anti-dumping duties is likely to cause a fall in realisations.

-

GHCL cut prices by 2%-3% in 1HFY20 and by another 4%-5% in 2HFY20. However, Ind-Ra expects margins to remain broadly stable in FY20 on account of operating leverage resulting from enhanced capacity, reduced coal cost, and favourable seasonality in 2HFY20. In 1HFY20, the EBITDA of GHCL’s soda ash division rose by 29% to INR3.7 billion (1HFY19: INR2.8 billion), with volume growth of 8% yoy.

-

Medium-term global supply-demand balance could tighten until end-2021, considering the absence of plans for fresh supply and increased sources of demand. The recently announced capacity expansions by global majors such as Solvay and Genesis Alkali are likely to come onstream from end-2021, broadly matching the projected global demand growth of around 2% per annum. This would result in a balanced supply-demand scenario post 2021.

Yarn Sector

-

The yarn division’s performance was subdued in 1HFY20 due to sluggish exports, resulting from a sharp decline in Chinese demand and weak domestic demand amidst higher domestic cotton prices. In 1HFY20, EBITDA fell by around 29% yoy to INR470 million, with margins declining to 15.7% (22.8%); the decline was restricted to some extent due to the storage of lower-cost inventory.

-

A new cotton crop from 3QFY20 might result in the segment witnessing better performance from 4QFY20. Domestic cotton prices have dropped seasonally, thereby improving the price competitiveness, with local cotton production likely to increase 13.6% yoy in the October 2019-September 2020 season on the back of increased sowing and above-average rainfall.

Home Textile Sector

-

The home textiles division has been facing severe headwinds since late 2016, driven by increased competitive intensity due to overcapacity and structural issues with the US retailers. The segment turned loss-making in FY18 and its revenue declined by 26% yoy. In FY19, the segment’s performance improved, with largely breakeven levels of EBITDA and flattish revenues. In 1HFY20, revenue growth remains elusive but EBITDA margins improved to 4%.

-

While the segment’s performance has been improving, its profitability remains significantly lower than the levels seen in FY17, when it had reported an EBITDA margin of 10.8%. Furthermore, capacity utilization was 56% in FY19 against the near-full utilisation in FY17 owing to decline in production and growth in capacity in FY18 (to 45 million meters from 34 million meters). The company has launched products with a focus on sustainability, which could bolster profitability over the medium term, while near-term performance is likely to be supported by its increased focus on its online business in the US.

Capex

-

GHCL is likely to spend around INR1.75 billion each in FY20 and FY21 to enhance soda ash capacity by 50,000tpa each by March 2020 and March 2021. With steady demand growth of 4-5% in domestic market, India is likely to remain a net importer even after the planned capacty expansion by GHCL and other industry players (currently, around 20% of Indian demand is met by imports).

-

The textile segment is likely to see capex of around INR250 million-300 million in FY20; a major portion of this amount would be directed to the yarn division. GHCL is also planning to set up a greenfield project of 0.5 million tpa in the next four to five years. The company is likely to spend INR600 million on land acquisition for the project.

Regards

Harshit

4 Likes

Finally co considering buy-back - https://www.bseindia.com/xml-data/corpfiling/AttachLive/784e0802-4f7b-41a3-b7a8-82f07ec02637.pdf

2 Likes

No doubt, movement in last few sessions with volumes did give a sign that something was surely cooking.

Indian Markets show results before declaration always ![]()

Would be interesting to see the buyback amount and whether it’s a tender offer or open market.

In 2017 it declared 80 crore rs buyback with Max price at 315 which hardly formed 3-4% of shares…

Currently they will be getting cheaper than 2017 price with a larger balance sheet size.

Expecting buyback of minimum 10% paid up capital (hopefully tender offer)

1 Like

Surprisingly low equity share buyback with maximum amount to be spent on buyback to be 60 cr. They seriously need to have a good CFO in place or get their priorities right. With the current EBIDTA, company could have easily gone for 10% buyback. It would have benefited shareholders as well as the promoters.

GHCL Q3FY20 Concall Summary

Business Update

- Slowdown in soda ash and weak performance of spinning business and retrospective withdrawal of MEIS scheme led to subdued performance

- The impact of slowdown in soda ash industry has been higher than expected both domestically and in global markets

- Expecting further softening of soda ash prices in the coming months which will lead to price correction of 2-3%

- Board has approved a buyback of Rs 60 crores upto a price of Rs 250/share

- Have reduced debt by Rs 200 crores during the year

Participants

- Dhanki Securities

- Kapoor & Company

- Kotak Securities

- Discovery Capital

- Sunidhi Securities

- ICICI Sec

- Securities Investment Management

- KM Visariya Family Trust

- Lucky Investment Managers

- Mittal Investments

- Principal India

QnA

- Expecting better performance from detergent and bottled glass industry which shoould stabilise soda ash prices

- The withdrawal of MEIS scheme should not have a big impact on volume growth in the textile industry

- Interest rates on loans have reduced to 8% due to healthier debt equity ratio

- Net debt figure as on Dec 2019 stands at Rs 1092 crores

- Long term pricing of soda ash has been very stable but in some quarters there are slightly lower/higher prices but on an annual basis prices are quite stable

- Due to entry of a new player in the soda ash business there has been an effect on pricing which has comealongwith tepid demand globally

- There will be no further inventory built up in FY21 and imports of soda ash are also expected to be lower which will help in liquidation of inventory

- The new volume from Mongolia will take 7-8 years to come onstream and that will mean additional supply of 1 million tonne every year

- A new capacity of 5 lakh tonnes pa will cost Rs 4000 crores and hence there are not many players who will committ capital to a new project

- The imports are coming from two countries namely USA & Turkey

- Have reversed the entire 4% benefit retrospectively as it has been withdrawn by the government

- Spending approximately Rs 150 crores in brownfield expansion of 50000 tonnes of soda ash capacity

- Expecting capex of Rs 250 crores on soda ash business next year

- Major benefit of fall in energy prices will be visible in FY21 and due to higher than expected decrease in soda ash realisations margins have fallen by an additional amount

- Not doing any sodium bicarb expansion this year and expecting sodium bicarb business to do well next year due to demand from NTPC for desulphurisation

- Out of total demand of India 25% of soda ash is being met by imports

- Capital allocation will always remain on the chemical side and till textile business performs on expected lines major allocation will not happen

- The promoters shares got invoked due to a loan taken for their company Golden Tobacco

- Expecting huge demand from flue gas desulphurization by power plants for sodium bicarb business

The company has declared buyback. How Do we participate in the buy back? As it open market.Should we just do a sell in our brokerage?

You don’t need to specifically participate. It is an open market buyback so they buy anonymously from the market .You can sell your shares anytime independent of who the buyer is

1 Like

Thanks for the reply

Is there a reason price has fallen to 100 rs now with P/E of almost 2/3 times with ROCEs around 20% (all as per screener.in)?

Is there a fraud here that the market is sensing?

Pledge selling by lenders in my view in such market. Promoter reputation does not help either. Check bulk /block deal data. Bajaj finance had been seller

2 Likes

Today GHCL accounced demerger of ghe textile business - https://www.bseindia.com/xml-data/corpfiling/AttachLive/95241921-2199-4b2a-b13c-97eb51026128.pdf

Looks like all set for the next move. Recent import curbs on the glass manufacturers could aid the soda ash players as its one of the inputs for the glass industry. Tata Chemicals moving up smartly. GHCL should be another play.

1 Like

Anti dumping duty on soda ash from Turkey and usa are on its way. Will prove great benefit for ghcl.5167a998-d007-4721-9119-f76edb4fd390.pdf (303.6 KB)

1 Like

TLDR;

Fuel Gas Treatment through Sodium Bicarbonate opportunity could be huge if the government supports it otherwise it is too difficult to bet on it.

I was going through the concall transcript. Treatment of Flue gas with Sodium Bicarbonate is being sited as the next big opportunity. So, I tried digging a bit about this process. Here are some findings:

- This process does not require any conditioning of the flue gas, such as increasing the relative humidity in the exhaust gas.

- The deposition occurs as a gas-solid reaction, usually at temperatures of 180C to 200C and residence times of less than 2 seconds.

- The actual reaction partner is soda-ash in the process.

- The higher price of bicarbonate is compensated for by the energy demand required for reheating the flue gases, which is necessary when using lime hydrate.

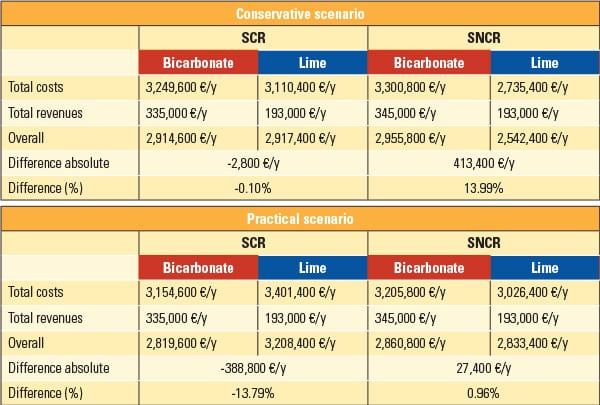

Cost Comparison between Lime and Sodium Bicarbonate methods:

The following parameters basically have a positive influence on the economic efficiency of the bicarbonate method, compared to the lime hydrate process:

- Low pollutant concentration in the exhaust gas

- Dropping additive costs

- Increasing energy prices

- Increasing disposal costs

Significant savings through the elimination of maintenance and repair costs as well as an increase in availability and a reduction in personnel hours could be noted. Quantification of these effects is difficult because of the quality of available data, so generalizations cannot be made.

Please note: Sodium Bicarbonate FGT is recommended especially at plants with the following conditions:

- SCR technology.

- Rising energy costs.

- Possibilities for commercial provision of heat.

- High disposal costs for residue from flue gas cleaning (possible recycling interesting).

- Low concentrations of acidic hazardous gases (especially HCl).

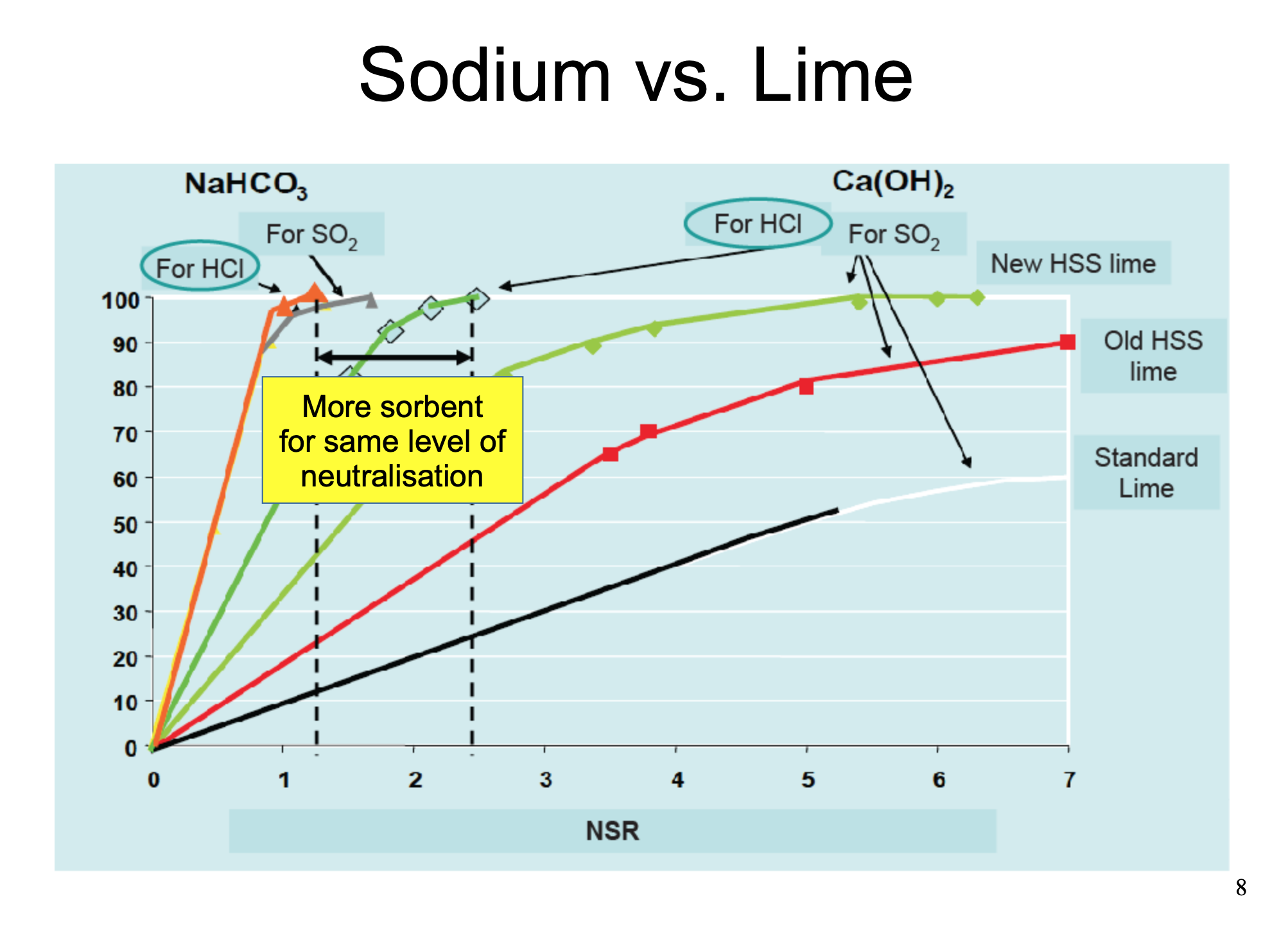

Another report gives similar prospects about Sodium Bicarbonate based Flue gas treatment.

Efficiency Comparison between Lime and Sodium Bicarbonate

Source

All of the above tell a promising story about Sodium Bicarbonate usage in WTE plants.

BUT

India is far behind in Waste to Energy sector. This article published in July 2019, shares the current situation. The summary is that policy framework is very weak to support WTE plants in India. It would require consistent support from the government to grow big. Here is a presentation by Agartala Municipal Corporation commissioner suggesting an action plan to the government.

1 Like

Just read the preliminary report of ADD on Soda ash (SA) imports from USA and Turkey. The reports says the landed cost would be around 266-275 $.The gap between the domestic price and imports is 20 dollars. 210-215 $ for USA and Turkey and Indian guy produce at 230$. The reports states that the domestic producers of SA are hurt because of imports. Although the ADD is not very profitable, this will increase realisation from 240$ to 260-270$ (still not very profitable).

Can you guys be more active. The company looks interesting.

1 Like