It is true that company has is virtually debt free (Although company avails overdraft facility and pays interest on it) and has stronghold in three districts of Maharashtra. However, annual revenue growth is marginal (less than 10%) and since Indirect taxes (excise, MVAT) eat away 74% of Revenue, Net margin suffers. Furthermore, higher cost of raw material adds insult to injury. One more thing that I would like to highlight here that since sales also includes indirect taxes component, any slight increase in taxes would also inflate the sales (it will not have any effect on net margin though) thereby giving the impression that the company is sales is growing. The company itself has admitted that high level of taxation and frequent changes in laws are common.

After seeing financial statements, one can observe that company rarely makes any effort to explain things, and occasionally has decided to omit useful facts over the years. For instance, company did not explain what exceptional items were in 2016, similarly we don’t know much about investment property, capital advances, deposit against demand in dispute, statutory liability. Although one thing can be inferred from note on capital work-in-progress that investment property also includes properties under construction. If company is engaged in manufacturing of country liquor, work in progress capital should have operation related stuff other rather investment property.

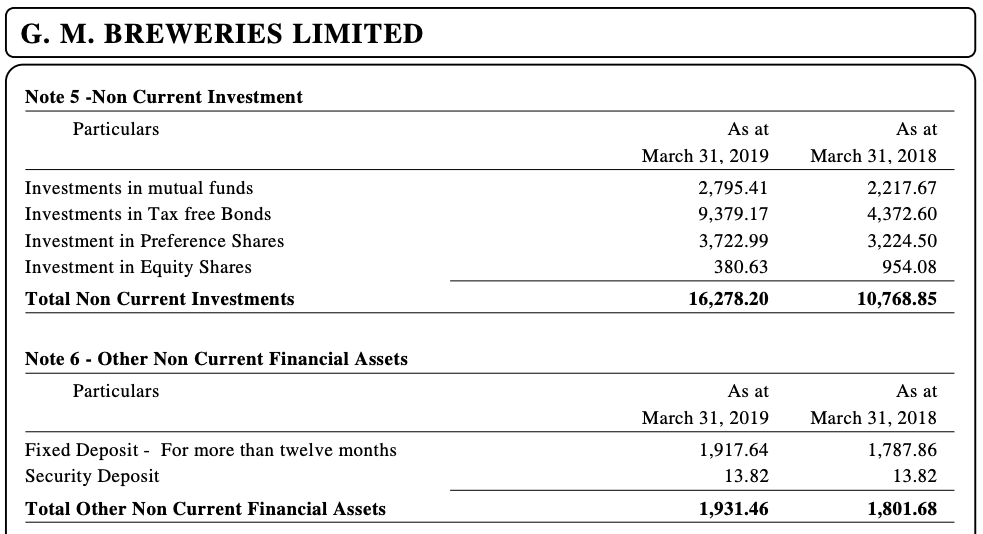

Furthermore, if you look at what other investment instruments company holds, you will get the feeling that the company is slowly digressing from its core operations and giving more attention to investments. For instance, the company is consistently increasing its assets in investment area (MFs, Bonds, investment property etc.) and at the same time, PP&E assets are decreasing. Now, one might argue that company has excess capacity and it is only utilizing 50% of that. I also agree, however for more than 5 years, company is staying that its annual capacity to produce country liquor is 13.76 crore bulk litres which is enough to meet the demands at least for the next Five years and the Company does not foresee any technological obsolescence for its products. Well, five years have already passed, demand did not reach close its its 13.76 bulk litre capacity. However, company is marginally increasing its capacity utilization over the years. But at this rate, company would need to expand its capacity in next 15 to 25 years and till then they have all the money to invest into other financial instrument. Why not use that money to expand its customer base in other regions of India.

Current ratio and quick ratio are also not very impressive.

Similarly, If you see CF statement you will notice that operating CF has one entry titled other Financial Assets – NC(Fixed Deposit) worth 19 crores that company redeemed in 2020. Correct me if I am wrong but it should be in investing section.

I’m also anxious about promoter/management, given the fact the Almeida family is taking home more than 5% of profit (PBT) which is fixed and not linked to any performance.

Disc: Not invested yet