Hi all,

does anyone know why receivables and inventory figures of this company are consistently so low? Seems like an outlier for a heavily taxed industry like liquor

I don’t think taxing has anything to do with inventory levels for any industry. But you are right in the sense that GMB has lower levels of inventory compared to the broader Breweries industry.

GMB is a cash and carry business. The regular GMB customers are people like this;

Not this:

They don’t maintain lots of inventory because they don’t have to. They produce according to immediate demand and everything gets sold on a cash basis.

1 Like

I’m not sure about the broader liquor industry but I know for a fact that the brewery industry shows its inventory inclusive of excise duty charges (as per law). I used to audit some brewery clients. In case regulations have changed in the last 3 years I’m not sure.

Also, No matter how low the inventory will be, there needs to be some especially as the company purchases ENA. Packaging and bottling material as well as store and spare parts and other nominal things like diesel fuel alone would be significant. These companies normally maintain 15-20 days of inventory in order to avoid stock outs.

Also, receivables, of the company should ideally be inclusive of excise duty and other taxes which can range from 100-300% of the total sale value as when they sell their cases wholesalers and distributors, it needs to recover its taxes already paid upfront.

3 Likes

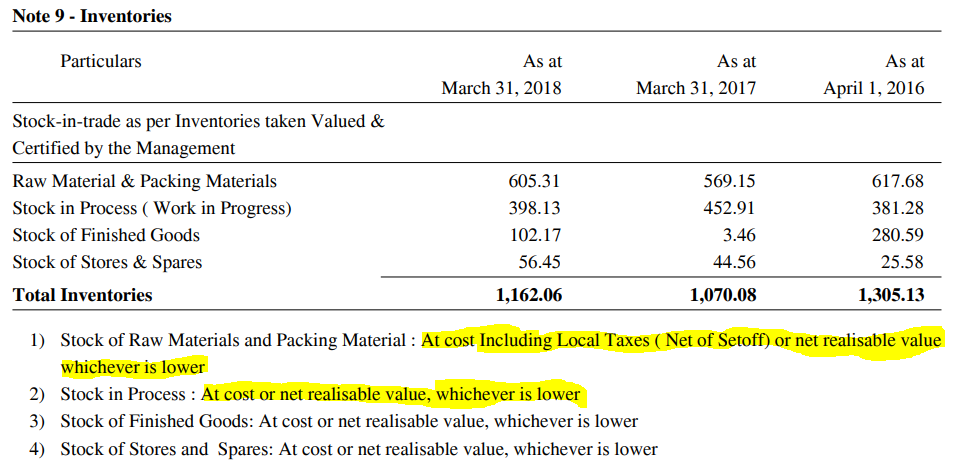

GMB’s Accounting Policy states how they record inventories:

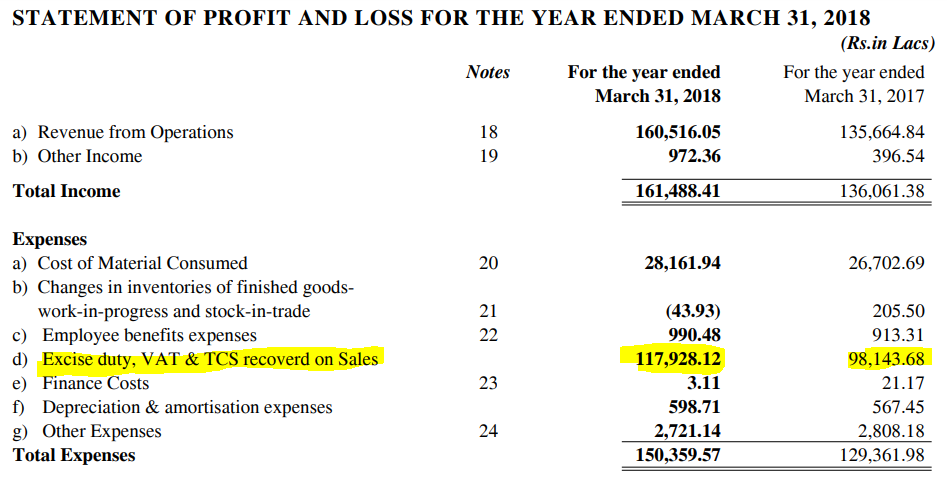

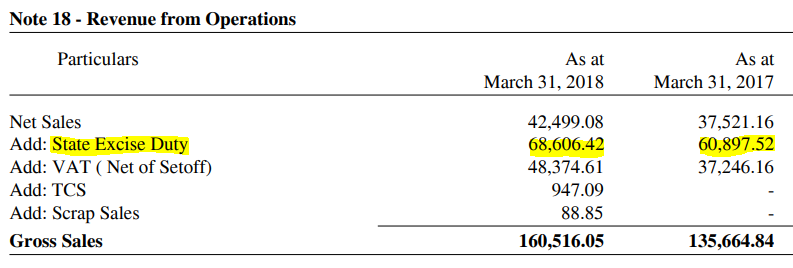

Here’s the Excise Duty outgo of the company:

And here’s the amount they can offset:

They also mention the following vide recognition of Excise Duty:

So, what I understand is that GMB recognizes Excise Duty related offsets only when the goods are sold. If there’s any gap in my understanding, please let me know.

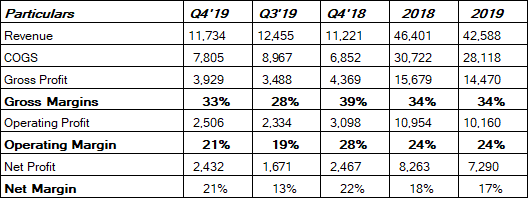

GMB has come up with a stable set of results. While quarterly results are variable due to raw material fluctuations, the yearly results are stable and quite good. The average ROE is 25% for 2019, which is excellent. The margins are great and have remained virtually unchanged from last year. Operating margin is at 24% and Net Margin is at ~18% for the last 2 years.

The cons are the the co is stingy is sharing all the cash it generates with shareholders and instead has opted to have a lot of investments on the balance sheet. This could be a cause for concern for some shareholders but i have chosen to live with it and have a smaller allocation of my portfolio to GMB.

The gross operating assets are roughly 1/4th of the balance sheet only. It has a very small operating balance sheet. The balance sheet is strong and there is no way the co is going to run into any financial trouble.

As far as inventory is concerned excise duty is to be netted off.

Best

Bheeshma

6 Likes

It is surprising for a cash-rich, debt free, company which does not require any substantial capital to have an average five-year dividend payout ratio of ~8%. About 25% of market cap and 60% of net-worth is locked in investments. Why does it need capital as capacity utilization levels are low with no capacity expansion, acquisition planned, these questions worry me.It is earning about ~7% return on about 60% of net worth. Despite that the overall ROE is close to 25%. What kind of capital allocation is this? Why will a promoter settle for ~25% ROE if they can generate ROE of ~50% by just getting rid of excess cash, unless he does not want to share the pie with shareholders. Had they been returning about 70-75% of profits for shareholders, I would have immediately taken a large position in the stock. Having said that, I trust their sales, the near monopoly status in Maharashtra. Every time I go to a wine shop about 60% of the crowd will be buying IMIL and of which 80% will buy GM. The questions around capital allocation are not letting me buy this.

SJ

Disclosure: No investment

4 Likes

Hi @jajushobhit

Not sure about their reach in entire Maharashtra. I think their monopoly status is in thane and surroundings.

This article read with the 2016 AR - suggests its market share in country liquor market of Maharashtra is ~27%. About 24.08 crore bulk liters of country alcohol were consumed in 2016. GM produced 6.35 core bulk liters in 2016. This amount to about 27% share by volume. GM also contributed ~900 crores to state excise from the 3000 crore contributed by the total country liquor industry, which also amounts to about 30% share in state excise. It would be fair to say that GM has about 1/4th to 1/3rd share in the country liquor industry making it quite dominant but not a state wide monopoly

While it would be nice if they could distribute more the shareholders. I think they have been fairly consistent in their distribution of cash. They haven’t skipped a dividend since the last 15-16 years. Dividend per share has not gone down. They have been giving bonus shares every 2 years since 2014.

The sense I get that within the liquor universe, its a fairly stable company with a fairly good long term track record of creating shareholder wealth.

As you pointed out, they could certainly do more with the cash they have and there is always a risk that there is something unpleasant going on behind the scenes that we are unaware of. These are unknowables and prevent one from taking a large position.

Best

Bheeshma

4 Likes

Improvement in capacity utilization to 51.82%. In the last 10 years, capacity utilization has dropped only in one year i.e 2014.

Source : AR

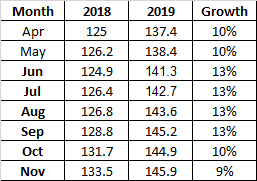

The co has quantified the impact of the increase in raw material and packaging cost in the notes to the results. Its approx 9.93 cr ( ~8cr due to rectified spirit and ~2cr due to packaging cost). On the plus side revenue has increased by ~8% yoy. The co has managed to increase revenues every year

Rectified spirit costs have gone up quite a lot. Find chart of rectified spirit inflation index from the MEA website ( https://eaindustry.nic.in)

2 Likes

Prices of rectified spirit are at a lifetime high as per data available at https://eaindustry.nic.in/display_data_201112.asp

Hopefully, we should see some moderation in the future (1-3 years) given the govt’s push to incentivize ethanol production. Both Sugar mills (1g plants) and OMCS (through 2g plants) are aggressively expanding ethanol capacities. Maharashtra Sugar cos are expected to invest 2300 crs. Currently, however prices of rectified spirit remain high. Can they go any higher? Ethanol prices for blending have now been linked to FRP for Cane and delinked from global crude prices. Our FRP for cane is the highest in the world. While Cane FRP has been hiked by 8% ( from 255/Quintal to 275/Quintal), the hike in ethanol procurement price through the B heavy route has been 10% (from 47.49 per liter to 52.43 per liter) and 25% through the sugarcane juice route (from 47.49 to 59.13).

Index , Base 2012 = 100

GM breweries stock price technical picture also suggests that the price may have found a floor. At the top of 966 it corrected and finally prices broke the support of 646. This was a about 320 points from resistance to support. This suggested a price target of Rs 325. Prices kept declining until they reacted sharply at 335 levels roughly around the bottom suggested based on price history and have also formed a nice classical looking cup.

P.S : invested and views are biased.

2 Likes

Some good nos on rectified spirit economics

Index Data from : https://eaindustry.nic.in, is suggesting that growth in the prices of rectified spirit may be tapering off after an unprecedented rise

1 Like

@dineshssairam , what do you think of valuations here.

MCap is 714 crs with Investments of 188 crs (as per Sept 2019) == 526 crs

Pre Tax Return on Tangible Asset is high due to Cash Basis Payment and Higher Inventory Change.

Whole company is available at pre tax yield of 19% with a dividend yield of 0.77%. I have not gone into the details of equity dilution over last few years but this is a really compelling case here. I would also like to keep myself reminded that growth and value are joint at the hip.

With average ROE of 25% and Reinvestment Rate of 90% , the co. can grow its earnings at sustainable rate of 22% which is attractive.

Is this a castle which is just having the sentiments weight in !

Pls have a look at where all cash generated is going.

Last I had seen bulk of cash was deployed in real estate, loans and advances and other current assets.

Also growth is a concern here.

Regards

My experience in last 15 years has been that moment a promoter gets interested in real-estate(except for new office/plant) it is time say good bye despite how good company or promoter has been in past. Real-estate can be used for n-number of things knowing how real-estate transactions happen in India. No wonder market gives thumbs up to any company divesting legacy real-estate.

2 Likes

It’s not equity dilution but issue of bonus shares

In my view GM breweries is a good stable co and has been run efficiently. The growth rate of topline is a steady 8-10% and in my view will remain so for the foreseeable future. The co has a policy of providing rent free accomodation to all its employees in the land adjacent to its factory. That said it’s true that it also is a little less with liberal with dividends than it should. Addn bottling capacity in a place like Thane and nearby areas will cost a lot of money and in my opinion the co is saving up for the day when production capacity hits it’s limit. As of now, there is sufficient capacity for at least 5 years with its plant running at 51% capacity and growing every year so it’s not that big a concern in my view.

While it’s main business is not cyclical its earnings certainly are as it’s principal raw material (rectified spirit) is a cyclical commodity. Of late the raw material prices seem to be tapering off and hopefully in a few quarters the impact will be seen on the bottom line. Let’s see how it pans out.

Best

Bheeshma

2 Likes

There’s a big chasm between “can” and “will”. The Self-Sustainable Growth Rate gives you a optimal growth rate without diluting capital. It does not, in any way, indicate that they will indeed grow at that rate.

Specific to GM Breweries, they have dug a trench in Maharashtra and actually contribute a LOT in taxes to the government. It’s a two-edged sword, but in any case it is worth concluding that they will continue their moderate growth of 7-8% into the next decade without any imminent threats (Unless it is in the form of government policy).

However, it’s equally easy to make out that they have no pricing power whatsoever. Read any of their Annual Reports from the last ten years and you’d find at least one sentence highlighting the fact that their customers cannot absorb the rising Raw Material costs. Indeed, if you think about the average GMB customer, it is the daily laborer / worker. Increase costs and he will just consume a little less. There is no winning here. If you have a special skill in predicting the price of Rectified Spirit, you may have an edge here.

The silver lining is in their entirely cash-based business model (Once again thanks to their customers), there is no need for Working Capital.

But what do they do with this cash? Some big Capex every half a decade or so, but mostly they sit as financial investments. And the last time I was tracking GMB a few years back, there was very little information on these investments or what the management intends to do with them. You’d think it’s easy for companies like GMB or CDSL to pay out massive Dividends, because they have literally no need for the money. They never do.

Unless GMB starts paying out more Dividends or makes better utilization of the liquid cash they have (Buybacks, Acquisitions), I wouldn’t personally consider investing in the company.

6 Likes