Beginning 2024 more than 2 million barrels a day of oil will be displaced by EVs and #lithium.

Beginning of a megatrend that will have to produce a total 12M T of #lithium by 2030, to have 200 million electric cars on the road worldwide.

Government of India slaps good and services tax (GST) of 12 percent on electric vehicles and 43 percent on hybrid vehicles. But both are eligible for incentives funded by the Centre.

in my opinion EV need solid and light structure so bet should be on aluminum and composite materials ,thermoplastics and carbon industries will be a good bet . along with lithium

The things which will not face disruption

mirrors

brake material

sensors and actuators ( Bosch will be major beneficiary sound magt with lots of patents and it is sailing in the 52 week low )

tyres / rubber

clutch wire / brake wire / cables

tyre beeds ( e.g ram ratan )

copper ( motors need wiring of armature Hind copper may be better bet )

handle and rubber gaskets

airbag material

seats ( mayor , harita seating jammna autos etc )

shock absorbers

…and more list can be explored …

electrical energy battery charger station

energy distributing companies …

regards

Adding a bit on Copper(source- Sustainable Copper).

EV technology is heavily reliant on copper, and copper demand for EVs is expected to increase from 185,000 tonnes in 2017, to 1.74 million tonnes in 2027.[3] EV manufacturing requires copper for multiple key components, such as batteries, motors, charging stations, and supporting infrastructures.

The more advanced the EV technology becomes, the more copper is required.[4] Internal combustion engines typically use 23 kg of copper, while hybrid electric vehicles (HEVs) use 40 kg of copper, plug-in hybrid electric vehicles (PHEVs) use 60 kg of copper, and battery electric vehicles (BEVs) use 83 kg of copper!

The biggest battery push will not come from EVs but Stationary power storage to go with Solar and Wind Power and provide 100% power to the grid.

i may have different opinion .in developed countries the user those who has installed solar power have an option to send the additional power generated via them back to grid and they are getting incentives .the amount of energy they send back to grid is minus from the actual energy they are using from the grid . in that scenario they don’t require storage devices .But you are right to an extent that they may require in the off to grid systems . The market of recycling or batteries is unorganised but has potential . in that case the emerging companies has large scope along with e-waste recycling .

The next question arises where will the existing automobile will goes .Does it will crushed or recycle or modified .if these goes to smelters the energy demand will increase or the rubber will be reclaimed from existing old tyres or the energy will be created by manufacturing bio fuel … The multiple questions and answers will comes in to picture …

It is there in India too and my friend has it installed. It is called as Net meter.

Lithium

Outlook to 2028, 16th Edition

Upcoming @Roskill_Info report on #lithium 10yr outlook to say demand will rise 5-fold and significant investment needed in new mines

This shows EV boom will start by 2022. Mining acquisition will have to start now…China has acquired best lithium assets all over the globe or hold majority stake in lithium, copper and cobalt mines.

As I mentioned before, unable to drill to direct beneficiary companies in case of EV disruption so earlier I thought that who ever wins EV race, they all will need motor insurance.

Now second thought is here, what about all the battery waste that is going to eventually pile up. There has to be focussed battery waste management and recycling. I was checking this space and found mostly start ups. Can anyone understand that which listed company today has this as its future focus area and will be well prepared for waste management out of EV battery. Will it be battery makers only or other might do it? Thanks

A pilot fleet of 3,000 buses, 100 ferries, two-lakh two-wheelers, 50,000 three-wheelers and 1,000 goods carriers are planned as part of this.

The State-run KAL plans to roll out 8,000 e-autos a year. It has also tied up with Swiss e-bus manufacturer HESS to assemble and later on manufacture e-buses, for which a memorandum of understanding (MoU) was signed on Saturday.

The plan is to make 3,000 e-buses for KSRTC. The KSRTC has already invited bids for 1,500 e-buses on wet lease this year. Thiruvananthapuram would have 100% e-mobile public transport within a year, he said.

Its actually interesting to see the subsidy being given for adoption of e-buses in India and each state announcing massive plans/nos to bring e-buses on road. Bringing these e-buses will provide comfort to the public + reduce pollution.

But look at subtle communication as to where EV stations will come at and who will provide power

NTPC and OMC are will be start and end point and state discom will be get fee for the same .

It does not matter which technology will dominate in 2025 ICE or EV or gas , if OMC can become final retail point - they are better hedged

Now comes what happens to current low cost producers of Autos like Maruti , Bajaj and Hero - That is uncertain

Tata Power signed strategic

MoUs to set up EV charging stations with Oil Marketing

companies like HPCL, IOCL and is working closely with

other key stakeholders in creating and promoting the

EV charging ecosystem in India. Further, over the past

year, Tata Power EV charging network’s presence was

established in Mumbai, Delhi, Hyderabad, Bengaluru,

Vishakhapatnam, Vijayawada and Lucknow under various

business models

Hi

Ola electric becomes a unicorn. I don’t know what do they exactly do or what operations do they run. As usual this valuation rise is because of Masa of Softbank.

EV market as per this news article will rise to $700 Mn by 2025.

Rgds

Please share views regarding which companies would benefit from the recent announcements in budget? In my view, e-bikes sector would benefit greatly from the 1.5 lac deduction. I am aware that Ujaas energy is launching e-bikes and would be benefitted. But the fundamentals doesn’t seem to be good. Any other companies in business of e-bikes?

Thought I’d share some of my latest musings with the usual accompanying data, all in the spirit of ‘Understanding EV Market’ globally.

June US EV sales and the Tesla revolution

In a country where pickup trucks and large SUV gas guzzlers are part of everyday culture, many Americans are struggling to accept or come to terms with the benefits of zero emission e-mobility. However, there are signs that the revolution is underway (starting with the sedan) and EV sales are going through the roof in the good ol’ USA, thanks largely to Tesla’s Model 3.

June EV sales in the US grew a staggering 51% YoY and +33% on the previous month. Tesla’s full battery electric vehicles (BEVs) commanded a whopping 68% share of all US EV sales, and the Model 3 continues its reign supreme as America’s No.1 selling Luxury vehicle and No.1 selling sedan, outpacing its similarly sized ICE rivals.

Tesla also created another record for itself during the June quarter, delivering close to 100,000 vehicles worldwide and smashing even the most bullish of analyst estimates.

By stark contrast, Nissan Motor’s US sales fell 15% in June and Toyota fell 3.5%.

These latest figures would have to be sending shockwaves through the hallways of traditional Automobile company Head offices, as they scramble to balance the need for profitability with the massive investment that is required to make the transition from traditional ICE vehicle manufacturing to full e-mobility. I believe that time is quickly running out for many of them in the sense that they will quickly lose relevance in a rapidly evolving industry, unless they look beyond their short-term profits to significantly bolster their investment and further accelerate their transition process.

Tesla’s Model 3 is making rival ICE’s and Hybrids look like relics of the past in almost every aspect with its zero emissions, performance, functionality, the ability to continually improve itself via over the air software updates and most importantly safety. Btw the Model 3 just received a 5-star rating from Euro NCAP, but the good news didn’t stop there as it also received the best score in Euro NCAP history!!

https://cleantechnica.com/2019/07/0…e-highest-overall-euro-ncap-score-ever-given/

The Big Hybrid Myth

Despite some analyst’s and several major car companies still trying to convince the public that Hybrids are a big part of the EV landscape as they supposedly represent the best of both worlds, the fact is that Hybrids unfortunately still require fossil fuels to power them and are all based on an old design that is centered around an ICE engine with the usual countless moving parts. This approach allows traditional car companies to use existing platforms (eg. Toyota Camry Hybrid), thereby reducing costs.

However, traditional ICE designs lack the pure performance of pure BEV designs and require significant ongoing maintenance compared to the groundbreaking and relatively simple full electric platforms. Therefore, some of the major car companies including Toyota, BMW and Honda are on course to mimic the fortunes of Kodak if they continue to downplay the rise of pure e-mobility (BEVs) and continue to focus on their Hybrid technologies, as hardly anyone is going to want them within a few short years.

As the charging infrastructure for BEVs rapidly expands, battery costs continue to fall and BEVs continue to increase their range, then there will be no need for Hybrid technology in the years to come (particularly in the PV space). Furthermore, you don’t see many Tesla owners complaining about ‘range anxiety’, so one could reasonably argue that we are pretty close to that point today.

Current statistics confirm this trend and the following 2019 stats for Passenger Electric Vehicles (PEVs) all point towards the eventual demise of PHEVs (Hybrids).

In Germany, sales for PEVs grew 65% YoY in May . In 2019, BEVs overtook PHEVs in terms of unit sales for the first time in history. The growth rate for German BEVs in May was a staggering 100% compared to PHEVs at 33%. PEVs represented 2.4% market share in Germany in May, and of that BEV’s accounted for 1.4% and PHEVs represented the remaining 1.0%.

In China, the story is even more convincing. Sales for PEVs for Jan-May 2019 stood at 426,000 units, a +51% YoY growth rate. BEVs represent over three quarters of PEV sales at 325,000 units (+56.4% YoY growth). PHEVs accounted for less than a quarter of all PEV sales at 101,000 units (+35.8% YoY).

However, in May 96,000 PEVs were sold and of these 75,000 were BEVs (+17% MoM) and only 21,000 were Hybrids (-19% MoM) i.e. Hybrid sales actually declined by almost 20% in May whilst BEVs continued their rapid growth story.

In the UK, well this article says it all IMO

https://www.businessgreen.com/bg/ne…plug-in-hybrids-suffer-in-sluggish-car-market

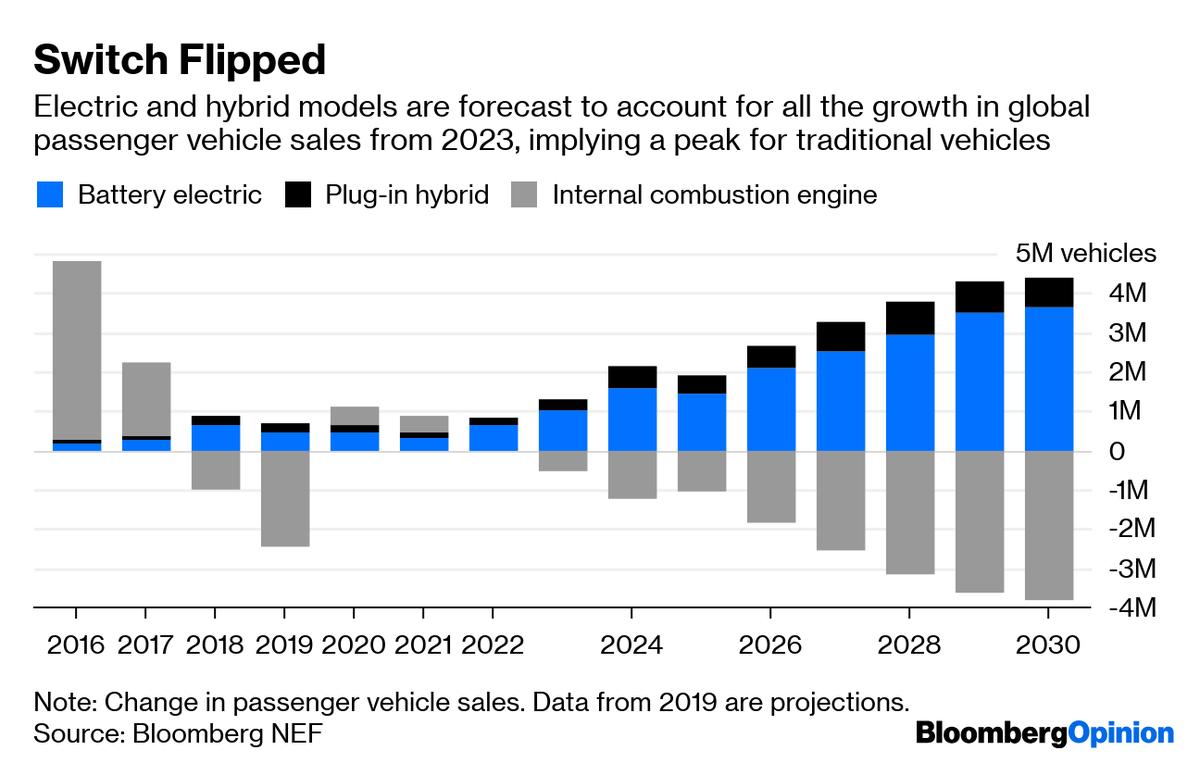

Looking beyond 2019, below is a forecast for BEVs vs Hybrids vs ICE vehicles. Note the expected virtual phase-out of Hybrids by 2022 as EV battery costs continue to decline with improved technology and a major increase in production (scale), batteries become more powerful and efficient and people realise that BEVs are not only far superior in terms of performance, maintenance etc, but they also have zero emissions meaning the added environmental benefits as they turn their back on vehicles powered by fossil fuels.

The China EV revolution, Latest Battery Trends and Global EV Expectations by 2025

China - May update:

New EV sales (NEVs) in China were @104,000 units in May and accounted for a record 6.6% of all PEV sales. Impressively the market share for NEVs in China continues to grow in an environment where government subsidies for shorter range EVs have been abolished. What’s even more impressive is that as of May 31st, the total number of EV chargers in China stood at 976,000 (+71% YoY).

EV Battery production for May also grew at an impressive rate, and NCM/NCA batteries that typically use Lithium Hydroxide continue to be the preferred shoice of Lithium Batteries for EVs. This bodes well for current and future suppliers of Tier 1 Battery quality spodumene.

China May EV battery production at 9.9 GWh (+35.6% MoM).

NCM/NCA type at 6.5Wh (+49.5% MoM)

LFP type at 2.3 GWh (-16.9% MoM)

LMO type at 1.1GWh (+456% MoM)

Jan-May 2019 EV Battery production at 37 GWh.

NCM/NCA at 22.9 GWh (62% share).

LFP at 12.2 GWh (33% share)

LMO at 1.8 GWh (5% share)

China - June update:

(note that only some of the June figures have been reported - still awaiting official total sales from my source):

Total NEV production at 129k units (+95% YoY)

Total EV battery installed capacity at 6.61 GWh (+131% YoY)

Battery capacity is growing faster than unit sales due to the average EV battery size for June 2019 increasing to 51.24 KWh (up from 43.30 KWh YoY)

From the latest data sets and reports it is clear that China is going full electric and earlier this week the Chairman of CATL said (at the World New Energy Vehicle Conference) that the electrification rate of China vehicles will reach over 70% in 2025. That forecast implies over 20 million EVs for China alone in 2025 i.e. based on the current annual unit volume of their domestic Auto industry.

If China continues to account for roughly half of the world’s EVs, then CATL’s statement suggests that @40m will be sold annually by 2025. However, I’d expect other populous territories including South East Asia, India, Europe, South America and North America to significantly increase their EV sales and market share by 2025 (due to a wide range of models being available and lower costs achieved through mass production), and therefore I’d expect China’s share of annual worldwide EV sales to fall slightly to @30-35% by that time. If that’s the case, then the rest of the world should be selling somewhere @35-40 million EVs in 2025, meaning annual global sales of @55-60 million EVs. This figure is broadly in line with Tony Seba’s central s-curve forecast (typical adoption rate of new technology – see below graph) and thus CATL’s forecast looks to be more plausible than what most mainstream analysts are forecasting, or should I say under-forecasting (more on that subject below).

Wright’s law (under the assumptions of Ark Invest) also support CATL’s bullish prediction and the above s-curve graph. Here’s what they recently to say:

‘The rapid growth of the EV market has caught many analysts flat footed. Four years ago, the Energy Industry Administration (EIA) among other forecasting agencies estimated that EV sales would total a few hundred thousand units in the early 2020s. After they hit 1.45 million units in 2018, the same agencies now forecast that EV sales will increase to roughly 4-4.5 million in 2023, suggesting that their growth will decelerate from 79% last year to 25% at an annual rate during the next five years. Based on Wright’s Law, ARK’s forecast for EV sales in 2023 is 26 million units, roughly six-fold higher than the consensus estimate, with growth compounding at a 78% annual rate.’

Battery Chemicals Demand Outlook - If 55-60 million EVs are sold annually and approx. 50,000 tonnes of LCE (Lithium Carbonate) is required for every 1 million units, then the world is going to require approx. 2.75 - 3 mt of LCE for 2025 alone. That’s a massive 10-fold increase in LCE supply from 2018.

Current EV sales forecasts from mainstream analysts are too conservative

It doesn’t take much research to reveal that the majority of mainstream analysts, including those representing the likes of Bloomberg, UBS, JP Morgan, Morgan Stanley, Cannacord etc. are all providing forecasts which are far too conservative IMHO. And for them there is good reason for their apparent incompetence (mainly to do with their bonus structures and under promising / over delivering to ensure minimal risk to themselves and their clients).

However it is known that the vast majority of mainstream estimates in past years have consistently underestimated actual demand, and therefore I see absolutely no reason to trust / believe their forecasts moving forward.

Some of the industry heavyweights (eg. Tesla, CATL, VW etc.) are also worth listening to as it is their business to understand and react to current and future trends of their products. However, I am also wary of large companies that are slow to react to massive change.

Summary

The latest data comprehensively points towards a rapid acceleration in electrification rates IMO - meaning that the age of e-mobility is upon us already and will become the dominant form of new transportation by 2025.

Simon Moores from Benchmark Minerals tweeted last Friday that ‘We are no at 91 lithium ion battery megafactories in the pipeline to 2028’ . Folks, this is massive news as this no. has already blown out from the 74 announced earlier in the year. That means that Megafactory capacity is nearing the 2000 GWh threshold (see graph below), which based on current trends will be easily broken by the end of the year.

However, expect 2000Gwh to increase to 3000Gwh, and the 2000GWh no. to be brought forward to 2023-2025 (aka the graph below) as the Megafactory pipeline continues to rapidly expand.