Hi @Rezang_La. Broadly i agree with your methodology for valuation, although I would assign higher multiples for the ARC business which yields a higher RoA over the NBFC.

However there is one risk which I find difficult to factor in the valuation. The listed company - Edelweiss Financial Services Limited is the Holding company for all its individual special purpose subsidiaries. There is a good change that the subsidiaries would list separately due to Investors Exit, Regulations of IRDA, SEBI, RBI etc. In that case it could be that the holding company would be valued at a significant discount to the underlying value that you are calculating.

I feel that risk also must be factored in the value you have arrived at by applying appropriate discount %.

Last time I checked, this is a forum and not a homework assignment

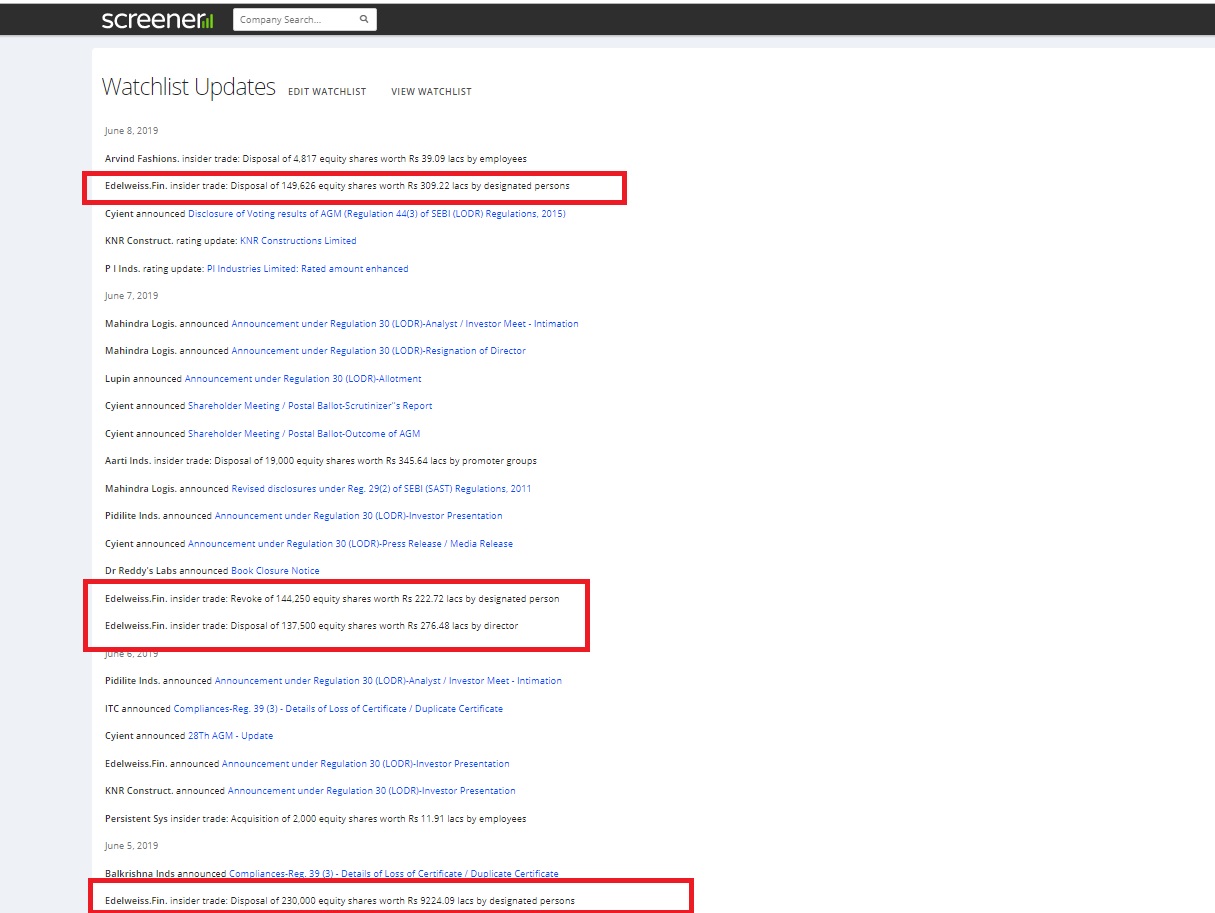

But I have no other data, hence the question in the forum. Lately the stock has been plummeting that coupled with insiders and promoters selling in hoards doesn’t seems a good sign especially with DHFL on their knees. It’s no secret that edelweiss has a huge exposure to real estate segment, so I am trying to find out any information I can

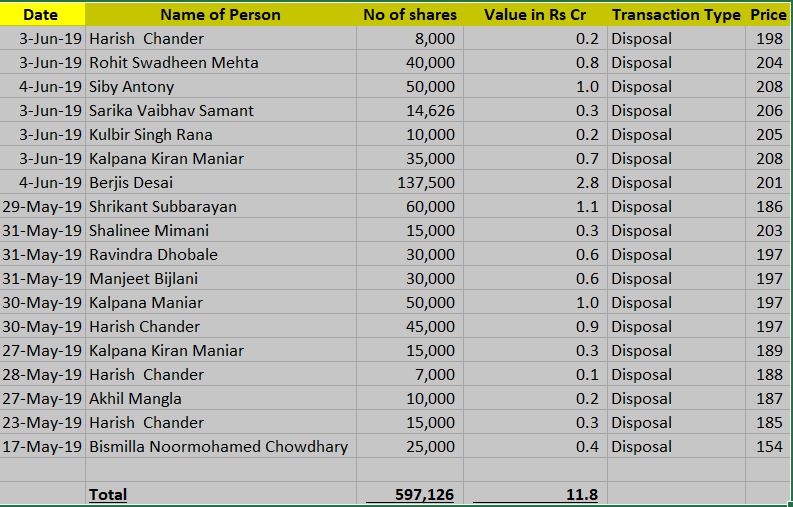

Here is the data collated from BSE…lots of selling between Rs. 195-210 by key employees…its like they know that the stock wont cross or sustain above 200

Hi All,

Need clarification on the below queries.

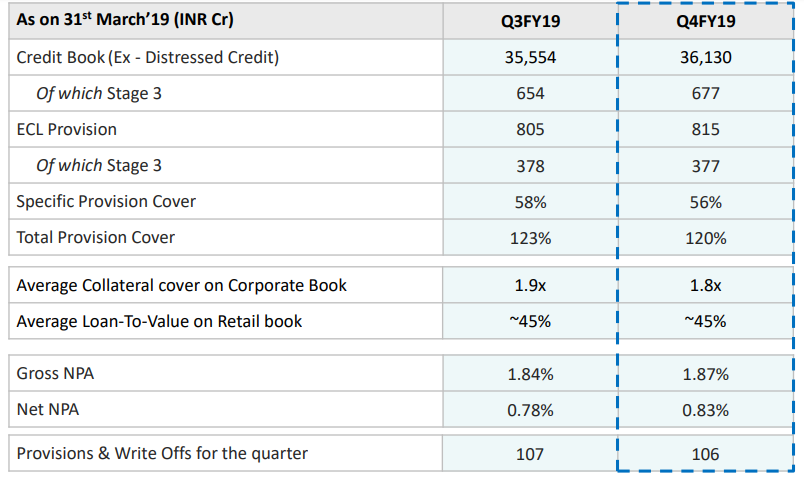

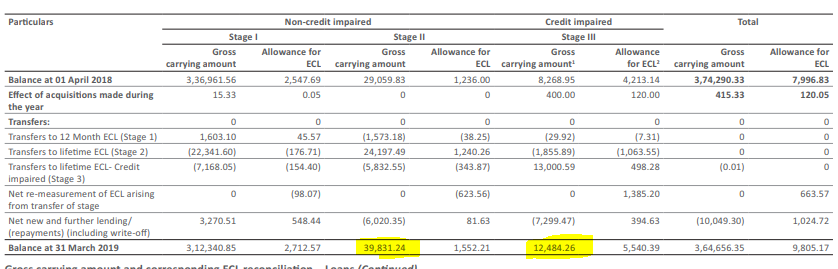

In the Investor Presentation , They have presented that their NPA is 677 Cr of 36130 Cr Loan book which is 1.87 % NPA ( Screen Shot 1 ) . However in the Annual Report they have declared the Stage 1 , 2 ,3 numbers as per below and the Gross Carrying amount is marked as 1248.4 Cr. And Allowance for ECL is marked as 554 Cr.

) Is Gross NPA same as that of Gross Carrying Amount ? If not can you please explain what it is ?

)Is Allowance for ECL similar to provision ? If it is similar then there is a difference between the numbers presented in the presentation and Annual report and looks like I am missing something here. Any help on these 2 clarifications should be much helpful.

Hi @vignesh@deeps2884 - just to clarify - this is new accounting norms arising from IND AS implementation, not RBI. Under IND AS, loan books have to be carried at fair value and income from them is recorded on an IRR basis instead of fees + interest being recorded separately as was the case earlier. Further, earlier norms required income on NPA assets to be recognized on a realized basis, whereas under IND AS, lenders have to calculate the expected credit loss over a 12 month period and over the lifetime of the loan asset, and account for it as expected credit loss - ECL. The rationale is that NPA norms only trigger when an asset is recognized to be impaired, whereas the book and income should be adjusted periodically for the expected future credit loss. Stage 1 is therefore ECL for first 12 months, Stage 2 is ECL over the lifetime of the loan asset but where the loan asset is not recognized to be impaired, and Stage 3 is ECL over lifetime on the non-provisioned amount of the loan where the loan asset is recognized to be impaired. This is arising from IND AS solely, and this will I think replace RBI’s accounting rules on the matter. This brief by EY has an overview: https://www.ey.com/Publication/vwLUAssets/ey-step-up-to-as-ind-for-banks-and-nbfcs/$FILE/ey-step-up-to-as-ind-for-banks-and-nbfcs.pdf

What @deeps2884 is referring to I think is SMA 0 SMA 1 SMA 2 loan status, which is RBI’s classification scheme for impaired assets prior to reaching NPA status and different from the above - these are called special mention accounts and are triggered at 0, 30, 60 thresholds, and post which they become NPAs - there are also qualitative criteria to be monitored. SMA is primarily for monitoring purposes, as lenders are supposed to report SMA status of borrowers once they trigger the criterion.

@vignesh the reconciliation is not possible because they are different accounting forms - the ECL stage 1 is the expected loss on non-impaired portfolio in 12 months, ECL stage 2 is expected loss over the lifetime of the non-impaired loan book while ECL 3 is the expected loss over the lifetime of the impaired loan book after netting off provisions. Gross carrying amount is I think essentially the PV / Fair value of the loan / earning asset book, so is not the same as GNPA. NPA provisioning norms are set out by RBI which kicks in when impairment is recognized, ECL is an accounting standard which applies for the total loan book which adjusts for expected impairment. Stage 3 gross carrying amount and ECL calculation is based on internal policies and models - i.e. credit impaired is not necessarily the same as NPA and ECL is not the same as provisions. I am not an expert on accounting but I think this example captures the idea - please correct me if wrong: Suppose you have lent Rs. 100 for 2 years at 10% interest, and the loan paid back equally over both years. There is a 5% chance the borrower will default in Year 1 and 7% chance they will default in year 2 - then the ECL Stage 1 is basically 5 and ECL Stage 2 is basically 5%*(-100)+95%7%(-50)= 8.325. In Year 2, Stage 1 is 7%*50 - 3.5. Acc to IND AS, you would in year 1, adjust the ECL stage 1 from the loan’s income and calculate the IRR income to be amortized basis that. Subsequently, if the loan continues in good standing, ECL Stage 1 will be applied for 12 months for whatever portion of the loan remains on the book - if the risk increases, ECL Stage 2 will be applied instead and post recognition of impairment, ECL Stage 3.The impact is basically on recognition of interest and fee income on loan portfolio, which is now on a life time IRR / FV basis and adjusted for expected losses and tweaked according to performance.

I think, the market is getting spooked. Any plans to sell anything is nowadays is seen negatively. During earlier times, market used to get excited at prospects of a windfall gain that could be passed on to the minority shareholders. Now, the chances of a single dime coming as a special dividend etc seems extremely unlikely. Moreover, companies like Edelweiss need the money now for meeting certain obligations.

Please read the conference call transcript of last quarter. U will have answers. Company is planning to split into 3 separate divisions and for each division company will bring a strategic investor. For credit already they have CDPQ. For insurance they have IFFCO Tokyo and for wealth they are bringing in a new investor. Each vertical will have a sepera5e board / governance structure. More details in conference call transcript. Pls read