Wasn’t the point of buying Edelweiss as a consolidated entity to get an all-weather compounder? Why split and create 3 cyclical businesses?

They are not going to split into 3 business. Please look into the investor presentation outlook 2020 - 2022 . You will have more details.

Are you not being too generous by calling this company an all weather compounder? It has given no return to investors in the last 12 years

My two cents … Every business should be capable to fund its own growth …

Agreed that Insurance need need to break even so understandable but there is no reason to dilute stake in a asset light business of Wealth Management to fund possibly the distress in LENDING business.

Isn’t CDPQ fund enough ?..

i am disappointed in case JEWEL crown of the business is diluted …Rest what happens later is everybody’s guess …

1 Like

This article can perhaps help to understand the stake sale from a different perspective.

Disc- Not invested but closely following.

1 Like

CRISIL has reaffirmed the credit rating for company’s short term borrowing. In an environment where rating agencies are facing lot of heat, they must have done a thorough review before assigning the same. So gives confidence amongst the negative price action the stock is seeig4e40788b-1d11-4d3b-baf3-68da625d3169.pdf (125.4 KB)

1 Like

I think the right way to see the company is the growth in revenues and profits. Stock Price is not in the hand of the company (market behaves irrationally - price in 2008 was out of whac and price in 2019 has also considered too many negatives)

If you look at the 10 year growth for Edelweiss - it has very nicely grown at cagr of 15-20% and I expect it to grow in such a manner over the next 10 years.

Edelweiss management is being prudent by raising funds on balance sheet by selling stake in the Wealth Management business - as the undrawn Bank Funding lines can remain undrawn (banks may refuse to disburse if things become tighter). Further by raising equity in the wealth management business they are getting a floor on stock price.

I feel in the medium to long run - Edelweiss would be split into 3 companies like IIFL or they would get a bank license (either of the 2 would happen)

1 Like

Asset quality exposed to risks related to concentration in wholesale lending : Asset quality will remain vulnerable to the concentration risks inherent in the wholesale loan book, despite the strong focus on collateral. As on March 31, 2019, wholesale lending constituted almost 50% of the total loan portfolio (excluding distressed assets credit), with the 10 largest loans constituting 17% of the wholesale portfolio.

Also, around 60% of the wholesale portfolio comprises real estate loans; this segment is vulnerable to cyclical downturns

Lower profitability than peers : Profitability ratios are lower than those of other large financial sector groups; return on assets (annualised) was 1.7% and return on equity (annualised) 13.3% for the fiscal 2019

Furthermore, the life and general insurance businesses continue to be loss-making. The general insurance business was started in February 2018, after requisite approvals were received from the Insurance Regulatory and Development Authority of India. This business is also expected to affect consolidated profitability in the initial years of operations, given its long gestation period.

(source: CRISIL)

1 Like

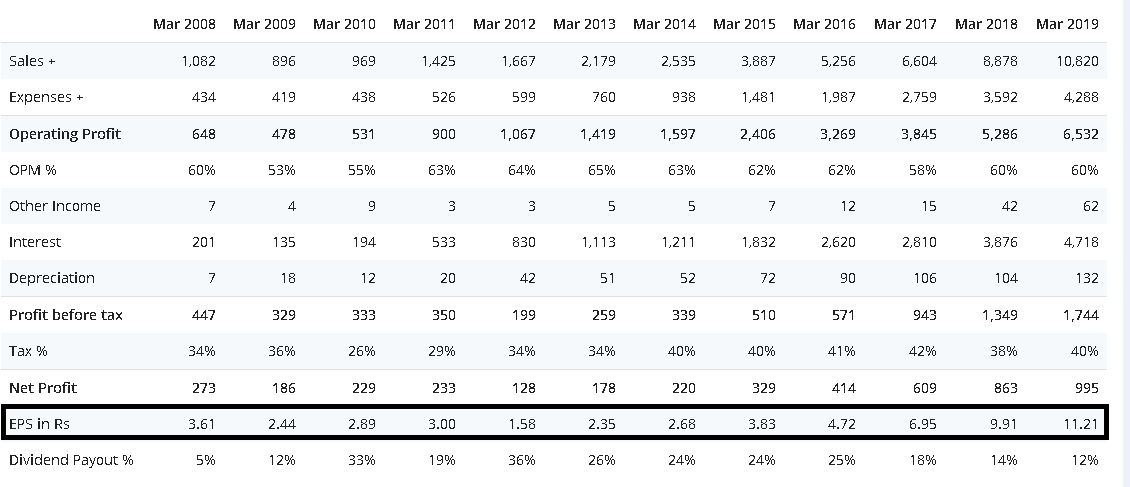

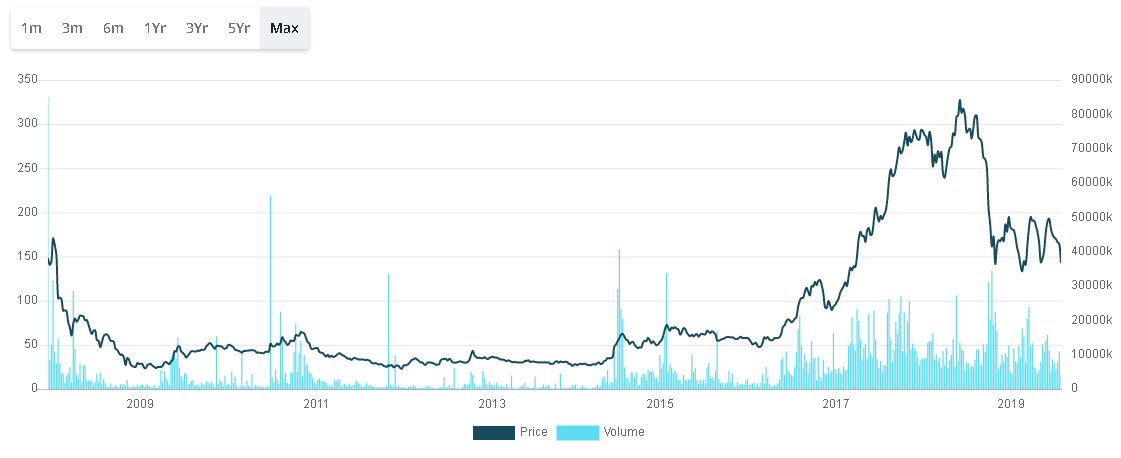

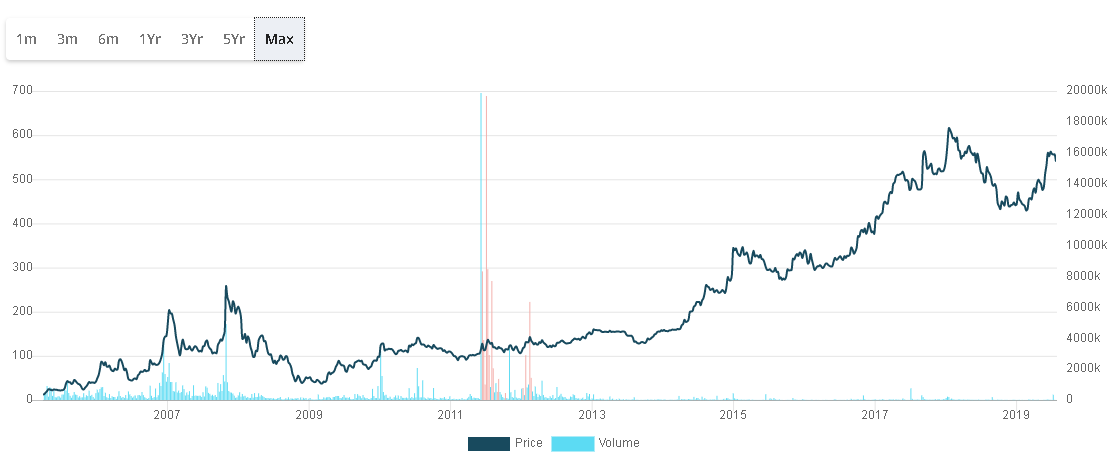

12 years back stock was at Rs150. EPS then was 3.61 in FY18. That is a P/E of 41.5x.,

Even now stock is closer to Rs150. EPS in FY19 was 11.21. That is a P/E of 13.3x

41.5x → 13.3x is massive P/E derating. Data for the same here from screener

1 Like

Interestingly the Sales Growth is 10 times but the EP growth is ~4 times. The earnings growth has been compensated by PE de-rating.

At this low PE we are getting steady compounder but the current downtrend shows it might get dragged to single digit PE level.

if you start comparing prices in 2008 and deduce that the company is a investment opportunity (i don’t know what to say).

2008 was an year of excess - even stock markets had breached 20k (so even the stock market was down or flat for ~5 years). People who bought a 50x stock should be questioned not those who are investing in 15x stock.

Edelweiss would be 10x of the current size in the next 10 years (if we believe in that we can buy the stock which is available at descent valuations).

2 Likes

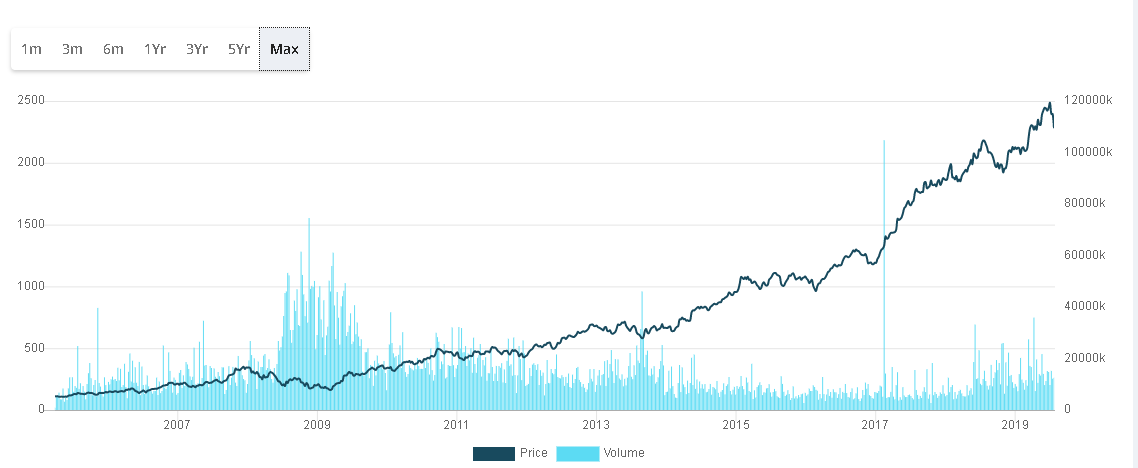

It is not like every company you invested in 2007 or 2008 has not given any returns like Edel.

For example see HDFC Bank below

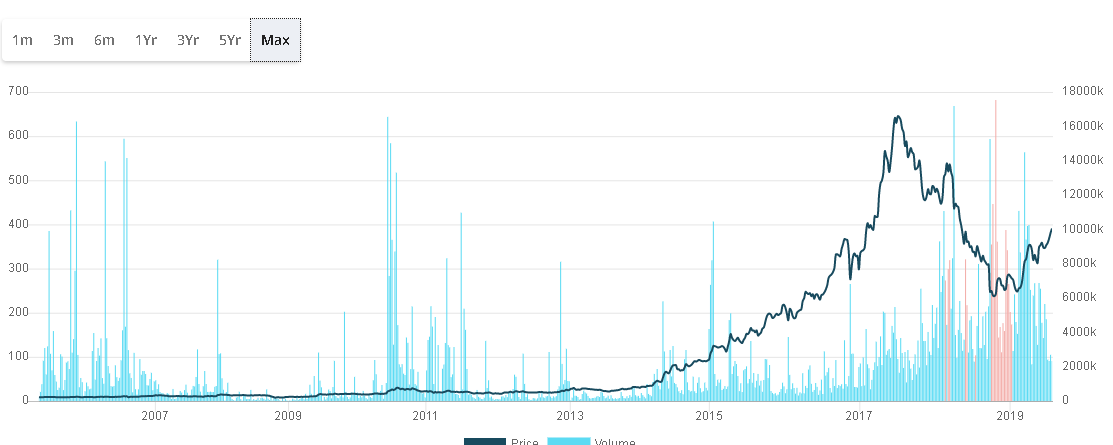

See Can Fin Homes

See NESCO

All I am saying is businesses like Edelweiss and Motilal Oswal are over hyped. At best they are trading stocks because a large part of their businesses are cyclical in nature. They are certainly not compounders.

Last but not the least even when you exaggerate one needs to be careful. 10x in 10 years is 26% CAGR for 10 years. You might want to check how many businesses in India have grown at that pace over 10 years and whether Edel works in such an industry where such growth is possible. Even the promoter Rashesh Shah would not have dreamt of such growth over the next 10 years in his wildest dreams.

3 Likes

This comparison discussion of Edelweiss in 2008/9 vs 2019 is a very interesting one, and got me curious. Given the stock price was about 160 then, and in the 140s now, I thought why not compare what the company and the business looked like then vs now.

-

Business Guiding Principles - 9 out of 12 principles exactly the same between 2009 and 2019, with 3 new ones added focusing on customers and stakeholders(Source : 2009 AR, 2019 AR)

-

Business segments (Source : 2009 AR, 2019 AR) :

- In 2009/10, active primarily in capital markets related business, and just starting off on insurance business

- In 2019, a well established player in the NBFC space, leader in Wealth management, leader in ARC, growing asset management space, and in a growing insurance business much more closer to profitability

-

Board of Directors - 6 out of 7 directors from 2009 remain on the board, with several new additions (Source : 2009 AR, 2019 AR)

-

Revenues of 1082 cr 2008 vs 10820 cr 2019 (Source : Screener)

-

Net Profit (cons) of 273 cr 2008 vs 995 cr 2019 (Source : Screener)

My request to everyone here is to please continue adding any interesting comparison points you see from then vs now.

7 Likes

Yes, it is a very interesting comparison. It may give an illusion of fair valuation. But the current valuation is not dependent on historical valuation. Just shows how irrational markets can be. If you compare Wipro’s marketcap revenue now versus the Dot com bubble, you will find similar observations.

1 Like

The valuation comparison interests me a lot less than a comparison of the business itself, what the promoters said vs. what they did, and other such perhaps more qualitative aspects.

1 Like

One of the interesting thing to note perhaps is that Edelweiss has managed to get funded by highly conservative investors, the Pension funds from abroad. It reflects the credibility Edelwiess has built for itself. Lending money is an easy part of an NBFC but raising funds for foreign endowment/pension funds requires to be best in league and trustable leadership.

6 Likes

I think Govt. is taking leap of faith in assuming that FPIs have institutional capability to buy distressed assets and resolve the same. What could happen is that small bankruptcies could be handled through this route. It could also allow promoters to get back their assets by routing funds through FPIs. In case of bigger and complex asset structures there are no alternative to ARCs. You could listen Rashesh Shah in the concalls where he said it is difficult biz to conduct in Indian circumstances and hence an entry barrier. In any case the opportunity size is big enough to accommodate everyone for the time being.

1 Like

kora management is investing 875 cr in edelweiss group in their advisory business. edelweiss also talks about listing the advisory business separately with a couple of years.

if we can understand at what valuation kora asset management is investing in the advisory business , that can be very helpful

Disc- Invested

1 Like

They are looking for a valuation between 8000 - 10000 by FY 21 as per mgmt. This was discussed management conference call.

1 Like