In which part did you find corporate governance issue in DBL like financial,result ,order book , working model etc. Can you please share with us so it will other to understand better.

1 Like

https://www.equitybulls.com/admin/news2006/news_det.asp?id=236837

COMPANY TO START NEW BUSINESS ACTIVITY (they say DBL will not run this as a business activity and will only act as a service provider?? What that mean??)

- To carry on the business of purchase and sale of petroleum and petroleum products

- To act as dealers in and distributors for petroleum companies

- To run service station for repair and servicing of automobiles and to manufacture or deal in fuel oils, cutting oils and greases

Discl-Invested

I believe Rohan Suryavamshi had mentioned in the recent interview that this agreement with IOCL was an one off thing.

The agreement though gives an impression that they are venturing into this business.

I don’t see any issue with it as companies do tend to do these kind of one off works to customers with whom they have long relationship with.

1 Like

You can only sepculate on the price action when the market keeps discounting good news like new order wins and early completion bonuses.

I believe market feels the liquidity squeeze in the system will affect the construction sector and projects will get stuck.

Also the market is severely punishing any stock which has uncertainty attached to it.

From valuation perspective,this stock is at attractive levels.However this is proper bear market for midcaps and smallcaps now,where no price is low price.

4 Likes

not sure if this has been discussed before, but can someone please explain the reason behind supernormal ROEs for Dilip? a few months ago remember a news regarding CBI raiding premises of the promoter. There are such huge corp. governance/political favor linked risks lurking in DBL and more so in many infra stocks…

another past article from 2012:

1 Like

The above news article is of 2012.

The above incident is the reason the market believes if BJP loses Madhya Pradesh elections,it will be trouble for Dilip Buildcon as its said to be close to MP CM.

The company has been questioned on this numerous times in the investor meets and their refutal has been that they are present and operate Pan India even in non BJP states and only 5% of the revenue comes from Madhya Pradesh and more than 90% of their order book is from Central govt.

Unfortunately in India ,there is always a political risk associated with road construction projects and may be L&T is the only exception.

Bet on Dilip Buildcon is on their execution capabilities based on the track record and comparitively decent balance sheet.

The stock is quoting at 10 times trailing earnings and 7 times forward earnings.

One has to look at it objectively and think whether the current price has accomodated the political risks(which is diffuclt to quantify).

In these times of fear,we also need to consider the opportunity size.India needs big infrastructure development in the coming years and the number of players who can execute these road construction projects are a few.

7 Likes

Additionally other thing is that company getting into unnecessary controversies… 2 Qtr back it was delay in publishing the Quarterly results which lead to rumor on auditor resigning and now it is changing the MoA for petroleum products which I do not find convincing at all. All these things dent the confidence in the company at a time when people want to be safe than sorry. With 75% promoter holding it is really hard to digest these actions as the drop in Mcap would be hurting them the most.

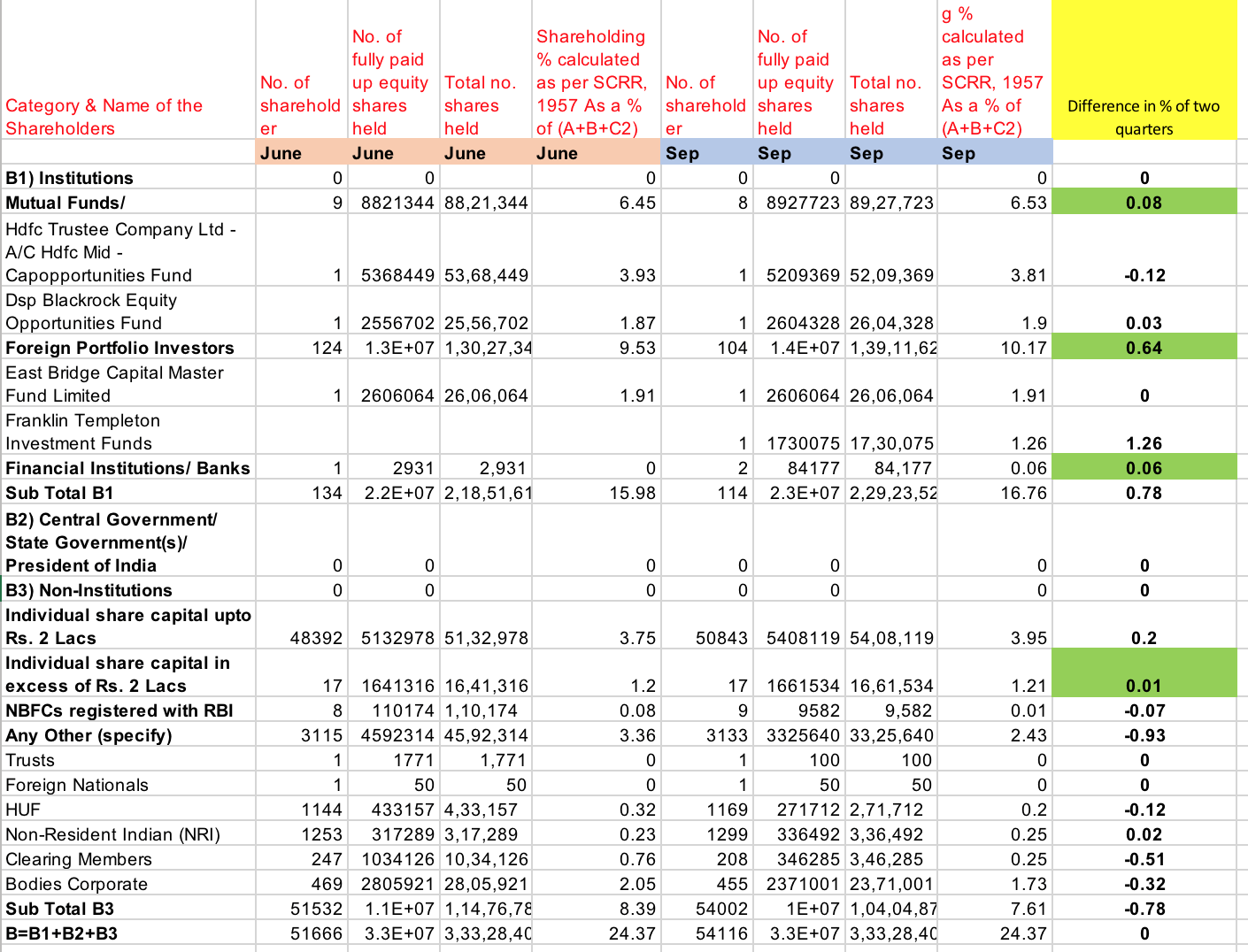

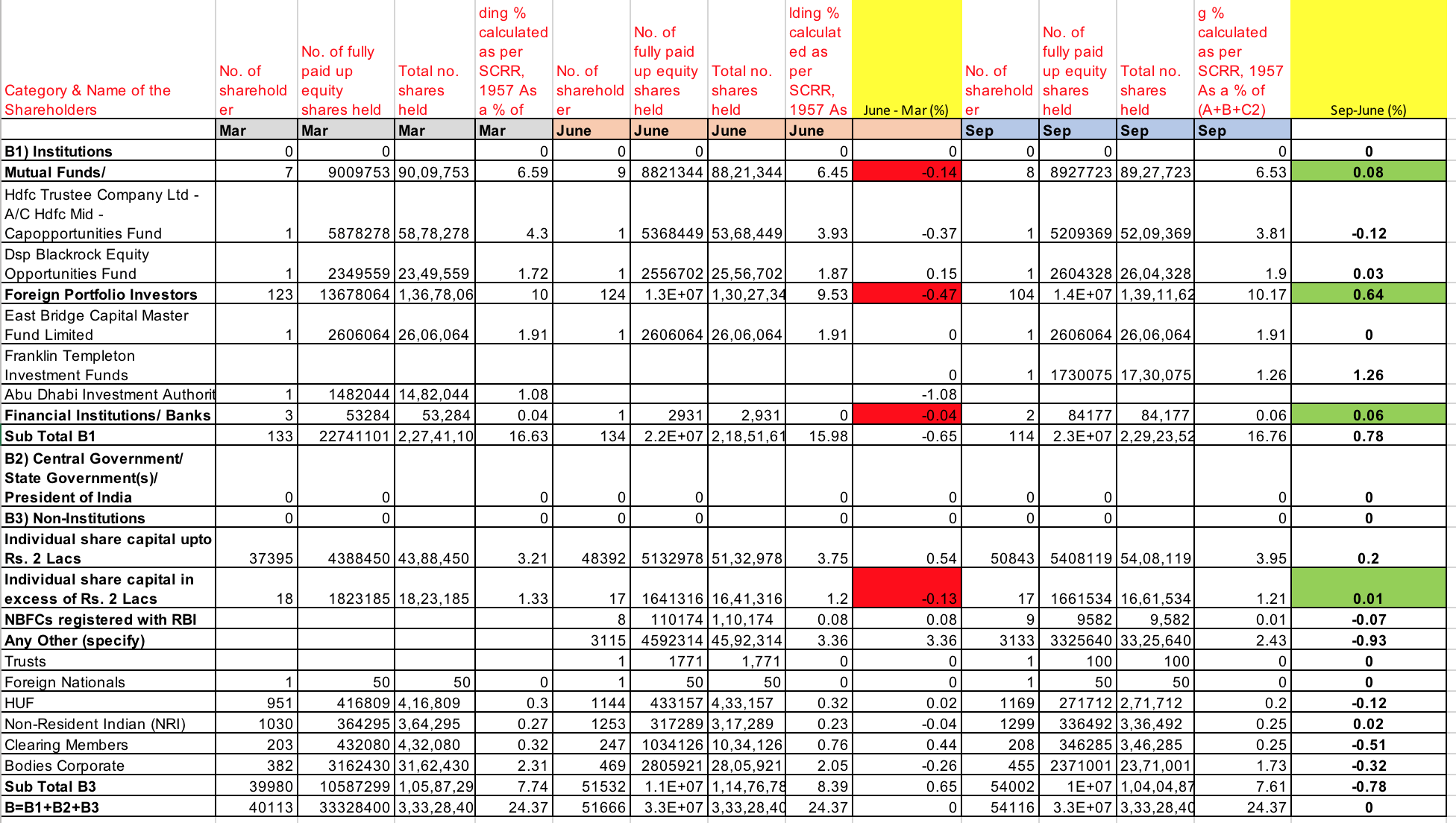

I was looking at the shareholding data for last and current quarter. I dont see major diff between MF holding , FPIs or for HNIs holding in excess of 2 lakh equity capital. Then whose selling triggered such a major correction in last quarter ?

EDIT : Comparing last 3 quarters too dont tell much

Disc : Not invested but tracking this scrip as I have other Infra sector investments

@Old-timers: Is the fact that there is no churn from Institutions and FPIs a contra indicator or they also, like rating agencies, are often slow to react? MFs I can understand won’t change views too quickly.

1 Like

One cannot infer from aggregate data what could have happened. Institutions could have sold and other institutions bought at much lower prices.

5 Likes

Got “Fastest Growing Construction company Award” and “India Top Challenger Award 2018”

1 Like

Attended the concall yesterday evening.

The Q2 revenue was way below expectations but the company maintains that H1:H2 has always been 40:60 mix due to monsoon and the management maintained its guidance for 10000 crore topline for FY19, EBITDA 17-18% and debt at March End lower than Mar 2017.

It’s a bit hazy but I seem to recollect that an I-Banker had posted here saying that DBL hsa achieved FC for HAM projects at 18% recently (somehow cannot find my post and his post) ; glad that one analyst asked the rates and the answer was that DBL and other top players are achieving closure at below 10% interest rate; the banks are PSBs and a few private sector ones; the list to be disclosed after closure of remaining one HAM project.

1 Like

Note from Conference Call Yesterday:

-

Received many awards.

-

Received financial closure for 8 HAM projects and 3 more projects will be completed in this month.

-

1 more HAM project is in the final stage of Financial closure.

-

Stressed on Half Yearly results more than Quarterly Results.

-

Reduced finance cost to 5.8% from 6.2%

-

Net Debt at 1.24 = 1.24 Working Capital Debt + Equipment Debt

-

Hope to reduce the DEBT to ~1

-

Working Capital Debt to Equity is at 0.7

-

Guidance at 10K Revenue

-

Revenue Breakup - 40-60.

-

Focus on winning Projects.

-

Diversify the order book.

-

Do not see the Debt increasing.

-

Expecting to win another 4-6K Crores projects.

-

Experiencing Unique Year.

-

HDFC Securities Q&A:

-

Any BONUS in Quarter? No

-

Cumulative Bonus? Similar line as past 100 Crores

-

Why Debt gone up by 300 CRs? Investing in all our sites, once we have the Appointment Dates we would get 2000 Crores hence we are seeing the number going up.

-

Would get 10% mobilization Advance.

-

400-500 Crores have been deployed even before mobilization advance has come.

-

All the preparation is going in at the same time and without mobilization advance we are seeing debt and inventories going up.

-

1000 Crores from new HAM projects in this year.

-

1 projects has delayed by 1 quarter and 2 projects were preponed hence the shrem deal is extended to Q1 FY20

-

Will never get into Oil Service Business. Only doing this as a one time investment that too done by IOCL since it is the biggest client.

-

DBL is given the chance to build the Oil bunk.

-

160 Crores has come from Shrem. When the actual shares are actually transferred then only Profit or Loss from the Shrem Deal is shown in P&L.

-

What is the growth of FY20? Too early to give out numbers, will focus on improving Debt to Equity, Cashflow Generation etc. Would discuss at the end of this Year.

-

What is the extra Tax item present in P&L? Why have you provided for 12.77 Crores in this Quarter? Tax is already paid on September 2017 and we are mentioning that this amount would come this year.

-

What is down side risk of guidance not being met? The projects are checked every day and there is no reason to worry about the guidance.

-

How is 160 Crores booked in Balance Sheet? They are part of non-current liabilities. Would be transferred once we book the P&L.

-

DOLAT Capital Q&A:

-

Earlier given 25% guidance but now we are pushing to end of Year. Why so? We will for sure do 15% on Topline but would give actual guidance once we get the financial closure.

-

By 15th December we would get financial Closure for all.

-

Appoint data by December 4 projects would be started, 4 in Jan, rest in Feb, March or April.

-

Total Capex would be around 500 crores.

-

JM Financial Q&A:

-

Did we miss any HAM project within Stipulated time? No, it is the government delays also.

-

EPC projects would have 90% lands and HAM projects would have 80%

-

In December we are going to see Appointment Dates for:

-

Anandapuram

-

Karnataka

-

Odisha

-

Madhya Pradesh

-

Interest rates at which we are getting the HAM projects? Below 10%, almost all are funded by Banks

-

How has been the response from Banks about project funding? Challenges are there but not for good players.

-

ICICI Bank Q&A:

-

Reason for Share Pledge at 17% why? Same as last quarter. Given to get only for the bank guarantees, no fund based borrowing. Should come down in the next Quarter.

-

Debt level will be targeted to 2800 Crores, how much is the mobilization advance? 2000 Crores is total very small has come, if all has come we would reduce.

-

320 from Shrem Deal and 2000 from mobilization advance.

-

What is affective Tax rate? 25%+

-

Will it be back loaded to entire second half? Yes

-

Why? Due to the reduction of ATIA sites, the number of sites got reduced and new projects would get the tax. We have MAT credit of 400+ Crores to cover this up.

-

How are managing receivables? That was in the last type of contractors, there is no Arbitration or Fights with Government so no issue with receivables.

-

Edelweiss:

-

Loss in momentum is due to? Is it only linked due to monsoon momentum, and it is different for different regions and we expected so and results are the same.

-

We would like to maintain 2 - 2.5 times of current revenues

-

Same line of raw material costs would be.

-

Progress is at very high level but cannot give the breakup.

-

What are the banks that are lending to you and industry? Mostly PSU and few Private Banks once we are done with the closures then we would discuss.

-

35 Crores provisioning.

-

New Projects coming in and existing debt would reduce both with balance each other based on mobilization.

-

2.5 K Crores would be the approximate debt level.

-

Outstanding balance on 2 accounts is around 200 Crores.

-

Why are we assuming lower order book if we have more opportunity? We are just maintaining our guidance and order book winning is based on how much we can do.

-

Number of acceptances from Balance Sheet for First Half: 850 Crores.

3 Likes

Found them being soft on growth projections on the call but couldn’t understand why…

Disclosure: Invested

Yes, that is correct. I too feel the same there are some states where they have very low or no activity at all so they bid more and use the existing equipment.

But they wanted to maintain the book at 2.5 times current years revenue. So that they can stabilize their Balance Sheet. I have read that somewhere on this thread we were discussing that they are going very fast which will increase debt. I feel they have to manage both given the issue with ILFS the confidence that banks have and banks’ NPA issues. If they aggressively get more HAMs and not able to find financial closure then it is both a dent on their share price and reputation as well. I think they can’t afford that any more. Given their shareholding percentage and the price fall.

They also mentioned that they will for sure make 10-15% growth but exact numbers would be available by next quarter because they would get the appointment dates.

But trusting their execution capabilities and their precision in calculating into the future revenue. I hope they would balance both bidding and execution and deliver us what they promise. I feel this counter is a 20%+ growth till 2020. Lets see how their guidance is next quarter. Lot of their money is in this company hope they disappoint themselves.

Agree with you. One think that was also clear from the call is that they are not facing any issues in getting financial closure for their current projects, which was a market concern… That probably is the reason the share price shot up 10% today even on an otherwise poor quarterly result.

Disclosure: Invested

HDFC Securities gave a buy call with Target of 817 but cutting from 1217 cautiously reducing the valuation to 13.5 (25% discount to valuation given to other peers, which is 18%) instead of 16.5 earlier. I expect the same to continue from other brokerages as well but compared to the CMP they are very high. But if DBL delivers on what they mentioned in the call then there would be a rerating from Brokerages also.

Stock up 2.5%. Think we will get real-time updates on the exit polls over the next 10 days along with DBLs movement!!

Disc: Invested.

2 Likes

Well, BJP is making a clean sweep in MP and Chattisgarh as per some reliable election experts. We can discuss this in 10 more days. BTW, DBL’s revenue share from MP has gone down materially so not a great source of worry as such