Agree on the revenue share. But DBL + other EPCs never went down for fundamentals. Purely sentiments + midcap massacre. Any clear win for BJP in MP will help sentiments part.

Ratings update: http://www.careratings.com/upload/CompanyFiles/PR/Dilip%20Buildcon%20Limited-12-12-2018.pdf

main issues are rise in debt, increasing capital intensity compared to peers due to ownership of sizable equipment fleet, tense lending environment

Long-term rating downgraded to ‘CRISIL A/Stable’ ; short-term rating reaffirmed

near full utilisation of bank limits, no mobilization advance for the projects leading to high working capital requirement

Does anyone think this rating downgrade will impact DBL in long run? I think full utilization of bank limit might be for short term until DBL get advance from NHAI. Thoughts?

Good results posted by Dilip Buildcon for Q3 FY19

- Revenue increased by 28% as comparative to Q3 FY18

- EBITDA increased by 27%

- Profit after tax increased by 26%

Overall results are good. Only concern is 25% pledging made by shareholders. Did anyone know more detail about it?

1 Like

They have mentioned in the latest investor presentation that

Shares Pledged against Fund based facilities 85,05,000 8.22%

Shares Pledged against Non-fund based facilities 1,77,54,720 17.16%

They had earlier pledged less than 10% of their shares as a collateral but as stock prices started falling,they had pledge more to maintain the margin.Promoters hold 75% in the company and i believe it would get reduced as the stock price goes up.

Thanks. I didn’t realize that pledge % is increased due to fall in market price. Still learning about these things. I am not sure why stock price is going down and stock is in 6 PE considering DBL has good order book and ROE/ROCE of >20%. Only risk I am seeing with DBL is their association with BJP govt and pledging. Not sure if govt changes(if it happens), will it impact DBL? Budget for Pradhan Mantri Gram Sadak Yojana has been increased from 15,500 cr to 19,000 cr. So I hope DBL will get more projects in upcoming months and their order book will keep growing. Anyone see any other risk with DBL which I am missing above?

Disc- invested

Market is valuing all road stocks pretty badly… It feels the elections are a big political risk. Also the road construction businesses are at best,medium quality businesses as lot of things are dependent on factors outside its control (interest rates, longevity of order book, land acquisition issues,political bias etc)… In my opinion companies which manage the things which are in its control (pace of execution, debt, prudent bidding) will do well as India needs road infrastructure and there are few companies who have the balance sheet to do it across India.

1 Like

May be the market has priced in the possibility of non BJP coalition government. But considering the latest developments related to Balakot air attack and mood of people, the chances of BJP has only increased.

At this valuation of 8 pe, I am tempted to take a small but meaningful position here.

I have tried to do a SWOT analysis of the company in current situation. I would request other people to add to it or any other risk we are seeing for Dilip buildcon.

Description - Dilip Buildcon Limited(DBL) is a 30+ year old infrastructure based company mainly in road business with market cap of 9700 cr. Company is diversified in Roads, bridges, buildings, dams, canals, water supply & mining. It has presence in 17 states having 32,000 employees and 10000 equipments. Company has completed 90% of the project before time.

Story - I am betting on infrastructure need for next few years. DBL owns its equipment and doesn’t sub-contract. So it has good margin as comparative to other infrastructure companies.

Financials -

| Growth Trends: | 7Yr | 5Yr | 3Yr |

|---|---|---|---|

| Sales Growth | 51% | 32% | 43% |

| OPM | 20% | 20% | 19% |

| PAT Growth | 48% | 20% | 62% |

| ROE | 36% | 25% | 25% |

| ROCE | 17% | 14% | 13% |

Debt to Equity - 1.2

SWOT-

Strength-

- Own equipments and have no dependency on subcontracting

- 90% of the project are completed before time and company got early completion bonus.

- 5 year CAGR of 30+%

- Good order book of 23000 cr

Weakness-

- Company has dependency on govt for road contracts.

- High CAPEX requirement

- Negative free cash flow

- High debt

- Management impression - there were some news in past about criminal case against management

Opportunity-

- Govt need to improve infrastructure and hence need of road construction. Hence there are chances of getting more order in future

Threat-

- Company seems have connection with BJP government in MP in past. In case BJP doesn’t come into power, it might impact future contracts.

- High debt and promoter pledging is a concern

Price- Since cash flow is negative, it is difficult to find intrinsic value of the company.

Question - Could it become a good company like L&T in future? Does it have potential? What are the risk avoiding it to become good company? I am putting it under great company because it has dependency on govt to get project and will always have CAPEX requirement. Thoughts are welcome.

Conclusion - Business seems attractive at low PE(single digit). But it has risk of high CAPEX need and political connection

1 Like

DBL stock price is dependent on election results. After BJP’s loss in MP and other states it corrected significantly. It was available at 7-8 trailing PE about a month ago. Market had probably priced in the defeat of NDA in central elections as well. However, it became interesting after Balakot attack on Pakistan when environment changed in favor of NDA. I had taken a position during that time but now the stock has run up almost 50% in less than a month and it seems like NDAs win is priced in here. Any negative result from election can again result in severe correction. I have booked my profits now because now the positive is priced in and negative event would be a surprise.

1 Like

I think company is still available at attractive PE considering it is grower at rate of more than 30% per year. I was listening to one of interview from Rohan Suryavanshi and he mentioned the plan to reduce debt to <1 in next 2 years. Also he mentioned there will not be any CAPEX need next year. Not sure how much will be true. But I think market cap will increase if company reduce debt in next 1-2 years.

hello

when will the AGM

Stock has fallen significantly despite BJP winning with such a majority. Does anybody know if there is any material change in the fundamentals of the stock? The only news I found was the new Andhra government cancelling orders placed by the erstwhile TDP Govt. That does not seem significant given that DBL’s primary revenue comes from the central government.

1 Like

Are these below reasons market is worried about:

- HAM projects requirement for equity off a high debt?

- Tighter liquidity due to NBFC crisis for funding projects?

- Delay in Financial Closure and Appointment Dates?

- Last year’s auditor rumors have surfaced up due to new resignations in other stocks, also some say that there is a chance of more auditor resignations in future?

Update

DBCON announced that it has received LOA for a new EPC Project 'Construction Of Extra-Dosed Bridge Across Sharavathi Backwaters And Approaches Between Ambargodu And Kalasavalli Of NH-369E In The State Of Karnataka By The Ministry Of Road Transport & Highways, New Delhi

in addition to above i found interesting numbers

As on 30-06-2019, the company has a total of 136,769,768 shares outstanding and Current Price: 385.10 sales in TTM

Sept 2018 1623 Dec 2018 ( 2487) Mar 2019 (2571) Jun 2019 (2287)= TTM 896800000000 Aprox source: ( Dilip Buildcon Quarterly Results, Dilip Buildcon Financial Statement & Accounts)

Revenue / Share = Rs 655 TTM

March 15 to march 18 the net profit increased from 3.17%-> 5.46% → 6.84% ->7.32%

in the same period the Operating Profit Margin was 32.10%->25.39%->27.19%->18.28%

This represent the good operational efficiency by cutting the costs

another good point observed is the company is building it’s assets and moving from HAM to pure Road contractor pay In which the 100 % cost bear by government whereas in former the cost by the contractor is 60% .

The Debtor Days is improved from ( same period )167-> 80 → 66 → 64. The proactive in realising the MONEY is the BLOOD flow in organisation.

Disc: invested .This is not any recommendation to buy sell or hold , i am not any SEBI analyst Please do your own research and consult SEBI approved analyst

update

: Compnat beg new order at Construction of Kharkai Dam at Icha with all control gates and its allied works including civil, Mechanical (with Design of Gates), Electrical and SCADA System under SMP in the state of lharkhand.

source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/28a30fd6-7b07-4007-a724-bf800e880271.pdf

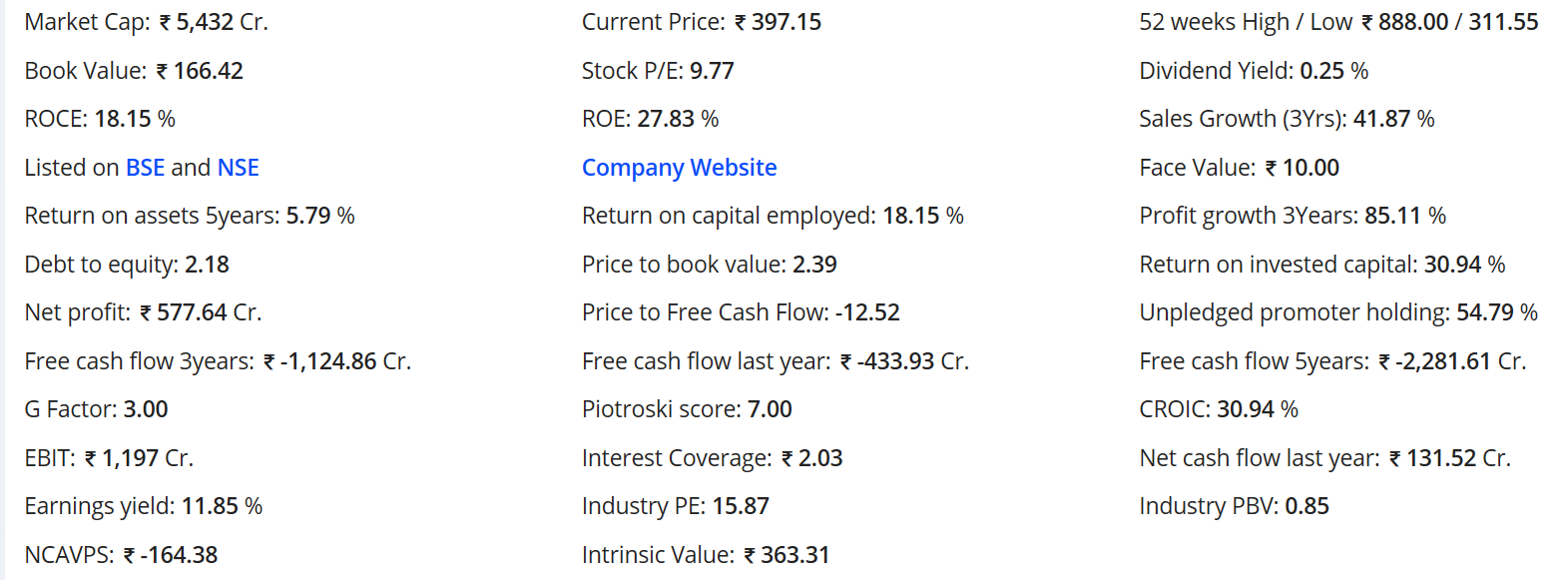

The Valuation seems to be good

1 Like

Hi, does anyone know if there is any news out on DBL. i was wondering if stock was down due to any bad news that we need to worry about or it is due to overall market sell.