If you check last 2 yrs AR they have added land bank recently, any information about exiting capacity utilization or expansion plan.

I saw in screener that tax % for the quarter has increased to 36.43%…

Does that mean the company hasn’t incorporated the tax cut benefit in the results?

Also, what could be the reason for higher tax % ? it was 26% in last years Sep quarter…

5 Likes

Hi Dinesh, @dineshssairam you mentioned you wrote to them regarding the cash position. Just want to check did you managed to get any response? Thank you!

No. Unfortunately, no response whatsoever. Maybe a few others can try their luck.

CS Email ID: info@dhpindia.com

CFO Email ID: ashok@dhpindia.com

It shows Rs. 1548442/- as “Reduction” in indebtness, however it is actually an addition. Maybe a clerical mistake or I am not understanding it properly.

Sent an email with the same query today. Let’s hope we get the response.

Following data is taken from Morningstar website.

| Parameter | 2017-09 | 2018-03 | 2018-09 | 2019-03 | 2019-09 |

|---|---|---|---|---|---|

| Cash and cash equivalents | 3663 | 8433 | 11222 | 3621 | 12052 |

| Short-term investments | 328339 | 332402 | 386210 | 427899 | 477525 |

| Total cash | 332002 | 340835 | 397432 | 431520 | 489577 |

| Short-term debt | 29486 | 29742 | 24448 | 31290 | 22942 |

| Long-term debt | 0 | 0 | 0 | 0 | 0 |

Numbers in INR thousands

MCAP at 230 = 689.85Mill

Value = MCAP - Total Cash = 689.85 - 489.577 = 200.27Mill

TTM Net Income is 99Mill

Hence stock is trading at PE of 2.

BSE India sought some clarification from DHP India regarding recent price movements.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=7222f7f6-d774-4867-aa5d-e8edaff7cca3

Not sure why so. This is the price movement since last 5 days

And this has been the case with most of the stocks out there recently. I am not able to understand why this clarification is required? Maybe someone can throw some light?

Exchange has sought this clarification from a lot of companies, i believe it is some automatic software trigger which someone in their software department forgot to switch off owing the global turmoil ![]()

5 Likes

DHP India Ltd.docx (176.3 KB)

Suggestions welcome!

This is only for educational purpose, not a recommendation.

3 Likes

Interesting co with solid fundamentals…

Also seems to be at reasonable valuations…

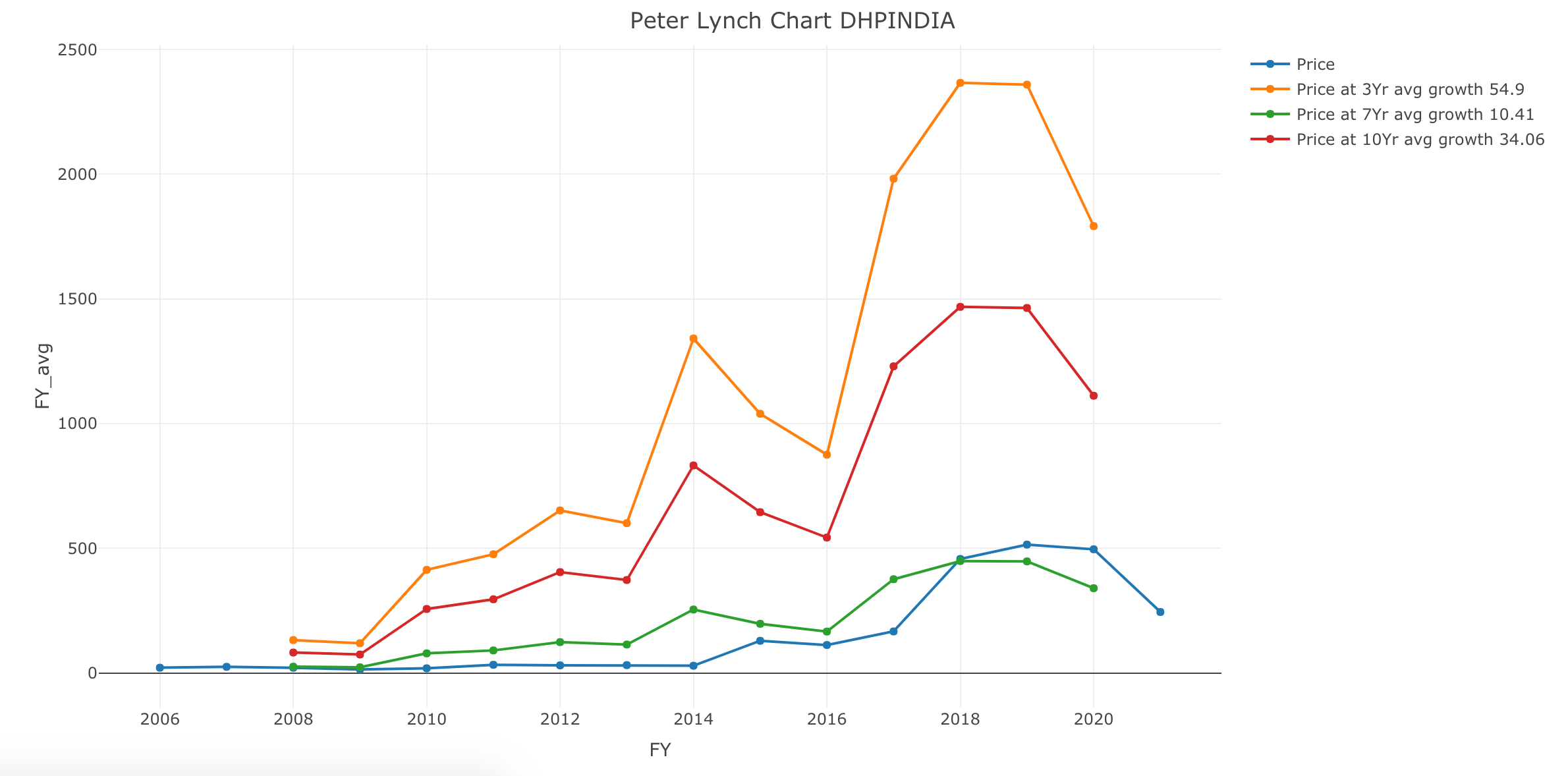

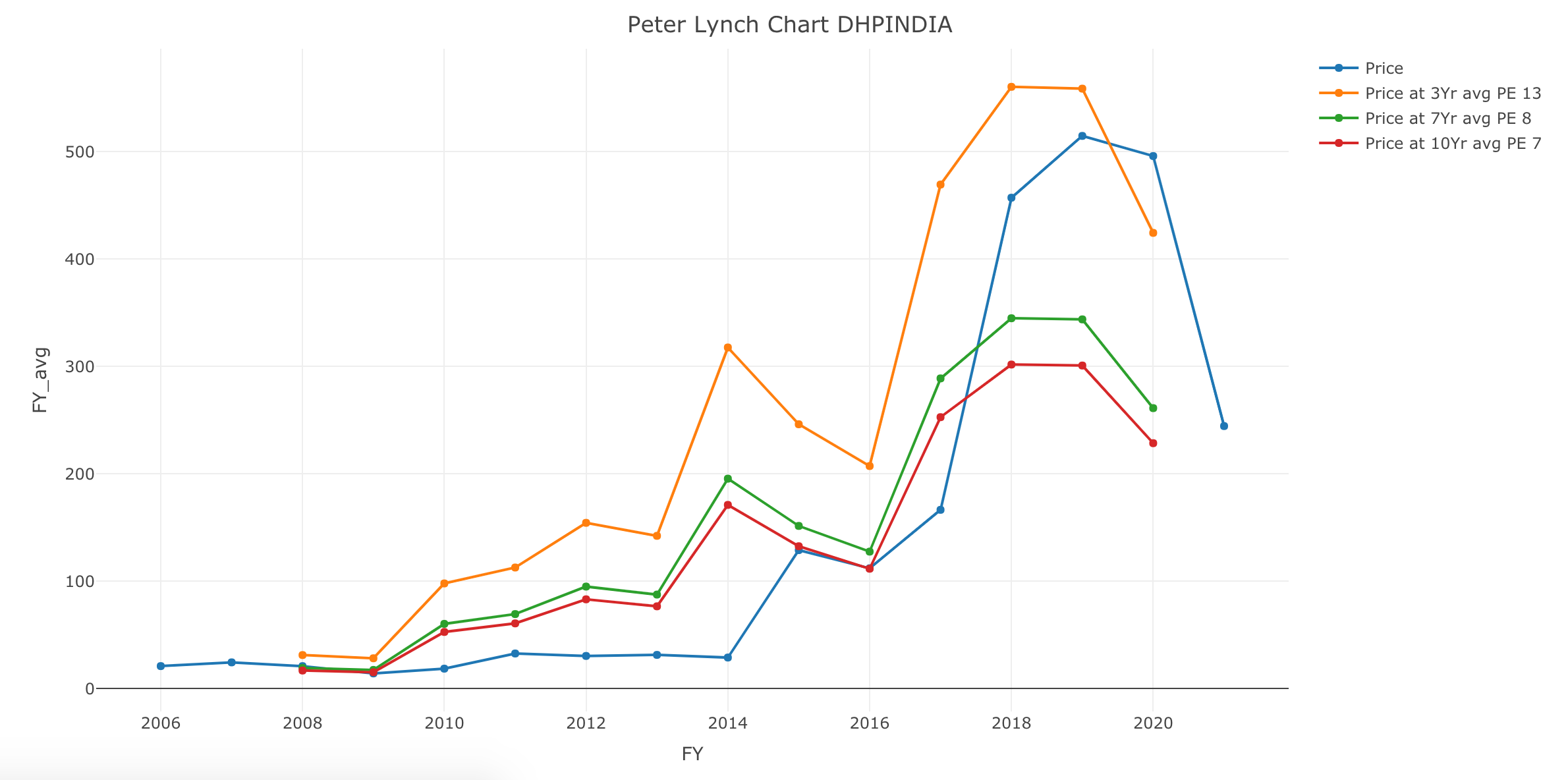

In India some companies always trade at premium due to corp. governance and other issues. So using historical PE instead of growth cagr gives us a better picture…

Also co looks like its back to its historical valuations… Just a simple PE chart…

Numbers look very interesting… I will study further…

Dicl: Interested but no holding… But may add in the future…

3 Likes

Thanks to all senior boarders here… Enjoyed reading all the posts… im trying to see who are DHP India clients. I understand they export to Europe. But whom are they exporting to ? I mean do we know the client names ? My apologies if I missed something obvious. Thanks.

They sell only scrap parts in India. So not much of a “client base”.

Name of some foreign customers are:

- Rotarex SRG (Germany)

- SOL Group (South America)

- Fairview Fittings (North America)

- VFT International (Singapore)

5 Likes

Thank you so much Dinesh… Very much appreciate it…

German client call them a partner:

This is a team that completely shares our philosophy for product innovation and quality

https://rotarexsrg.com/featured-product/511-111-series-tank-pressure-regulators

Germans dont call someone for namesake… I couldn’t find much with other clients…

6 Likes

Clarification regarding price movement is sought for the second time in 3 weeks while the company hasn’t yet replied to the previous one.

Fundamental analysis

- Coffee Can Filters

19% average sales growth over 10 years; 29% average Net profit growth - 15% CAGR of Sales over 10 years

ROCE of 27% average over 10 years

(Sales growth in 2015 and 2016 was negative - which is a botheration as to why it became negative)

-

Accounting Checks

Most of CFO over 10 years converted into profits

Self sustainable growth rate is 43% and company is growing below that. So debt must reduce. Nil Debt over the years - which means company has been paying off debt to become a 0 debt company

Company has 26% cash as a percentage of market cap!!! (So really the company is generating cash) -

Value Filters

Dividend yield low - company likes to give INR 2 or 2.5 as dividend each year. Not sure why the company is keeping so much cash on its book. Dividend payout ratio is only 6%. So this could become a divided play over time if management returns cash to shareholders

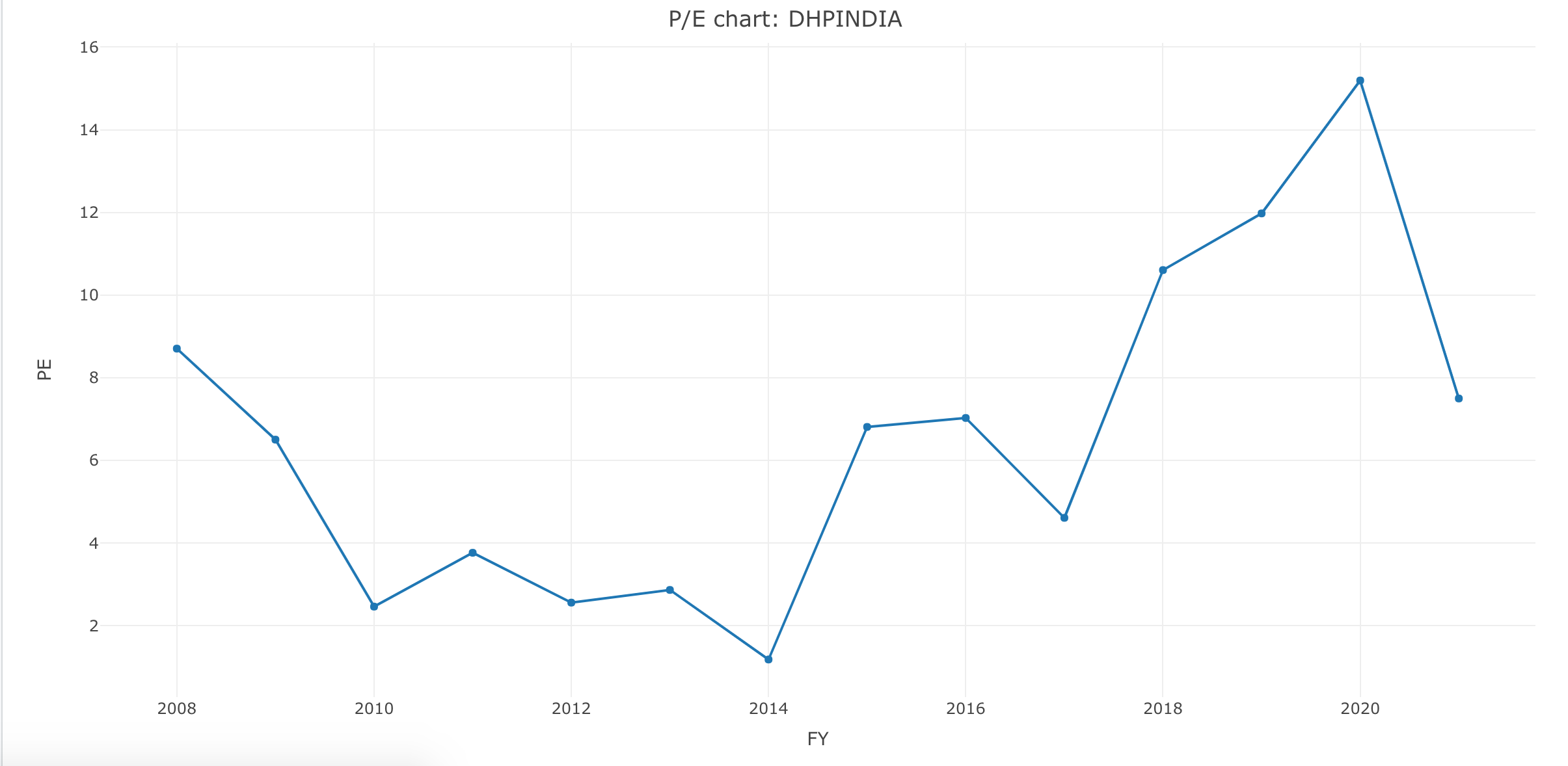

P/E has expanded to around 10.5. Earnings yield > Govt bond

Current market cap is 0.5 - 0.33X of true value as er Ben Graham method

Could be a 2-3 bagger over 5 years purely on earnings growth as I do not see P/E expansion beyond this point. Interesting thing is company is able to grow at a decent pace without need to take on debt and add cash. If we take cash out of market cap, P/E will be around 7 to 7.5.

Disc: Invested, around 150 shares at 338 INR per share

6 Likes

I believe this is a fundamentally good company. My only concern is the cash piling up.

If the management is not able to manage the cash properly, it could end up losing it. I would rather like to see the management putting all the money to good use.

2 Likes

Disaster results posted… Big provision posted for Covid …

1 Like