DHP results https://beta.bseindia.com/xml-data/corpfiling/AttachLive/70d5e854-c25e-4183-beef-e51073de6962.pdf

1 Like

Excellent set of results, in addition to improvement in financial position. Debt has come down a bit and Cash has improved a bit. Working Capital has worsened a little bit too, however.

3 Likes

Hello sir at what price to book this company becomes attractive in relation to its roe

At 12 P/E, 15%+ Revenue Growth, 20%+ Profit Growth and 20%+ RoE, I think it’s still very attractive at CMP. My only worry, as always, is the utilization of Cash. It’d help them to reinvest somewhere or acquire something that makes sense. But I wouldn’t mind receiving a Special Dividend too. What I’m worried about is Cash piling up, with nowhere to go.

3 Likes

Why did the company do bad in 2015, 2016? Was it one-off or bound to repeat? What was the mistake and steps taken by management to avoid it next time?

What are the countries to which the company export? Which are those companies?

Given the fragmented and some-what commoditized nature of the industry, is the company venturing into value-added products? Is there scope for value-added products in the first place?

Disclosure: Not invested and not well-informed about this industry.

There is not much info available about this company. Management seems to be quite conservative. Even if you read Annual reports of last 10 years, it is just a copy paste (only the numbers got changed  ️) let me share some info which I got based on my little research.

️) let me share some info which I got based on my little research.

Sale/profit drop in 15&16- As per the Annual report ‘this was due to the lower demand due to high competition in market’. Other than this no info available. If any body has attended the AGM he can share for the benifit to us.

They are exporting to North America majority of their products. Products are - pressure regulators for Patio Heater, Grill, RVs etc. Clients- ROTAREX SRG (Germany), SOL limited (South America), Fairview Fittings (North America), VFT international llc(Singapore). Regarding product category, yes they are facing completion but IMO their products are critical to safety and it is quite difficult to get the license and certification for supplying these products in export markets.This is some sort of moat IMO. Further I don’t have much info. If any senior member have done any shuttlebut it would be really beneficial for all of us.

Disc- Invested (just tracking position)

7 Likes

These are also my views. I tried to read a couple of their Annual Reports and got a headache. They are poorly structured and difficult to read.

As I’d shared in this thread earlier, only about ~70 players are licensed to produced Pressure Regulators in India (Since they are very critical safety components). Out of these, most of them supply locally. I don’t have the exact data, but DHP India is among the very few players that work in the export business.

While the licensing is definitely a smaller moat, I think the bigger moat comes from the production cost, what with them producing in India and supplying to Germany/America/Singapore. But we should be ready to admit that theirs is a quasi-commodity product and so, they can face headwinds as and when the cost leadership position is challenged. Until then, I think the cheap valuation offers a decent shot a good returns.

7 Likes

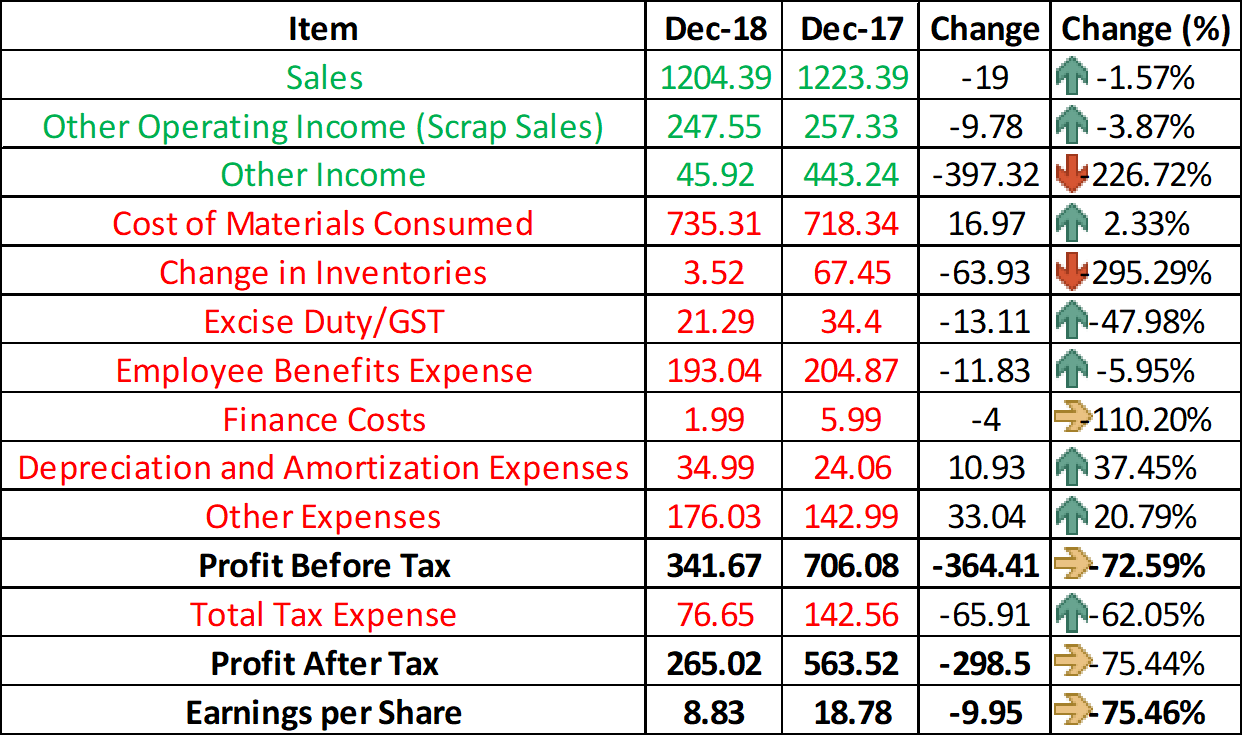

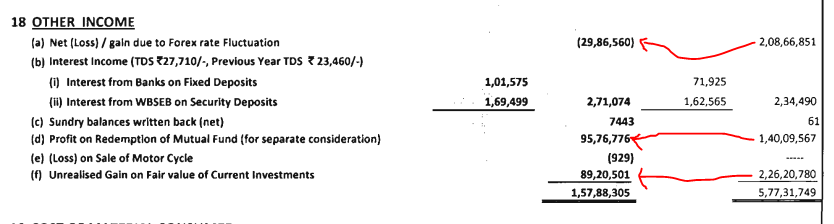

Poor QoQ results on the back of a significant drop in 'Other Income’

https://www.bseindia.com/xml-data/corpfiling/AttachLive/db1ed425-6948-4973-8f96-2409e3249794.pdf

For reference, here’s what ‘Other Income’ consisted of during the last AR:

My guess it it would have been largely due to change in FV on investments (They have a ton of Equity and Debt investments) and perhaps Forex losses. It is good to see that there has been very minimal change in inventories, meaning the old inventory is getting depleted. Finance costs have dropped sharply (Not that the leverage was that high to begin with anyway). Every other item has remained the fairly similar.

3 Likes

@dineshssairam True. I am however bit concerned about no revenue growth. Sales YoY has remained flat. Do you see this as a concern?

DHP India is a quasi order based company. So, I’d not bother about QoQ Revenues that much. We did have massive increases from Jun-17 to Jun-18 as well as Sep-17 to Sep-18 (70%+ in both cases if I’m not wrong). So for the year, I’d expect a generous increase in Sales overall.

7 Likes

Q4 results:

The board has recommended a dividend of Rs.2.5 per share.

2 Likes

Annual Report

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f14423de-2fd8-4c84-a093-529eaeecffbc.pdf

Couple of interesting things:

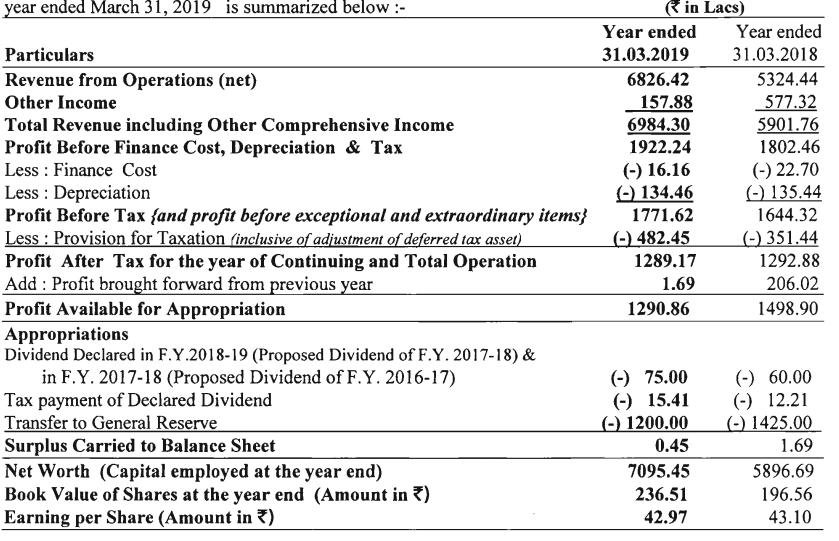

Financials Summary

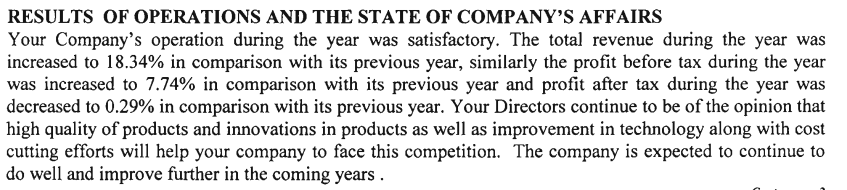

Management Guidance

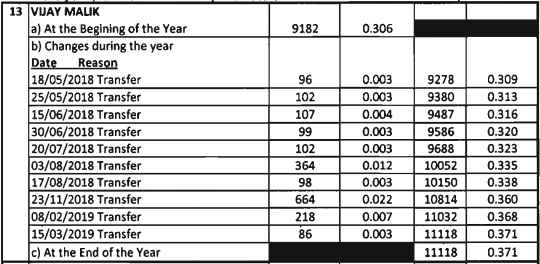

Dr. Vijay Mailk increased stake during the year

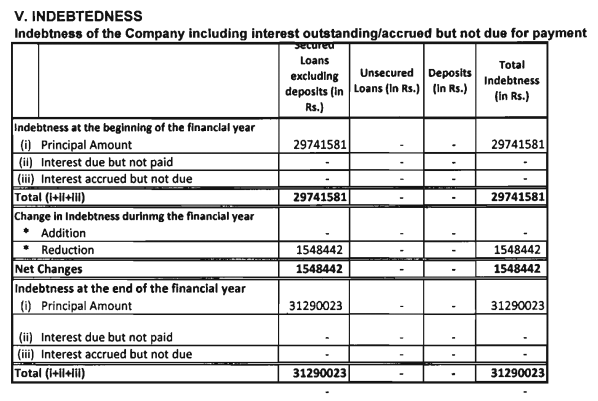

Borrowings have increased slightly

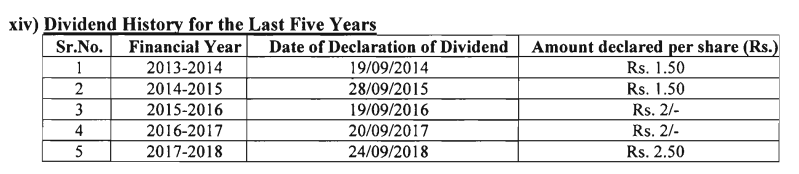

Highest Dividend historically

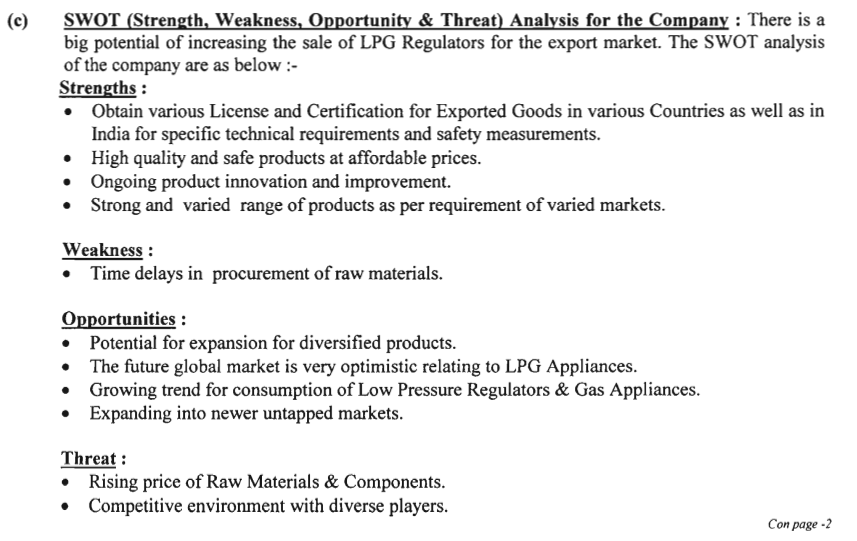

SWOT Analysis of the company

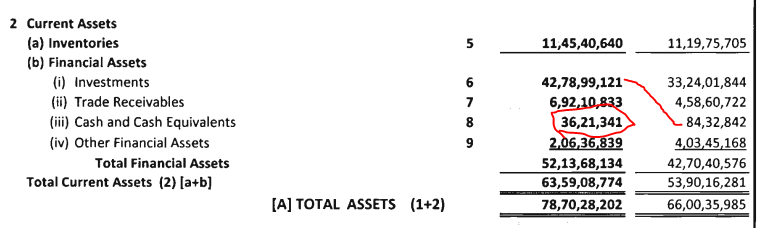

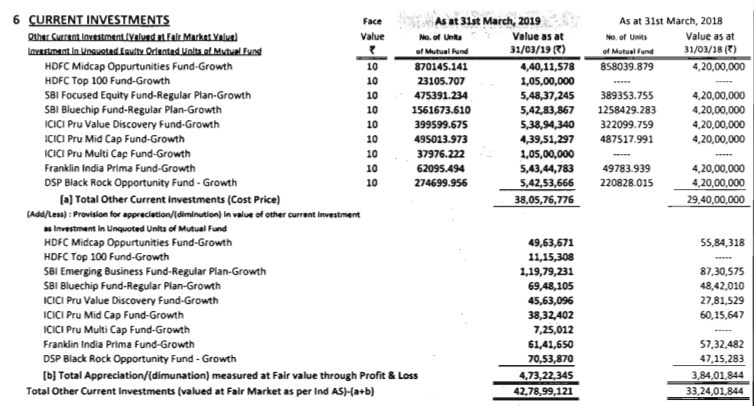

Shifting more liquid cash to investments

Liquid cash and investments now form ~25% of Market Cap.

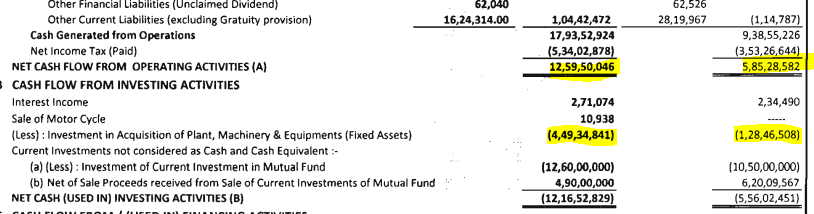

Strong Free Cash Flows

You can also see that they have invested quite a bit in MFs (We saw this above). Also notice that they have included ‘Sale of Motorcycle’ worth Rs. 10,938 in the Cash Flow Statement. If the management had pocketed this amount and didn’t include it in the company’s financials, the shareholders would have missed nothing and we’d have no way of knowing something like this happened. The fact that they have included an entry like this in the AR shows how good the management is. When was the last time you saw an entry like this in any AR?

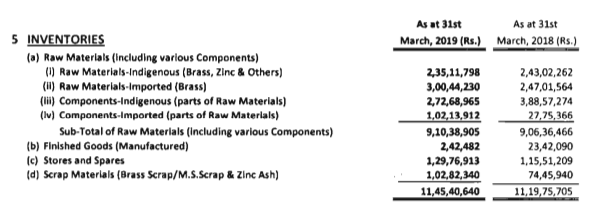

Stable Inventories

In fact, better inventory position. Sales has increased a lot and inventory has stayed the same.

Investments

Do any of these funds have exposure to DHFL? ![]()

Net Receivables

Receivables increased by 50%, while Payables increased by 72%. Once again, excellent performance - a confirmation of why they were able to produce such a high FCF this year.

Drastic ‘Other Income’ Reduction

I suppose I guessed it right a couple of posts back. ![]()

The markets (Both forex and equity) have dampened the accounting profits this year.

Major RM of the company

AGM Date, Time and Location, in case anyone’s attending

22 Likes

Noteworthy point below. I have repeatedly said that the usage of the cash on books has been the biggest risk in DHP India. This one here is not a huge problem, but why skip over something that can be done easily and save those small percentages in brokerage?

Update: I have written a mail to DHP India’s shareholder grievances e-mail to this effect. Let’s see if I get a response. If I do, I’ll post it here.

14 Likes

Terrible results. Huge drop in Sales and Profits.

Although it’s true that one quarter does not mean a lot, especially in B2B, I’m surprised by the sharp decrease in Sales and a sharp increase in expenses as well. Wonder what went wrong there.

2 Likes

If you see opm on qoq basis then there is some improvement still sales is down which is point of concern.

Can you please share industries where they supply, to get an idea whether its cyclical slowdown or something different.Even if sales is down still they were able to maintain Debtors and inventory level that’s one positive I m seeing in the results.

1 Like

Has not the company done brilliantly in the last 10 years? Has it not been brilliant last year. Only traders worry about quarterly fluctuations. The min. measurement period should be once in a year and not quarterly. This is because we really intend to hold a stock forever.

I’m not “worried”. Just curious. Even compared historically, the numbers are too bad. But I would absolutely continue purchasing DHP (Provided I have the cash) if it falls further.

.

@dineshssairam

I invested in DHP at 100 levels but exited when it reached 500 a year back as I thought it is no longer cheap and growth rate is nominal.

I’m curious to know, what makes you confident about this company as you said you are buying when it falls.

PS: My Allocation by value was low at that time as I had just begun my investing.

It’s a great company in an otherwise bad / ailing industry. Just a look at the historical numbers should tell you that.

I have some other Scuttlebutt information that increased my conviction, but the person I discussed it with didn’t want it shared publicly. So I will respect that wish.

But it’s not all rosy. It’s still a commodity business. On top of it, they are not doing proper capital allocation with the bulk of cash they have. These are some concerns I have and probably why my allocation will remain on the lower side (Currently lowest % holding in my PF).

2 Likes

The company is selling at 12 times free cash flow. The company seems to have bettered it’s position in the last 10 years and major performance ratios like ROCE and ROE look fantastic. It’s future will lie in its ability to utilise free cash productively in the manufacturing activity. I have 15% of my PF in this company, though it is advisable to put no more than 5% in such small companies, where you could either make a lot of money or lose everything.

At a time when quality is unaffordable, you can either sit at the sidelines, or invest in small cap quality. With around 74%, the promoter has skin in the game. The operating margin keeps fluctuating and the opm was even worse in June 2017, so I wouldn’t be worried about quarterly fluctuations. I could locate only one video of the promoter, in which he stated that they are constantly improving the quality of their product. And this is the only thing that really needs to be done.

2 Likes