Hi All,

Initiating my first thread on Valuepickr. I’m looking to own businesses with a long runway for growth, small-medium in-built MoS and Market Cap <2000 cr for 10/20/30 years. Ran the following Custom Screener and it threw up 11 companies, of which 1 I’m discussing here.

Debt to Equity < .5

EV to EBIT <8

Dividend Yield > 1%

Market Cap <1000 cr

Sales Growth 3 years > 15% (think this is showing for 2012-14)

Profit Growth 3 years > 15% (think this is showing for 2012-14)

EPS > 15

The following information is from the 2013-14 Annual Report :-

CORPORATE OVERVIEW :

DHP India Limited is a Manufacturing Company of LP Gas Regulator (Liquified Petroleum Gas Regulator), its accessories and parts thereof. The Registered Office of the Company is situated in Kolkata & its Factory is situated in Howrah District, West Bengal.

FUTURE PROSPECTS

There is strong competition in the market. Your Directors continue to be of the opinion that high quality of products and innovations in products as well as improvement in technology along with cost cutting efforts will help your company to face this competition. The company is expected to continue to do well and improve further in the coming years .

MANAGEMENT DISCUSSION AND ANALYSIS REPORT OF 2013-2014

[As per Clause 49 of The Listing Agreement with Stock Exchanges]

TO THE MEMBERS

The financial statements have been prepared in compliance with the requirement of the Companies Act, 1956, and Generally Accepted Accounting Principles (GAAP) in India. Our management accepts responsibility for the integrity and objectivity of these financial statements, as well as various estimates and judgements used therein. The estimates and judgements relating to the financial statements have been made on a prudent and reasonable basis, in order that the financial statements reflects in a true and fair manner the form and substance of transactions, and reasonably present our state of affairs, profits and cash flows for the year.

Apart from financial analysis, the management discussed on following areas :-

(a) Forward-Looking Statement : All statements that address the expectations and/or projections for the future, not limited to the Company’s strategy for growth, product development & innovation, market standing, expenses and financial results, are all forward-looking statements. These are based on assumptions and expectations in the future and the Company cannot guarantee its accuracy or its realisability. The Company’s actual results and/or performance will hence differ from those portrayed in forward-looking statements. The Company assumes no responsibility to publicly amend, modify or revise such statements on the basis of any future developments, information and/or events.

(b) Industrial structure and development : The Company concentrated on expanding the export market for its products and continues to do so.

(c) SWOT (Strength, Weakness, Opportunity & Threat) Analysis for the Company : There is a big potential of increasing the sale of LPG Regulators for the export market. The SWOT analysis of the company are as below :-

Strengths :

● Obtain various License and Certification for Exported Goods in various Countries as well as in

India for specific technical requirements and safety measurements.

● High quality and safe products at affordable prices.

● Ongoing product innovation and improvement.

● Strong and varied range of products as per requirement of varied markets.

Weakness :

● Time delays in procurement of raw materials.

Opportunities :

● Potential for expansion for diversified products.

● The future global market is very optimistic relating to LPG Appliances.

● Growing trend for consumption of Low Pressure Regulators & Gas Appliances.

● Expanding into newer untapped markets.

Threat :

● Rising price of Raw Materials & Components.

● Competitive environment with diverse players.

(d) Risk and concern : The Company is exposed to risks from market fluctuations of foreign exchange, interest rates, commodity prices, business risk, compliance risks and people risks. It is difficult to assess the risk involved in the business. It is always the intention of the management to minimize the risk involvement with proper analysis and market study & internal control systems.

(e) Internal Control and System Adequacy : Your Company believes in formulating adequate and effective internal control systems and implementing the same strictly to ensure that assets and interests of the Company are safeguarded and reliability of accounting data and accuracy are ensured with proper checks and balances. The internal control systems are improved and modified continuously to meet the changes in business conditions, statutory and accounting requirements.

The Audit Committee of the Board of Directors, Statutory Auditors and the Business Heads are

periodically appraised of the internal audit findings and corrective actions taken.

The Audit Committee of the Board of Directors actively reviews the adequacy and effectiveness of

internal control system and suggests improvements for strengthening them. The Company has a

robust Management Information System which is an integral part of the control mechanism.

(f) Operational Performance : The Company has already shifted the main focus of its manufacturing business from domestic market to the export markets and is confident of obtaining satisfactory orders in the coming years.

(g) Industrial Relation : The Company considers its human resource as the most valuable ingredient of the functioning of the company and utmost endeavor is made to maintain good relations with the employees at all levels

Now coming to the numbers :-strong text

CMP - 119.8

Market Cap - 35.94 cr

Issued Shares - 30 lacs

Promoter Holding - 74.37%

Debt to Equity - .12

EV/EBIT - 37.363 / 8.7559 = 4.27

EPS TTM - 19.23

P/E - 6.23

Divident Yield - 1.25%

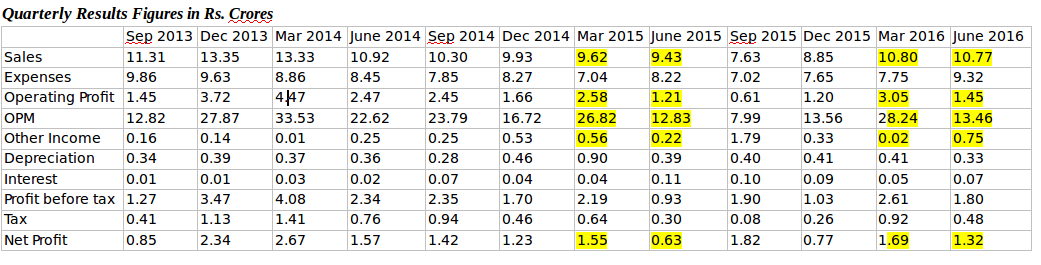

FY’15 numbers aren’t as good as FY’14 with 20% drop in sales.

I have absolutely no idea about the business/industry and the management. Also, never done a scuttlebutt before. My basic inference is that it’s earnings shouldn’t be cyclical given it’s product offering. Looking for your opinions / comments on this one.