Instead of May, plant should go live in July this year. Full marketing efforts are on.

There is huge demand coming for Phenol as one large US plant has been shut down partially (3 lac TPA). 9-10% growth in demand growth for phenol is more than expected. More downstream industries will come online with local availability of Phenol. Demand scenario at the moment is such that they will not be able to fulfill all domestic demand even while operating at full capacity.

Moratorium period for debt for phenol plant is till June 2020. This is good as there will be no interest burden until they ramp this plant up fully. First year (70% utilization) expected.

Regarding ethylene (RM) for phenol plant, it will be purchased from GAIL and BPCL.

Existing Operations

FY19 will be better than FY18 as they are doing brownfield capex (~60 cr) to increase capacity by 25%.

Margins should improve (due to China factor) starting Q3 and due to undergoing capex.

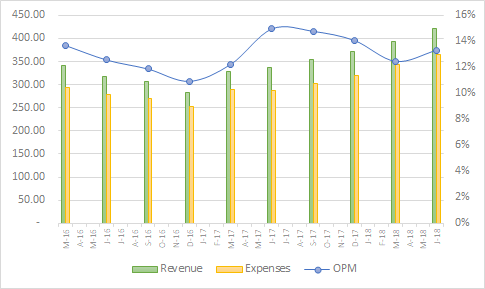

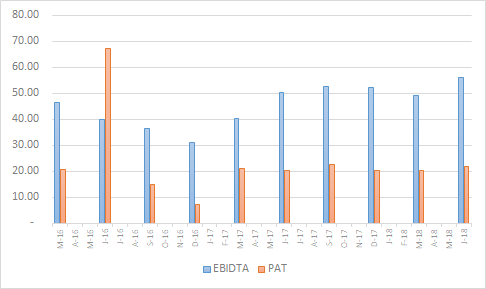

Highlights of Q4 FY18 and FY18 performance

Key Financials

FY18

o Revenue grew by 18 % to 1467 Cr from 1242 Cr compare to last year

o EBITDA grew by 41 % to 214 Cr from 152 Cr compare to last year

o EBITDA margin stands at 14.6 % over 12.3 % last year increase of 230 Bps

o PBT grew by 65 % to 122.08 Cr from 73.92 Cr due to sale of land compare to last year

o PAT grew by 60 % to 80.46 Cr from 52.15 Cr compare to last year

o PAT margin stands at 12.5%

o EPS stands at 6.34 Rs for the current year

o Depreciation stands at 51.95 Cr over 46.6 Cr last year

o Finance cost increase to 40.34 Cr Compare to 30.89 Cr last year

o Segment wise revenue

Bulk Chemical

• Revenue stands at 746.98 Cr over 695 Cr

• EBITDA grew by 21 % to 106 Cr

• EBITDA margin grew by 30 bps to 14.3 %

Fine Speciality Chemical

• Revenue grew by 23.6 % to 463 Cr from 375 Cr , contribute 31 % to total revenue

• EBITDA grew by 39.4 % to 115 Cr from 82 Cr last year

• EBITDA margin stands at 24.8 % over 22 % last year

Performance Product segment

• Revenue grew by 14 % to 299 Cr from 262 Cr last year, contribute 20 % to revenue

o Total debt stands at 452 Cr with Debt-equity ratio of 0.49

Q4 FY18

o Domestic Revenue grew by 23 % to 243 Cr over 198 Cr last year same quarter

o Export revenue grew by 16 % to 147.3 Cr over 127 Cr last year same quarter supported by high demand

o Segment wise revenue

Bulk Chemicals

• Reported 8 % growth in revenue over last year same quarter

Fine Chemicals

• Reported 23 % growth in revenue over last year same quarter

o EBITDA grew by 107 % to 30.1 Cr from 14.6 Cr over last year same quarter

Key Highlights

Plant at Roha has fully restored in May 2018 . So product capacity utilisation was less then maximum

Awaiting for brown filed CAPEX in

Address opportunity in textile and Detergent

Business Outlook

Export will run in full capacity utilisation in FY19 in fine and speciality chemical

Profitability expected to improve

Concentrate on brown field expansion of project of 60 Cr

Mega Green Field project

o Company is in pre-commission stage . Complete focus on start up . Company will become leader in Acid tone and Phenol in India after this expansion

Company had raised 150 Cr from QIP held in January 2018

Q&A

Which company had shutdown production of Phenol ?

o Shell has close its 3,00,000 ton from total 6,00,000 ton total capacity

o China also integrated into downstream product so they are captivity consuming their Phenol demand

Does current price of Phenol is sustainable ?

o From last 6 month price is in favour of company further it will also going up

At the current crack price what can be the peak EBITDA level ?

o 550-600 Cr

When will company operate on full capacity utilisation in new plant ? Does company have a strong distribution to CATER demand

o Yes company had established it and in process of signing with distributors . Ramping up of Phenol utilisation will not take much time . People in market are waiting for company production . Company have important 125 customers and out of them 25 are more important . Company also get highly experienced marketing team

How will company make OVM business profitable ?

o This year it will be positive EBITDA as demand is growing in the market

How is the attraction on Acid tone ?

o Parallel work is growing on Acid tone as demand is increasing

How much margin improvement can be seen in next year ?

o Much better then current because the demand growing very well in all segment

o In fine chemical also company is starting the plant . Spending 60-70 Cr in growth CAPEX . Production will start by end of second quarter

o Company is now reaching at Peak facility in all the segment

Does company have any dependence on china ?

o No

Does company see threat from Saudi Arab as they are also expanding capacity ?

o Yes threat is their but they are not focusing on Indian market they are supplying to China .

o Demand in India is rising . Import is coming but in very small quantity so it is not a issue

What kind of peak revenue can be achieve at current capacity utilisation ?

o Company will expand 20 % capacity . At 100 % utilisation company will be able to sell entire quantity.

o Thinking of investing 70-75 Cr in Pharma in agro product

What will be the impact from supply side on prices ?

o Company will have own pricing policy going forward

What is the debt repayment plan on Phenol ?

o It is a 20 year loan and payment will start in July . Company don’t want to be a zero debt company because company want to grow and have plan to expand

How much companies will supply raw material to the company ?

o Company had tie-up with BPCL , and talking is going with GAIL

Hi,

As per mgmt concal, phenol/acetone project at peak utilisation generate 500-600cr. As per earlier concal mgmt indicated they can clock 15% ebitda margin, so it means they can generate around 3500cr out of phenol/acetone project itself and core business currently generating 1600cr and in next 2 years it can scale to 2000cr. So fy 2020 the revenue of 5500cr possible , which is on track of promoter goal of $1 bn revenue by 2020.

500 Ebidta is overall - taking this number: assuming it happens by 2021, current EV = 5000 cr, so it is trading at 10 times 2021 EV/EBIDTA. assigning a 20 EV/EBIDTA multiple at exit would give a 10000 cr EV.

IMHO, This is very simplified valuation and I am not sure if this is the right way to value this business - but I am going to be happy if my valn. assumption work out by 2021.

Others please feel free to suggest your valuation criterion.

Revising your valuations a bit, current EV = 4000 Cr, current EBITDA = 200 Cr, implying EV/EBITDA = 20x

Incremental EBITDA at peak = 550 Cr, At 12x EV/Ebitda EV should be (550+200)*12 = 9000Cr. Expected debt is 2000 Cr, equity value = 7000 Cr against current MCap of 3500 Cr.

The Shell US plant has been ‘idled’ and not shut down as phenol margins became drastically bad. This will sure improve local demand, but not prices. As soon as prices/ margins improve, the production will be restarted.

This may not augur well for average margin expectation of phenol-acetone over benzene-cumene over the next 12 - 24 months.

Some commentary on the Chinese impact. Environmental challenges and production disruptions in China led to volume gains for local customers boosting domestic revenues. Phenol demand is also growing globally, due to which, the demand-supply capacity is moving towards equilibrium, as downstream projects in China which commenced earlier during the current calendar year have led to greater captive consumption of Chinese Phenol capacity. Developments in the Chinese market have been accompanied with shutdown of a large global facility for production of Phenol in the US. These factors have resulted in firming up of overall prices of Phenol globally.

Strong commentary. I wonder why they have opted to submit only standalone numbers for fy19. We all know phenolics is going to take some time ramping up so numbers can be misleading…but still i would have preferred a wholesome picture. They should do 2000 cr additional topline with 100-120 cr pat from phenolics by 2020E. Phenol demand is increasing at a rapid pace here in india and the supply demand mismatch globally is almost becoming negligible.

RM cumene is made from benzene and propylene which will be sourced from reliance and bpcl. Tie-ups already in place in part.

Differentiator here will be cumene transportation cost savings, Phenol/Acetone demand cluster around Dahej, RM cluster around Dahej (Propylene will be sourced from Cochin), best tech from KBR, and hedge cost savings for clients.

Risks - ADD removal (but seeing how demand is rising domestically, won’t hurt DN much), pollution risk (in case of leakages)

Valuation - isn’t cheap and a lot looks to be priced in. (Subjective)

Good thing is that the base business is doing very well and commentary is pretty bullish.

Can someone through light on the 840 cr debt and its repayment structure?

Consolidated Debt: equity is 1.07 times. The only worry is that if phenol prices don’t support the volumes, debt and interest burden will have huge impact.