Qip allottement list219f1a16-2c0c-4f22-b28e-c25253a8aad4 (1).pdf (1.6 MB)

1 Like

u can check https://www.researchbytes.com/ it has the concall audio links, but u have to create a login.

From Q3 result note -

1 Like

Here are notes from pvt discussion with @snowprince …for everyone’s benefit…

Please take a look at the attachment (from Anand Rathi Securities). Deepak Nitrite _Anand Rathi.pdf (1014.8 KB). This is an old report but still relevant for what we are looking for.

In summary, Phenol/Acetone project requires two key ingredients (Benzene and Propylene). India is Benzene surplus but Propylene deficient. That is why India till date imports almost 80% of its Phenol/Acetone demand despite huge growing demand. Now check this article from Platts -

https://www.platts.com/videos/2016/july/india-phenol-acetone-prices-071120162 as per which India’s has got strength to influence Phenol and Acetone pricing due to its ever rising demand for these chemicals.

Regarding margins -

Final project margins for this project will depend on these factors.

i. Anti-dumping duty ~7%, which will help the domestic manufacturer.

ii. Basic demand/supply equation. South East Asia is a big market for Phenol. Platts report confirms that.

iii. Crude impacts Benzene/Propylene prices.

iv. Efficiency of the plant. The tech is sourced from KBR, and is the best tech available for Phenol manufacturing.

v. Demand centers (mostly close to Gujarat/Maharashtra belt). So transportation would be cheaper from this new plant as supply is close to demand.

I think Deepak Nitrite has chosen this project in such large capacity as there is good demand for these organic chemicals in India, prominent RM Benzene surplus, supply/demand proximity, anti-dumping duty, and instant absorption of all supply (80% utilization in 1 year). I am unable to pin-point exact margins for this as it is dependent on various factors but may be we can check some transcripts where they might have discussed this in detail. In my opinion it would be close to 14-15% as they won’t go with something at such magnitude, which is lower than their current return ratios.

9 Likes

Mridul,

How Deepak nitrite make sure availability of proplyne then?. Do you have any information on this, who is the major producer of proplyne and demand supply scenario of that?

Thanks

Regards,

Sathish

1 Like

Propylene is mostly imported in India. Demand is much more than supply. This is probably because Propylene produced in refineries is used to produce more valuable downstream products.

http://cpmaindia.com/propylene_about.php

The global propylene capacity for 2016 is projected at ~127 MMT while the demand is pegged at ~102 MMT for 2016.

In India, the propylene capacities is projected to be ~4.7 MMT for 2016-17 and expected to increase to around 4.8 MMT in 2017-18. The market of propylene in India is anticipated to grow at a 8%CAGR during 2016-2025 as demand picks up from automotive, FMCG and other industrial sectors. India accounted for a share of ~10% in the global propylene market in 2015.

Main producers -

BASF SE, China National Petroleum Corp. (CNPC), Eni SpA, Enterprise Products Partners L.P., Exxon Mobil Corp., Formosa Plastics Group (FPG), Ineos Group Ltd., LyondellBasell Industries AF S.C.A., Reliance Industries Ltd., Royal Dutch Shell PLC, Saudi Basic Industries Corp. (SABIC), Sinopec Corp., The Dow Chemical Company, Total S.A., Valero Energy Corp.

Indian Oil also produces Propylene. https://www.iocl.com/Products/Propylene.aspx

In a crude oil refinery, propylene is a coproduct of FCC units producing useful lighter products from atmospheric and vacuum gas oils. In areas where the refinery olefins supply is plentiful and there is a need for a high octane motor gasoline blend stock, the propylene and butylenes are often used to manufacture motor gasoline alkylate. Although the propylene yielded from olefins plants and FCC units is typically considered a coproduct in the process to produce the more important primary products of ethylene and motor gasoline, propylene is also increasingly commercially produced on purpose.

6 Likes

Even I am trying to figure out the proplyne supply - major suppliers are like reliance, IOL etc and total demand for DN is apporx. 2% of the total domestic production - but I am not sure of the pricing as such in case they want to squeeze out DN.

The assumption of 80%+ plant utilization in the first year seems a bit off to me. While the current demand in India is high, it is important to note that the demand is currently being serviced by someone. For such raw materials, large consumers typically do a longer term contract (6 months - 1 year) and these contracts will be done in March - April with traders/ international manufacturers. Large consumers may buy only part quantities in the first few quarters until supply from DNL stabilizes. Added to that, plant stabilization with all equipment working and rated capacity will take some time.

Deepak Nitrite will have to start importing phenol themselves so that they can honor quantity commitments. It depends on how quickly they are able to implement this and capture the required share of the market.

1 Like

Mythace,

For same reason they are doing seed marketing past 2-3 quarters. And I hope they can able to get most customers on board once plant commission. I agree first 2 quarter very hard to achieve guided capacity utilisation due to teething problem, may be 3rd quarter they can achieve 80% utilisation

Could someone pls explain the difference between chlorophenol and phenol acetone? very limited knowledge around chemicals  … Valiant seems to be into making chlorophenol hence the question?

… Valiant seems to be into making chlorophenol hence the question?

Chloro phenol is a further derivative of phenol. post chlorination of Phenol, you get para and orthophenold depending upon the time you run the chlorination. Deepak Nitrite is a manufacturer of phenol and sells its phenol to players like valiant who further process it into chlorophenols.

2 Likes

Many thanks mate, that makes sense.

Can somebody gather and share negative points or better to say criticism on Deepak Nitrite please. Need to study all aspects including negative side of this stock also.

Disclaimer : Took small position and interested to invest more % of my Portfolio.

Q4 quarter result good top line growth , but bottomline dragged by tax and other expanse item.Operationally company did well, ebitda margin improved very well and closer to 15% is very good sign. Overall operationally this quarter result looks very good. But couldn’t find reason for higher tax expanse and other expanses. And also performance product division struggling to break even

Regards,

Sathish

1 Like

Investor Communication: Q4 and Year Ending

1 Like

Overall the results look good, Now let’s see the new plant - how it shapes up

No tangible information yet on when the new plant will be operational.

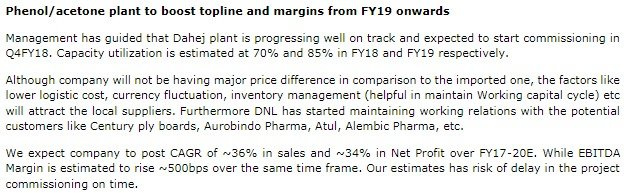

HDFC report dated 24th April…target price 302-348

1 Like

Excerpt from the above mentioned HDFC report regarding Phenol/Acetone plant. (Company will not have any major price difference vis a vis imports)

2 Likes

Wasn’t that the case always?

It was just that the companies which are currently importing, will move to domestic procurement as procuring domestically will lead to shorter lead (working capital) cycle and as well as no risk of forex fluctuations.

as per my understanding companies procuring from DNL, will save on logistic cost and interest (due to shorter cycles).