Wow! That is some guidance. Almost 5 times its current revenue in next 4 years. MD himself says that’s optimistic.

I have gone through the whole thread. I feel there are lots of things which effect this business. Crude price is one that effects topline and PAT big time along with inventory and offtake.

Regarding OBA division break-even (at PAT level), mgmt guided for Mar FY17, but has still not happened even after 5 qtrs post the original guidance. So approvals are taking time.

Some questions -

What would be approx revenue contribution from Phenol-Acetone plant (around 2000 cr at 80% utilization as per Anand Rathi report)? Margins are supposed to be close to 15% int his division.

@snowprince@ankitkhemka7 - Any word on competition from GAIL in Acetone and Phenol division? When is the GAIL capacity coming online?

Why are they paying dividends when they are doing QIP and raising huge debt for capex? They could have saved 60-65 cr in last 3 years had they not paid dividends.

What is the cost of the debt? What is net debt at the moment? This company has been constantly raising debt but not trying to reduce it, as constantly coming with some new project. Have they cleared their plans on debt repayment post the large greenfield project? What are the repayment terms?

@basumallick - They have guided to grow Specialty chemicals business at 15% CAGR for next 5 years. Will they be needing any capex for the same? I believe revenue from Phenol/Acetone division would not be included under specialty division…Correct me if i am wrong.

ROE - They have been extremely poor on this front.They have constantly said they will improve margins as contribution from Specialty Chemicals division increases, but the things are yet to reflect in the numbers. Similarly, Asset turns have been reducing constantly from 4.6 (2012) to 2.1 (2017) probably because they are constantly doing capex and are unable to utilize that as per their expectation. Leverage is continuously increasing. So all three parameters of ROE are questionable.

Receivable days (from 52 days in 2009 to 91 days in 2017) constantly rising every year.

There are lots of such questions which from Balance Sheet point of view make this a questionable investment. There are better companies with much better operational metrics than Deepak Nitrite. Though, phenol plant can change the dynamics for this company (that’s what i am betting on).

Q2 results have been good. Revenue increased by 16% drive by fine and specialty products and performance products. EBIDTA improved by 43% due to better product mix and higher realisation. PAT grew by 53%.

Overall, business is doing good. For multiple reasons, customers are reducing dependence on China for raw material which is benefiting DNL.

However, the star performance will come from Deepak Phenolics Ltd, its subsidiary. The Phenol plant will be operational by Q4. Sometime back, I read this product will add Rs. 1000 cr to the revenue. Current TTM sales are Rs. 1288 cr. So, almost doubling sales.

Phenol, in Nov, in Asia was trading at 1065 usd per ton, while acetone was trading at 765 usd per ton.

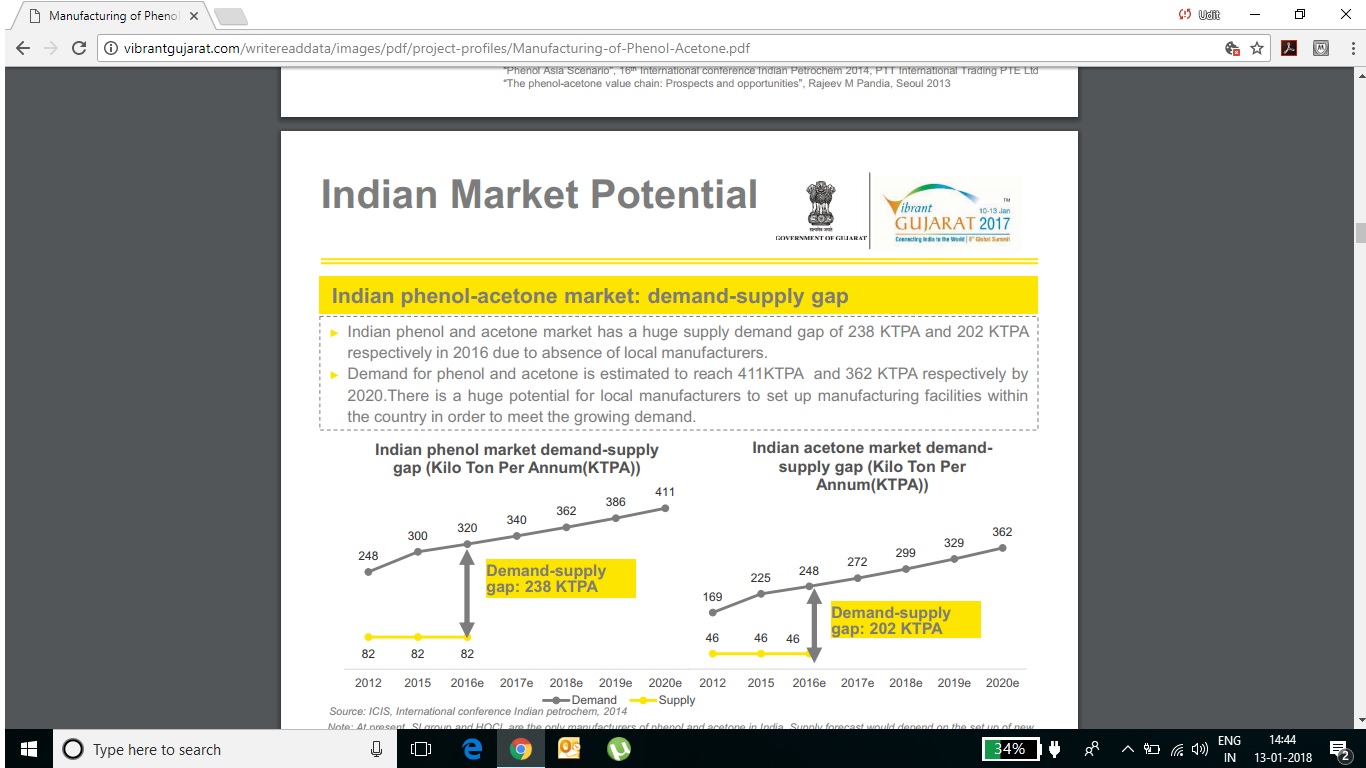

Now, as we know, DN is coming with a plant with 200000 mtpa capacity for phenol and 120000 mtpa capacity for acetone. Thus, aassuming 65 inr per usd, at full capacity, gives 2000 cr adfitional revenue. Key to rerating will be the margins here.

The margins will be descent as the Company has already done test marketing. Majority of the current requirements are met by imports in India. Any idea of the QIP the company wants to raise…the quantum as well as the timing?

Not sure about quantum. Should be priced around 205. They are supposed to meet tomorrow regarding this.

Reg. Margins from phenol and acetone, should be ~15% as per analyst reports. Yes, the products will be consumed domestically and it is likely that all production would be consumed.

the new plant will commission in H2FY18 (mostly it will be in the last quarter)…the revenues will start to reflect in FY19…a few points i found in AR 2017

1. Products cater to a long list of industries like pharma, petrochems, papers, textiles, agrochemicals etc.

2. Global leaders in several niche products like Xylidines, Cumidines, Oximes and colour intermediaries.

3. Doing capex at Dahej for manufacture of phenol and acetone.

4. Witnessing a global shift of manufacturing of chemicals to india. India ready to become the world’s chemical manufacturing hub.

5. Has set up a manufacturing plant at dahej to manufacture 200000 MTPA of phenol and 120000MTPA of acetone supported with manufacturing of 260000MTPA of cumene which is the raw material. Capex planned is 1400 crs. Approx.

6. Already started seeding of phenol in domestic market to establish strong marketing and distribution channel.

If additional revenue after adding phenol and acetone comes to 2000cr… And assume that the net profit margins will be around 3% (being conservative here.) then 60 crores will get added… In 2017 net profit was around 97 crores… Around 160 crores will be the net profit…as of now 13.1 cr outstanding shares are there ( share capital 26.2 crore and face value is 2) so eps will be around 12 rs…assuming a pe multiple of 20 it will be around 240/- …dont u think the expansion is baked in to the current price??

Hi,

Below is my understanding and basic calculation. I am looking at from what deepak nitrite can achieve in revenue over next 3 years. From core business side they are close this year with 1500cr revenue. In most of the business they are market leader, and so it can grow 15% top line next 3 years, so bare minimum core business can do 2000cr by fy20. And come to phneol and acetone project, this business has potential to generate 2000cr at optimimum capacity at 2020. And as per mgmt guidance in core business they can add 1% ebitda margin every quarter by way of process improvement and so by 2020 they can do 15% ebitda margin on sale of 4000cr. So it can fetch me 600cr ebitda. And total debt around 800cr, so interest outgo of 72cr per year. And 1200cr plant , and plant life time take 15 years so depreciation for phenol plant come to 80cr and core business plant depriciation around 40cr. So it has potential to generate pbt around 408cr. And if I take 30% tax rate they have to pay. I will end up with PAT of 285cr and pat margin of 7%. Instead of valuing in pe wise, I am valuing it as sales wise as most of their products are commodity so I am giving valuation of 1x sales. So it can achieve 4500cr mcap by 2020. So I am buying business which has potential to go to 4500cr mcap and I am buying at 2500cr mcap today. Please let me know whether I am making sense

Regards,

Sathish kumar jalantran

Hi All,

I did some basic research. Phenol and Acetone are widely used chemical intermediaries. They are further processed to produce various industry specific chemicals like Bisphenol A, phenolic resins, Aniline etc.

This provides Deepak Nitrites scope for forward integration and new avenues for growth. The company’s target of $1billion dollar revenue (6500 cr) by 2020 is keeping this in mind.

Also I agree that margins will be the key here, since the raw materials cost would almost be 80% of projected revenue.I did some calculations and only Benzene and propylene(main raw materials) costs come to 1550 Cr for the projected 2000cr revenue. Hence those invested or planning to invest should track the margins closely.

Utsav,

I agree there is oversupply of these commodity chemical in the world today. But consider below situation, as there is no domestic manufacturers for these chemicals. So who ever wants to these chemicals they have to rely on imports. As per mgmt comment, these chemicals caters to lot of end user industries. And each one of them requires very low volume,so they can’t directly import from outside and they have to buy through traders and for traders they can’t store large volume of inventories of these chemicals and he needs to take foreign currency fluctuations risk and also there is already anti dumping duty is present for these products. So those whoever procuring needs to bear all these extra burdens. And if there is one local reliable supplier comes for these chemicals most of above issue will be taken care. And as most of raw materials needed for producing these chemical surplusly available In india and that too nearby deepak nitrite plant. In my opinion they can produce phenol/acetone at competitive price . and they are going to work on cost plus model so there won’t be much margin fluctuation.Given all this I don’t think margin will be cone under pressure unless somebody else will start production locally .

agree with your point that above 80% of the requirement of acetone and phenol are imported into India.

The biggest thing i can make out of it is that to setup such a big capacity a company has to incur huge capex which in itself is a huge entry barrier and also add to that the growing demand for phenol in India in the years to come. phenol market is expected to grow at 10% CAGR till 2022 if i am not wrong.

Deepak nitrite came out with good set of result.

Top line - 371cr vs 283cr yoy

Bottom line - 20cr vs 7.3cr

Need to understand why performance product segment which turned around last quarter again posted loss this quarter?. (Understand whether Any seasonality effect ).

Ebitda margin too dropped little bit compared to last quarter,mgmt guidance of 1% margin improvement every quarter.

Waiting for concal to get more detail

I am pasting a few of CMD’s statements here, from the investor presentation above:

We are especially heartened by the performance of the Basic Chemicals and Performance Products segment which has delivered enhanced profitability due to robust demand from local customers who are benefiting from supply disruptions in China

Basic chemicals definitely have done well. Performance Products also actually have done well as compared to last year, though the net profit from same is still negative. Nevertheless, good to see the demand growing. To also add here, due to recent environmental issues in China, for the next year or two at least, demand from there should remain, till things improve there.

We are on the cusp of commissioning our Greenfield mega project for production of Phenol & Acetone. This global scale plant, aligned to the Make - in - India initiative, is poised to commence commercial operations shortly. This will elevate our performance and the opportunities for forward integration will open up new platforms for growth in the ensuing years The Greenfield project has now entered the last lap of construction completion and finishing work. There has been enhanced focus on operational readiness and flawless start-up for which technology provider’s team is at the project site and has commenced the final checks.

It is good to see that they are on track and on time for the phenol project. I do not remember the last con call details, but they had planned to start production first week April, and it looks that they should be able to do it considering that the final checks for the project have started.

The company is raising additional 150 crores through QIP in addition to 150 crores already raised in March 2017.

The floor price set is Rs.277.30 against the CMP of 286 and opened on 22nd. The board is meeting today to determine the price of the equity shares to be allotted. Is there any source where we can check on the subscription rates of QIPs?

Hi,

As per latest QIP allotment announcement, the company allotted share of company to QIP at 264 rupees vs floor price of 276 vs CMP 291. I have query why company allot shares much lower than floor price?. is it indicates company not able to convenience institutional investors to invest at that said floor price or demand is tepid from institution due to recent run up?. how to interpret this development.

And compared to last QIP allotment announcement, company didn’t disclose this time whom is the institutional investor bought this time