Did anyone get the Concall? Please post notes if possible. Thank you.

Notes from concall

Next year guidance :

Topline 105 - 110 Cr & PAT - 18-19 Cr

Margin is 15% in MC & 40-45% in FC

Expected EBITDA - 27-28%

(expected MC in next year 65% / FC will be 35% - it keeps the bottom line capped)

3Cr inventory loss - Preventive measure taken is no further production on verbal commitments

Brazil -

Order balance is 68 Cr

Brazilian budget cut impacted approx 8 cr in top line for Q4 (Management committed 45 Cr for Q4 but could achieve 37 Cr)

South Africa -

Balance 17 cr order is expected to finish by Sept’19

Next year (Oct’19 - Sep’20) is still unknown, Cupid is trying via JV with new partner

Last year tender qty was 40 mn pieces

US - cupid gets $1 per piece, while the vendor gets $3 per piece, cupid exploring direct entry to US but cost of marketing is too high & currently not in their control. They are ready to spend 1-2 mn on marketing & try out

Currently selling online FC in US w/o registering product as FDA doesn’t stop them from online sales. They expect online sales to double in next 2 years. There was 33% increase in last year, although quantity is very small

Raw Material : Latex price is normal but Silicon oil’s price went up (approx 40%) & again came back in normal range

Dividend Payout : Mgmt will continue 40-45% dividend payout policy

Other expenses went up by 5Cr in FY18-19 - It was business development expense

Water based jelly - production capacity 75 mn/yr (Rs 1 Cr) - capacity utilization is 90% & margin is 50% - selling through NGOs

Plant / Property expense has gone above by 4 Cr - purchase of equipment worth 4.8 Cr

Female Health / HLL / Cupid - 3 manufacturers are qualified for SA last year

Business succession - CEO - no luck as management is searching for marketing oriented candidate with financial background

Note : Please cross verify before consumption as I may have missed certain part

6 Likes

Dear Mr. Rai thank you for your efforts. I continue to maintain that management guidance should be trusted only 50pc.

Yes, but this time management is super conservative, adjusting for the write off the company already did 18 - 19 cr this year. So pretty much flat in terms of profits (y-o-y). Don’t think it gets any worse than this (fingers crossed). I think the loss of the south African tender business is a big blow and until some replacement comes up (US business or replacement SA JV) the company will continue to flat line. The Brazilian tender compensates to a certain extent…

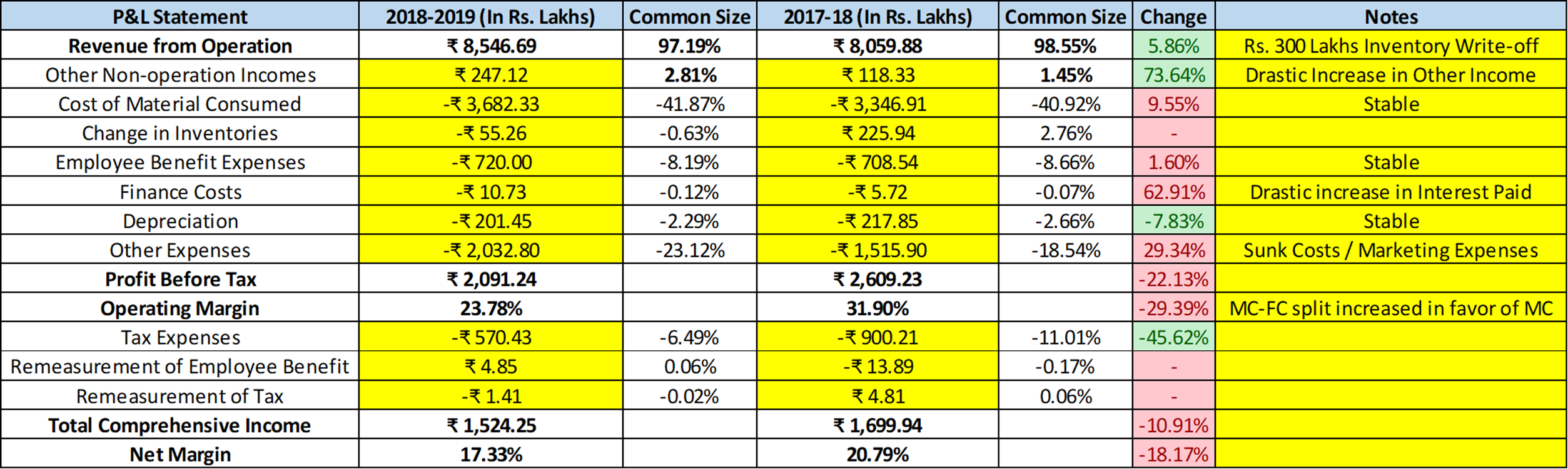

Dismal show by Cupid overall, but most of it can be tied back to the unexpected inventory write-off and the sunk costs / marketing expenses in entering new markets. Let’s hope things get better from here on out. Rs. 105 Cr (Expected Sales) * ~20% (Expected Net Margins) gives us an expected yearly Net Profit of Rs. 21 Cr, which is +38% from current levels and +23% from last year’s (A more ‘normal’ profit level).

Cupid - Results Analysis.xlsx (17.2 KB)

3 Likes

Appreciate your analysis.

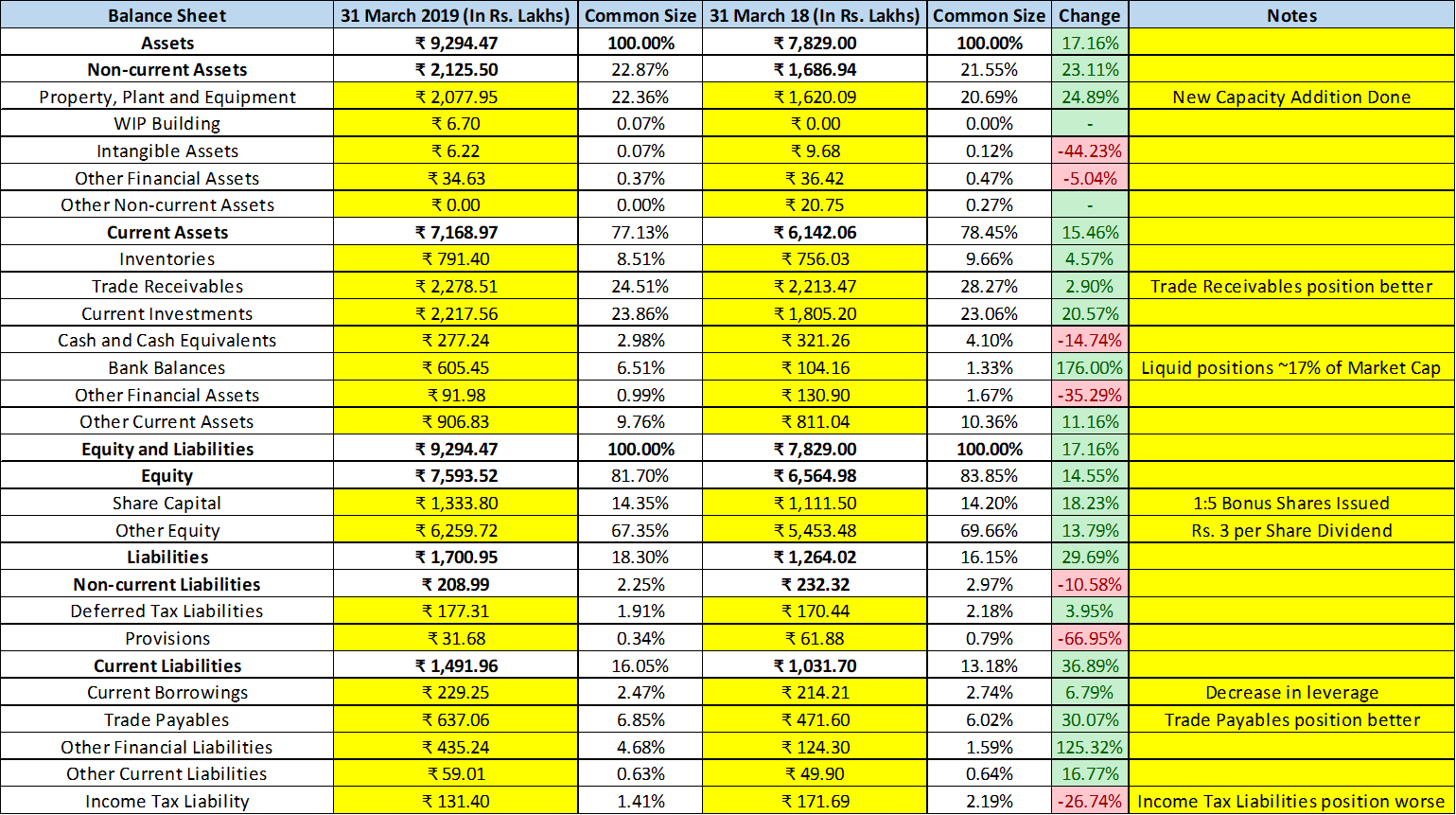

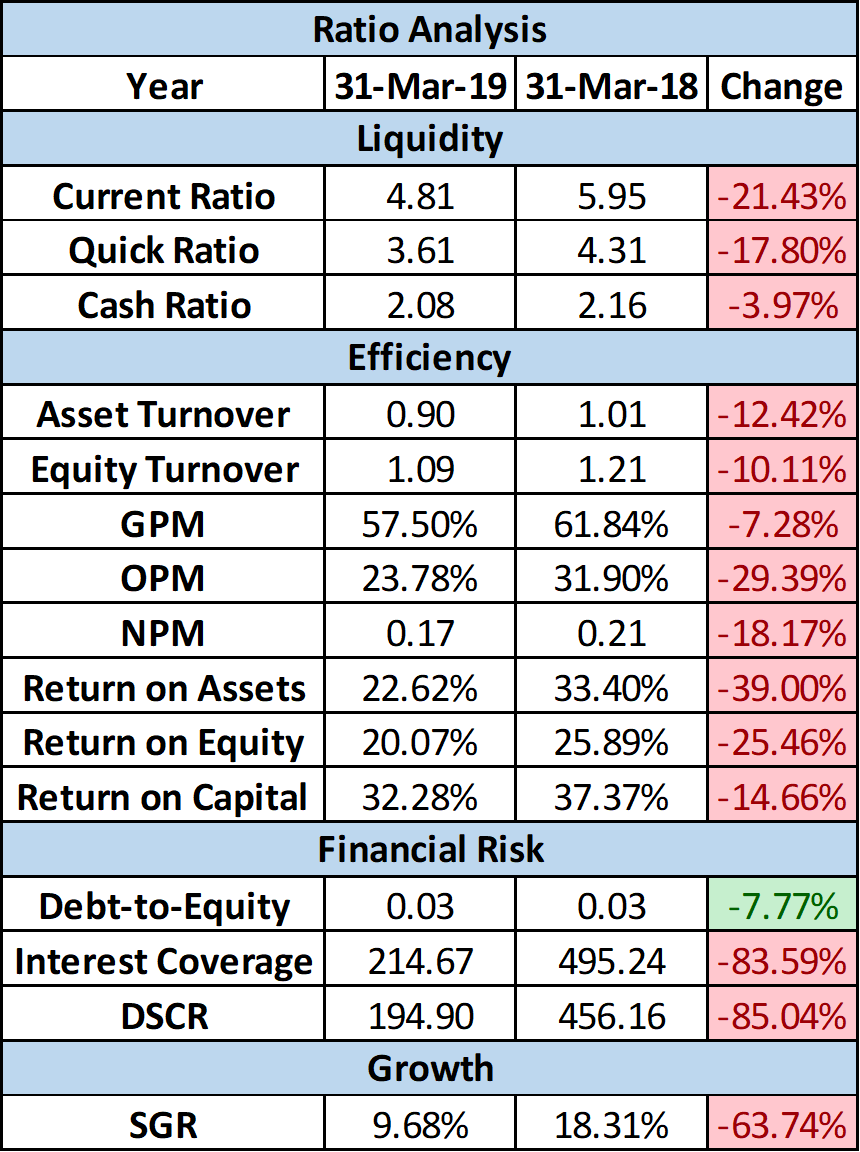

ROA and asset turnover is not relevant for these industry types. They have a decent FA turnover ratio.

Secondly the normalized ROE is higher when the inventory effect is taken off. Not sure if 2018 had one offs.

If we were to revert to the mean, what earnings power can be considered? Inviting everyone’s thoughts. Over the next 5 years, can the company maintain minimum 85 cr sales, 16 cr net profit, 2 rupees dividend and ROE of atleast 20pc?

1 Like

At the current price, PE and order book, the stock seems a hold.

Not sure if 143 cr will be actually executed. They underachieve topline and are able to come up with reasons to back it up. Either they underpromise and overdeliver or meet the guidance. The word of the management is becoming difficult to digest

Cupid is probably the only company where I can see the management commentary play out exactly in the numbers. There’s no mucking about. What they say is what you get. So I personally trust the management commentary a lot.

1 Like

Over the last few concalls, they’ve missed on the revenue & profit guidance and have reasons for the miss. The Q4 revenue was guided at 40+, fy19 was guided for 100.

Which part of the Management commentary u referring to that has played out exactly as guided?

Seeking answers doesn’t constitute mucking, this is a respectable management.

Can you show me any management commentary that was able to predict exactly how things would turn out? That too consistently? That doesn’t happen really.

The reasons they gave also show up in the numbers, is what I’m trying to say. So, it is very easy to follow the business this way. Remember, this newfound business model of Cupid has only been around for 2-3 years (After they won the WHO contracts). So, there is still a lot of learning curve left. The management’s thorough analysis of their own numbers allows me to travel right along.

That is what I feel. You are certainly entitled to take the management’s word with a bucket of salt, should you choose.

3 Likes

The bottomline is that unless the management delivers numbers, valuation won’t come thru. Notwithstanding reasons and hindsight analyses, it is performance that is crucial.

There are Managements that have delivered the guidance given in concalls.

It’s high time that cupid delivers on topline and gets in a new CEO, else it’s better to get acquired at this point in time.

1 Like

I think we have to realize that Cupid operates in an industry where revenue cannot be easily predicted. When they say order book that does not necessarily mean a firm commitment to purchase. Its more of a “client intention” to purchase. Mr Garg indicated that client has the freedom to delay purchases or move it from one quarter to the next etc. This is what makes it hard to predict, even for management, what numbers they will produce in any given quarter.

I don’t think this is management’s fault, its just the nature of the business they are in. If investors want a predictable topline business then they shouldn’t invest in Cupid.

One could argue that Cupid should probably stop giving such guidance given the nature of the business, but the nature of capital markets is such that investors and shareholders want guidance.

3 Likes

The item on which duty has been increased also includes condoms. This can be the break Cupid needs to enter US markets.

Can entry to US will be costly

Concall Transcript

I still don’t understand how they expect to make lower margins next year with an order book of 83 cr FC and 60 cr MC order book. For FY 19 the split between FC and MC was 40% and 60%. Quite strange.

They don’t expect to make lower Margins. The mentioned figures indicate a ~17-18% PAT Margin.

The split for the next FY is likely to be 50:50, as mentioned in the Concall.

The reason for Margins remaining flat is likely the additional expenses being made on marketing in US. These expenses are unlikely to generate Revenues until 2020-21.

2 Likes

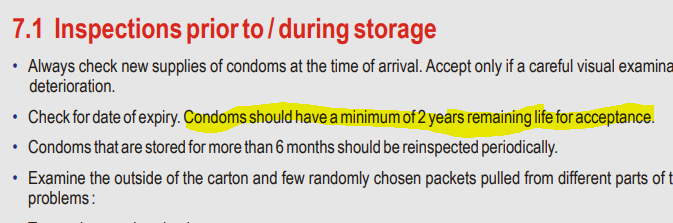

Regarding the write-off of 3 crore they have done due to expired batch.

I was checking the expiry period on packing for some other brands, for most of them the difference in Date of Manufacture to Date of Expiry is greater than 3 years. (Of course quite a few only have just date of expiry mentioned on them). But the once on which the Date of manufacture also mention the expiry period is 3 years.

Are cupid using some other raw material whose expiry is just 1 year?

If this is the case they have to be extra conscious about there inventory all the time. Plus the sale+delivery+usage time should also not go above 1 year.

Secondly as a customer if i get a preference to choose from 1 year vs 3 years expiry product. I will certainly go with 3 years product.

That’s a very good question. Someone can either write to the CS or ask it in the next concall.

My guess is that GOI is just that strict with categorizing expired condoms. Here’s a document I found from the National AIDS Control Organization:

So assuming Cupid condoms indeed have a life of 3 years, GOI would stop accepting them within a year itself.

1 Like

Valid & logical but raises another concern that why they couldn’t sell it via other mediums, I understand that all mode of sale shouldn’t have similar restriction.

I recall that this question was raised in concall but I was not convinced with management reply. (Please refer page 10 of transcript)