Please suggest these in the AGM. M pretty sure the management would’ve thought thru this.

Veru, the global FC2 company, got 75% of the South African FC order. Negative for Cupid.

What is the source of information brother

However, this was already discussed in the latest Concall. Well, at least it was hinted that Cupid would get around 20-22% of the order, with some additional order possibilities once the JV is setup (Wherein it was specifically stated that the SA Govt has promised to take up the entire capacity of the JV, which is planned to be around 16 mn).

1 Like

So some quick questions:

- Is Veru the same company that bagged the most of the first year’s orders? i.e.FHC? Or veru sprung a surprise as an unexpected bagger?

If veru isn’t fhc and the 40 mn order was finalized between fhc, cupid and HLL, then how come veru bagged 75% of the total order? The remaining order was 80 MN pieces which is 67% of the total. So in this case, veru can bag at most 67%, unless any part of the first year’s order was retendered.

- I thought that total imports = 80 MN and JV = 40 mn (meaning 67% imports and 33% JV). Veru bagging 75% of the orders meaning 90 mn pieces? So is it that the JV share is down now?

Overall Tender is for Up to 120 Million Female Condoms Over Three Years

Veru awarded Up to 29.8 Million FC2 Female Condoms of 40 Million Total for First Year

Overall looks nothing lost for Cupid & we are on track for 100 Cr top line this year

1 Like

Veru Healthcare and FHC(O) are the same. There are only 4 players in the global B2G2C Contraceptives market - Cupid, FHC, HLL and a Chinese player.

Last year’s order book was 63 Cr. This quarter saw a dispatch of 17 Cr worth of orders. Along with the new order of 40 Cr from the JV and 9 Cr (The remaining 22% allocation apart from FHC’s 75%), the current order book stands at 95 Cr. How much of this will be executed remains to be seen. This is only for the first tranhce (40 Cr) of the 120 Cr requirement for 3 years. The remaining (80 Cr) requirement isn’t allocated yet. According to the concall, Cupid is expecting a bigger piece of the pie for the latter allocations.

A 10% growth in topline from last year would demand Cupid to execute an average of around ~24 Cr for the remaining quarters in the year (or) 75% of the current order book (Which sounds a little steep in my opinion).

Assuming that the JV executes the production of 16 mn, at an average rate of Rs. 20 (Say), Cupid will be privy to ~16 Cr worth of Revenues (16 * 20 * 49% / 10), although this will come by way of Capital Appreciation, rather than an actual increase in topline. I’d be interested in understanding how Cupid Values the JV in its books.

The JV has not begun operations as yet. However, once it does, Cupid will get a one-time payment from the JV for import of raw materials from India (Cupid’s unused raw material, that is). This could also help a little with the topline this year. After that, Cupid will only benefit via the Capital Appreciation of its 49% stake in the JV and a small (5%) royalty payment every year. The positive here being, the SA government has promised to take up almost all the production done by the JV and this could possibly be a medium-term to long-term (As of now, 5 year) engagement.

TLDR: The news of FHC winning 75% of the first tranche has no bearing on Cupid, at least to the extent that it’s already been discussed by the management.

3 Likes

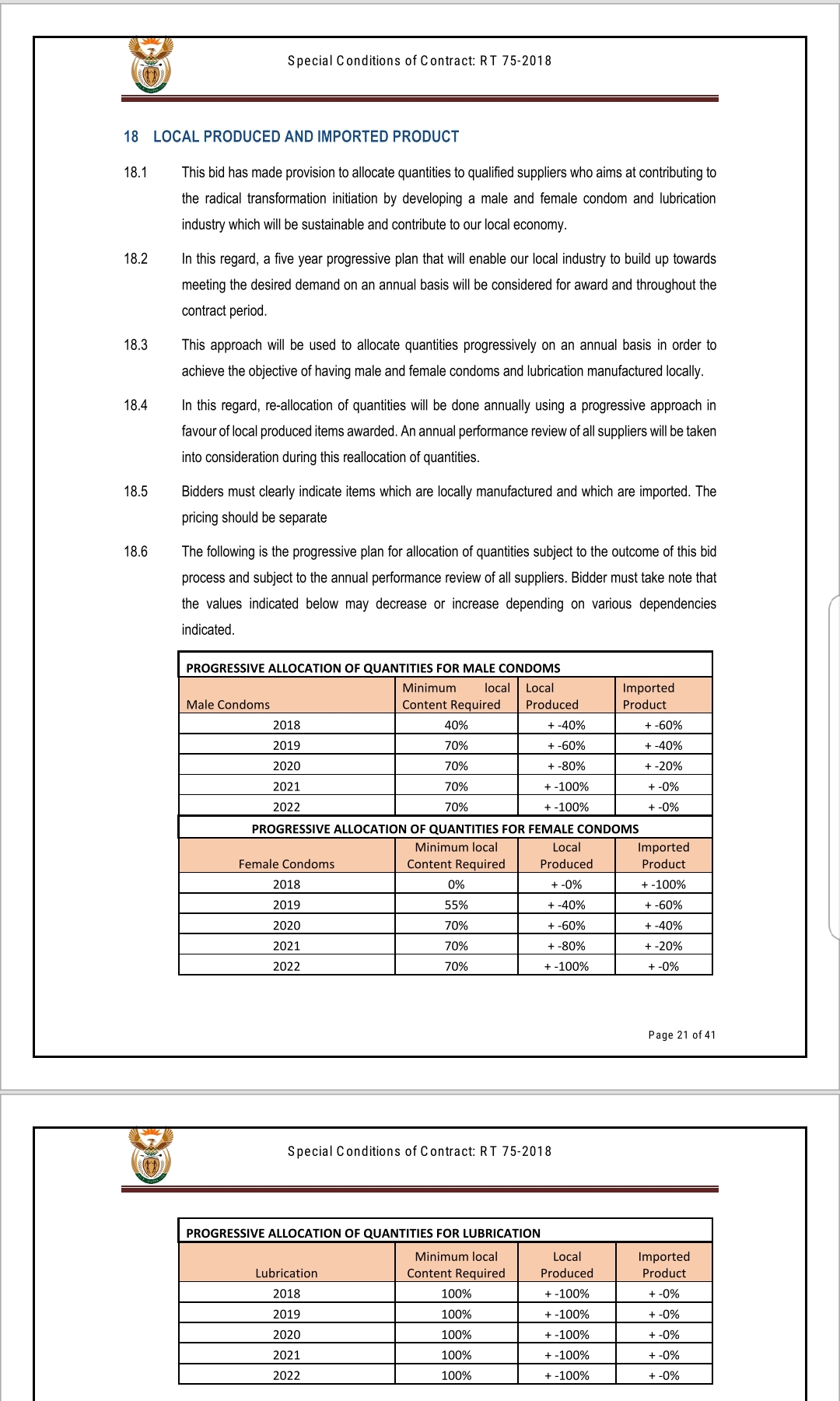

please share the url to that tender image bro @hnk_so

Going by the image you shared,

For the female condoms,60% will be local produced in 2019 80% will be local produced in 2020 and 100% will be local produced in 2021 and 2022 which is a great news for Cupid JV

For male condoms and lubricants,I think there are local producers already I believe

Pls correct me if I am wrong @dineshssairam sir

True, but the other players will also try to get into a similar arrangement (A JV or a full-blow manufacturing plant) in SA. There’s no free lunch. We’ll have to wait and see if Cupid has some kind of counter-measure for this. Currently, the only way I see Cupid doing this is by executing the present JV orders skillfully and at attractive margins to the government.

I’m more interested in how the company approaches other markets like India, US and Europe (Still no update on how the Cupid Angel line is working out in Europe so far).

What I really admired is Cupid’s swiftness in responding to the adverse situation (SA government wanting to produce Condoms locally). I just hope the new CEO is just as good as Mr. Garg.

2 Likes

Yes Sir ,execution will remain the key in the JV.

Going by the tender numbers,it seems Female condoms is mostly limited to 2 companies this time(FHC and Cupid). If FHC will also be involved in a joint venture with SA government, I believe then allocation would have been 50 -50 between Cupid and FHC for this year rather than 20-80 ,unless FHC is doing business at lower margin with SA government (assuming that Condoms manufactured by both companies are of same quality). Hence I am hoping it is a joint venture with Cupid alone.Thinking Greedy may be

However major re rating will happen only once B2C market opens up ,which remains a long shot

While going trough Annual Report, I came through some interesting notes

- Cupid received the contract worth INR 40.09 Cr during August, 2018 from South African Treasury Department through our agents situated in South Africa for supply of Male condoms (worth 23.80 Cr) and Female condoms (worth 16.29 Cr) during the period from October 2018 to September 2019.

It means that we may get approx 20 Cr in current FY (till Mar’19) & balance 20 Cr in FY 19-20

- On the positive side, in addition to fulfilling several repeat orders from our existing customers from various countries, the Company received new orders from WHO/UNFPA covering new geographies and two new contract manufacturing orders from the Domestic market. Despite the significant cut backs in the South African demand for Female Condoms, we increased our sales into new Geographies like Central African Republic, Guatemala, Honduras, Jordan, Tajikistan, Morocco, Tanzania & Uzbekistan. As on Mar 31st, 2018, we have confirmed and repeat order worth 630 mn to be executed during this year. This does not include any potential orders Cupid may get from the South African and the Government of India tenders.

Expected topline could be 63 Cr (order in hand as of 31 Mar 2018) + 20 Cr (taking 50% possible delivery in FY 18-19 + any potential orders in next 2 quarters

- Water based jelly is just 4% of total revenue

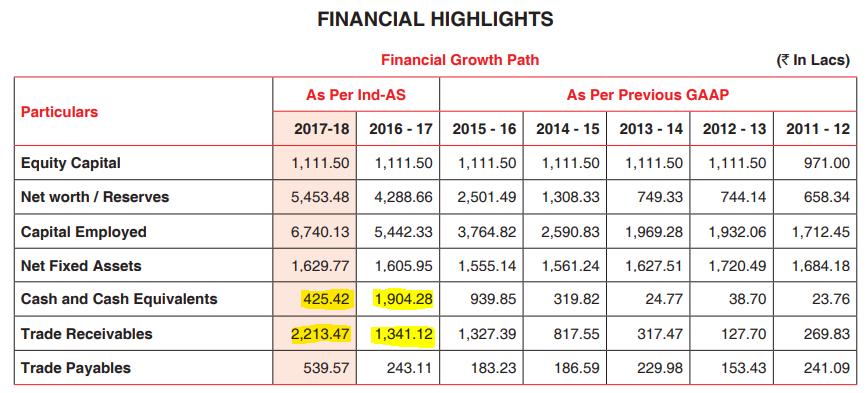

- While going through financial highlights, we can see that “Cash & Cash Equivalents” is down by approx 14.78 Cr, even if we club it with “Trade Receivables” only 8.72 Cr ets adjusted leaving a whopping gap of 6.06 Cr.

Request guidance from finance experts

Cash is down becoz they’ve parked the cash into investments. There is working capital borrowing probably becoz of that.

You may refer the cash flow statement.

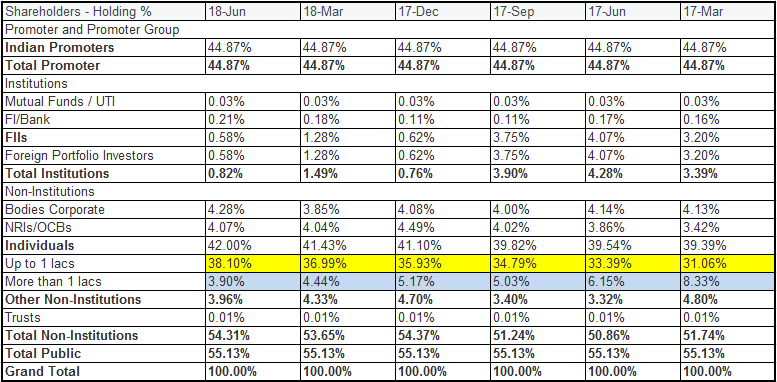

Dushyant Poddar, institutions like Elara and others exited/ pared holdings. They seem to have sold when the stock was priced in the 300-400 range.

Are we missing something that they saw? I think only one institution was a net purchaser.

Looks you have hit the nail as big individuals (more than 1 Lacs) have reduced their holding from 8.33% to 3.9% in last 6 quarters and again the small investors seem to have got trapped (almost 7% increase in holdings)

The reason may be Q3 & Q4 of FY 2017-18 had lot of challenges & trouble as mentioned by management in annual report. I suspect big guys could sense it which we missed. Now once again things are improving with bright chances of hitting approx 95 Cr - 100 Cr topline in current FY

M not put off by the exits. Just want to keep knowing if things r on the right track. Institutions and money managers are under constant pressure to perform, so they can’t afford to wait during challenging times, they have to exit and switch to other stocks that keep their performance look good

CEO appointment, capacity expansion, scaling up sales and efficient capital allocation need to be top notch.

1 Like

Is anyone attending AGM of Cupid Ltd ?

Please update here about takeaway from AGM.

FDA Reduces Regulatory Burden for Female Condoms

Now Cupid can target US Market after necessary product certification.

More detail on new law from US FDA at : https://www.regulations.gov/document?D=FDA-2017-N-6538-0080

7 Likes