I recall the Ceo mentioning that millions of dollars were required to fund the FDA trials.

So I think a part of this figure might be used for this purpose too.

As per last concall, the USFDA approvals would need upto 15/20cr. Clinical trials itself cost 2 mil. This would be needed over the period of 2 yrs. My guess is that the additional money would be for acquisition. Let’s hear that from management during concall whenever it gets scheduled.

I do have following additional questions, putting it across so that we can collaborate and ask questions whoever gets opportunity during con call.

- What do we plan to do with additional capital being raised?

- What is the progress on registration process with USFDA?

- B2C – what is the progress, when can we start recognizing sales. What is overall strategy, branding, distribution plan etc

- On Govt of South Africa order, how much of that is now remaining to be delivered in Q4 & fy18?

- Regarding repeat order from Govt of South Africa, we had following update from earlier conf call.

We have several round of meeting. Their deadline is Dec 17. June 18 is current tender. They may increase by 40% more.

any further update on it? - During Jan to mar we expect more tenders to come out which would be for fy18/fy19. How is the tender pipeline looking and anything that we are winning from it?

Disc: Invested

1 Like

7.Other expenses is up substantially ( from 3.42 --> 5.67, nearly doubled). What is the nature of these expenses ( recurring/one time) & for what purposes( Marketing expense for setting up distribution network perhaps/Capacity expansion/USFDA trial etc) ?

- What is the management guidance/expectation on the Raw material(mainly latex/rubber) cost in the coming quarter?

- The Sales proportion of the newly introduced Lubricant Jelly is 10%. What is the management guidance for this product category ( Is it one-time or a repetitive in nature). What was the OPM for this ?

A Bulk deal has taken place yesterday where 66488 shares were bought at Rs 321.5/- by Mr Sanjay Katkar. Is he the same person who runs Quick Heals solutions… am not sure ?

Yes seems like the same guy

If he is the same Sanjay Katkar., then doesn’t this look funny :

“Selling your own company’s shares at a premium, to buy other company’s shares”

@RajeevJ have not heard any inputs from you on Cupid for quite sometime. Would love to hear if you have interacted with the management recently?

Another Warren Buffet in the making …

1 Like

Could be due to expenses incurred for promotion and survey during navaratri season. Just a guess.

Another interesting point I have,

Normally, the cupid management immediately announces the conf call with the investor community, i.e just after the quarterly results.

This time , they have specifically asked for some more time in the press release.

Something is definitely cooking here !!

I hope

-Maybe new ceo ?

- large new order ?

- acquisition ?

My point is , apart from a major development expected by the management, there is no logical reason why the investor conf call should be delayed indefinetely.

Hi Venkatesh,

No, have not had any recent interaction with the mgt. I do not have much to add to my posts of Jan 5th & 6th. I guess the next concall will happen only after the mgt. is in a position to share with us who the incoming institutional investors are & how exactly do the intend to use the funds that are coming in.

4 Likes

What a great thread and what learning! super really really enjoyed going through each of the 575 posts.

After going through , i have come to believe that Cupid has transitioned to a “Franchise”. In his 1991 letter WEB laid down his definition of franchise and i believe Cupid fits the bill. He says

An economic franchise arises from a product or service that:

(1) is needed or desired;

(2) is thought by its customers to have no close substitute and;

(3) is not subject to price regulation.

The existence of all three conditions will be demonstrated by a company’s ability to regularly price its product or service aggressively and thereby to earn high rates of return on capital.

-

There is no question that FC’s are needed

-

The YWCA (a global organization working for the empowerment, leadership and rights of women, young women and girls in more than 120 countries) says that “Female condoms remain the only tool for HIV prevention that women can initiate and control”. In other words - there is no substitute for a female condom especially when it comes to preventing HIV.

-

There are no price regulations.

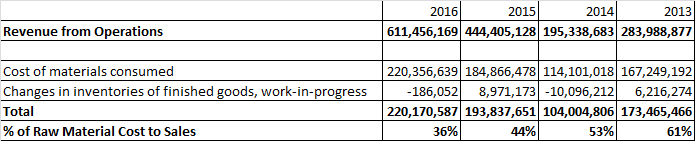

Cupid has managed to increase its price realization by a significant amount thereby demonstrating its capacity to raise prices. Its raw material cost (latex) was only 36% of its sales in 2016. In 2013, it was 61%. While latex raw material prices have come down to Rs 8455 per 100 kg in March 16 from Rs 11,100 per 100 kg - translating to a drop of 24% ( source: http://rubberboard.org.in/rubberprice.asp?url=earlyrubberprice.asp). There is undeniable evidence that Cupid has managed to increase prices ( even if we price raw material cost to 2013 levels)

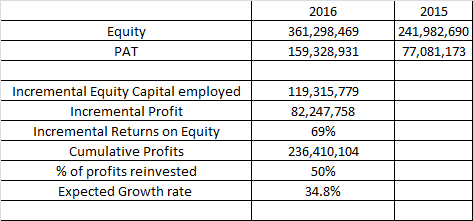

Over the last two stellar years 2015 & 2016, the company has managed to deploy an addn 11.9cr of equity producing an incremental profit of 8.2 cr. This translates to a superb incremental return on incremental equity of 69%. They have done this by reinvesting only 50% of the earnings. This means that the expected earnings growth rate going forward if they manage to keep up with this is a remarkable 34.8%.

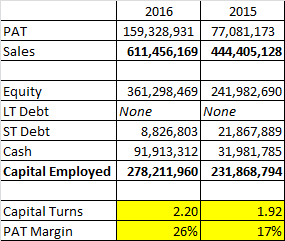

The company has improved its capital turns ( from 1.92 to 2.2 ) and the margins have expanded ( from 17% to 26% ). Both have improved substantially.

It seems to be that at a PE of ~18 the market is completely ignoring its growth prospects. Any growth over any period will lead to a rerating again. I am invested and obviously biased ( came to the party late , read through all the posts , stock corrected dramatically and offered me a chance to get on the bus full of happy investors )

12 Likes

And for those who are interested, here is the original patent granted in 1989 ( filed for in 1982 ) for the invention of the female condom to its inventor Henry J. Lee. FC’s were invented 35 years ago !

US4840624.pdf (262.3 KB)

2 Likes

BOB capital Viewpoint:

https://www.bobcapitalmarkets.com/getreport.asp?id=194

4 Likes

Good to see BoB following up on their initial coverage on Cupid which was in Aug 2015. BoB was perhaps the first institution to recommend a buy after which there was a 100% jump in the prices!

Order book indeed looks very healthy. It’s only a matter of time before a strong re-rating sets in. More visibility in order pipeline through long-term contracts would do the trick

While I love the financial ratios and growth figures of this company, what I worry the most is this - one man (Owner) show , one product (FC) company. Any “Black Swan” event can deal a severe blow to this company. So personally I feel risks are far outweighing the upside potential (maybe after reading Howard Marks memos)

Disclosure - exited all my positions after news of equity dilution.

1 Like

The Gates foundation is out with their annual letter ( 14/02/2017 ). This year they have written to Warren Buffet -

Scrolling to page 8 i found this ( highlights are mine )

The most hard hitting statement is

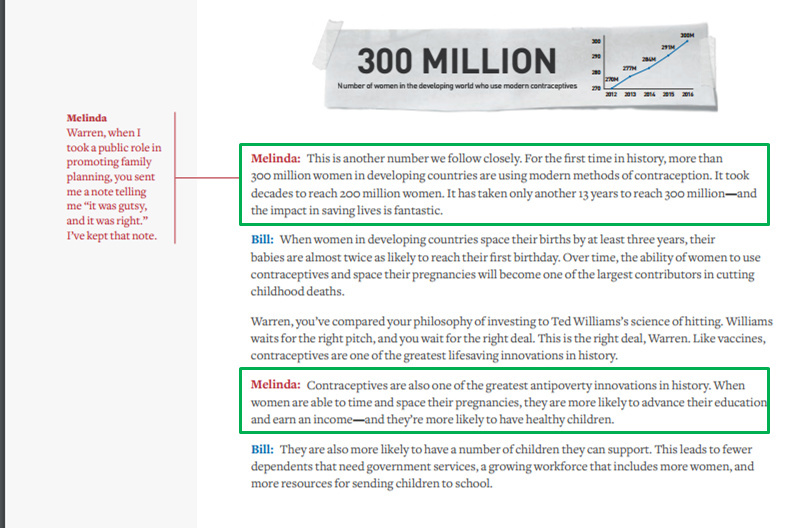

No country in the last 50 years has emerged from poverty without expanding access to contraceptives

"There are still more than 225 million women in the developing world who dont want to get pregnant but dont have access to contraceptives"

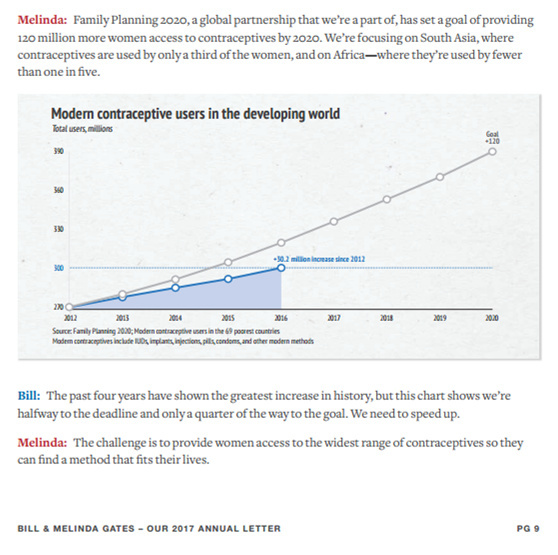

Melinda: Family Planning 2020, a global partnership that we’re a part of, has set a goal of providing 120 million more women access to contraceptives by 2020. We’re focusing on South Asia, where contraceptives are used by only a third of the women, and on Africa—where they’re used by fewer than one in five.

225 mil + 120 mil - 30 mil = 315 mil ( Additional size of opportunity in front of players in the contraceptive industry )

You can view the letter at 2017AnnualLetter-EN.pdf (1.7 MB)

Happy investing!

29 Likes

Dear fellow investors,

In FY17 Q3 press release the company has mentioned that they have pending order worth Rs. 729 mil.

This should last for about one year approximately.

**But what is the future of the company after completing this order? **

Are there chances/hints of repeat order?

Sincerely,

Django.

Thanks for bringing up the elephant in the room.

In my humble opinion, this is exactly why the market is not ready to pay more for Cupid. Unless Cupid shows strong visibility on the orders there is no way it is going to be lapped up by FIIs and DIIs. What Cupid needs now (all the more than ever before) is a HUGE order to be executed over a 2/3 year period and then we will have a re-rating

If not the market will wait and watch over a 1 year / 2 year period to see and evaluate these repeat orders which will keep coming in bits and pieces… just enough to justify current valuations

1 Like