Equity dilution is a matter of concern as it will reduce EPS in the short run. If additional money is indeed for acquisition, then I think it is risk since current leadership has very less bandwidth. So unless they find capable CEO to take care of day to day operations, acquiring (and merging) other business would be big challenge for small company like Cupid.

In long run, it may become winning move but I am seeing lot of short term (1-2 years) challenges for the equity dilution route undertaken by the promoters.

it is not hidden. There is an octagonal ring which keeps the condom from going inside completely by accident. It is the core design which is patented by Cupid. One of the competitors has a hexagonal ring I think.

Secondly even our own discussions with management confirmed that in Africa sales via direct retail channel are negligible, and it is all institutional. So promoting retail in places where the product is fairly well known has proved challenging.

Retail condom sales will require significant marketing expenses and I have my reservations if those expenses can really generate profits as has proved with skore and manforce, both have tremendous distribution presence.

@Rahulj I understand that Retail condoms market is highly competitive mainly because its eventually like a commodity and only differentiation which can be added is minor changes to the design to improve experience.

But correct me if I am wrong, one you are trying to compare male condoms market with the female condoms one. Two you are trying to compare the loss due to operations which could be due to a number of other factors like supply chain inefficiency, pricing errors, bad use of marketing budget, labor costs etc. If Manforce is losing money with Sunny Leone they could have looked at other marketing options with better marketing ROI.

For any business, facing hostile conditions and stiff competition is common especially in a commodity business. But that doesn’t mean they do not choose to launch a new product or try a new channel. For all the things which you mentioned the company needs to be more cognizant of the marketing spend, track the marketing ROI closely and enter into the business with an easy exit option. (Be asset light).

According to me, branding and marketing is a great way to create a barrier for entry for new market entrants. And considering the position Cupid is in right now this seems to be the right time. They are trying to create something similar to what Xerox did to photo copier industry. They are early movers in a particular segment and they are trying to make the best use of it by getting brand recognition for the product. Competitor failure is a great learning but not a measure of their success or future outcome. I really like the fact that Cupid went in with the “For her” campaign and is trying to educate the consumers to improve adoption rather than flashing high paid models expecting people to relate it to something they are aware of. Fingers crossed. I think it’s a gamble which if pays could work wonders allowing the company to introduce more variants of the product with minor design modifications for better margins both in domestic and international markets. If not they are running at full capacity and would continue to do so with only the marketing expense as sunk capital cost.

Not really sure of where they would price and whom would they really target. Considering the facts you mentioned I would assume they would run pilots in small geographies for understanding the market, rather going in with big bang push with high inventory off shelves of the distributors, high distribution logistics costs and big marketing spend. Completely opposite to what others are doing. But it’s a wait and watch game. Personally, I think the risk is lower than the reward potential but I may turn out to be wrong.

You are assuming that manforce is making losses because it is not selling. But the fact is it is the top selling premium condom. The distribution of mankind is humongous and manforce is less than 1% of total sales, every corner of the country you can get manforce.

A female condom is not going to compete with female condoms but with male condoms and pills especially. The use of a female condom is complicated as well. Cupid has no experience of retail. They had tried retail in the past and went into a debt trap which they got out in 2014. Current management has very little bandwidth and from what I understand, the promoters kids are not interested in the business.

Cupid has been looking for buyers for the promoters stake for the last 6-8 months. But they have not been able to find ányone because most indian and international condom makers are sitting on huge capacities and are not interested.

The machinery that cupid uses to make condoms cannot be used for making products other than balloons or surgical gloves, which are again very competitive products, will not be value accretive (cupid did try them in the past).

What I am trying to say is retail female condoms business is something they are showcasing to potential buyers and not really interested to make money. They need to show where the potential growth is going to come from, so far they havent been able to.

Let me ask you a bit silly question. its more for my knowledge purpose. Cupids balance sheet for fy 16 mentions total share capital as 11.12 cr

Lets assume that the promoter wants to increase it to 20 cr.

From where will the promoter obtain the additional 8.78 crores , to increase from 11.12 – 20 cr ?

Will it be taken out from the company`s cash reserve ?

Also, apart from the EPS going down proportionally , what other impacts might there be on the balance sheet ?

share capital is 11.12 cr. Now to increase the share capital, company will have to issue new shares. This can be done in multiple ways. One is issue bonus shares to existing shareholders, what happen is share capital goes up and securities premium/ P&L balance account goes down. Net effect is zero, so no change is cash balance remains the same.

Other is issue new shares (qip, rights, fpo etc)… Then securities premium will go up as well as share capital. A proportionate rise in cash balance will occur.

Cupid mgt. has decided to raise funds not exceeding 60 Crs. As per the SEBI formula, the pricing of the issue will be at a minimum of Rs. 300 per share (could be higher). From the looks of it, it will most probably be a QIP which is very good news for the Cupid share holders as it means that Cupid will, in all probability, finally have some institutional share holding. These big guys usually have a more long term view of about three to five years. They would also have satisfied themselves about the viability of the expansion plans. What these expansion plans really are, would only be known in due course, but the Cupid mgt. is conservative & would not be willing to compromise on profitability / margins.

While the authorized capital is being raised to 16 crores, the paid up capital will be raised only to the extent of the dilution. In this case, not more than 2 crores so the move to raise the authorized capital to 16 crores should be seen more as an enabling provision. Yes, the paid up capital would go up to about 13 crs from 11.12 crs currently, but the Co. would receive about 60 crores, the returns/ benefits of which will accrue to all the shareholders.

The key is to figure out what the company will do with the money raised. The EGM Notice mentions the following:

“The Company requires adequate capital for expansion/ diversification of business. The Company is in requirement of fund to meet capital expenditure, R&D expenditures, cost of overseas registration, brand promotion, working capital requirements and other general corporate purposes as permitted under applicable laws. While it is expected that the internal generation of funds would partially finance the need for capital, it is thought prudent, it is thought prudent to have enabling approvals to raise further funds for the said purposes as well as for such other corporate purposes as may be permitted as may be permitted under applicable laws through the issue of appropriate securities as defined in the resolution.”

Q3 RESULTS came in at 8.15 AM today morning. SUPER STRONG performance, at first glance.

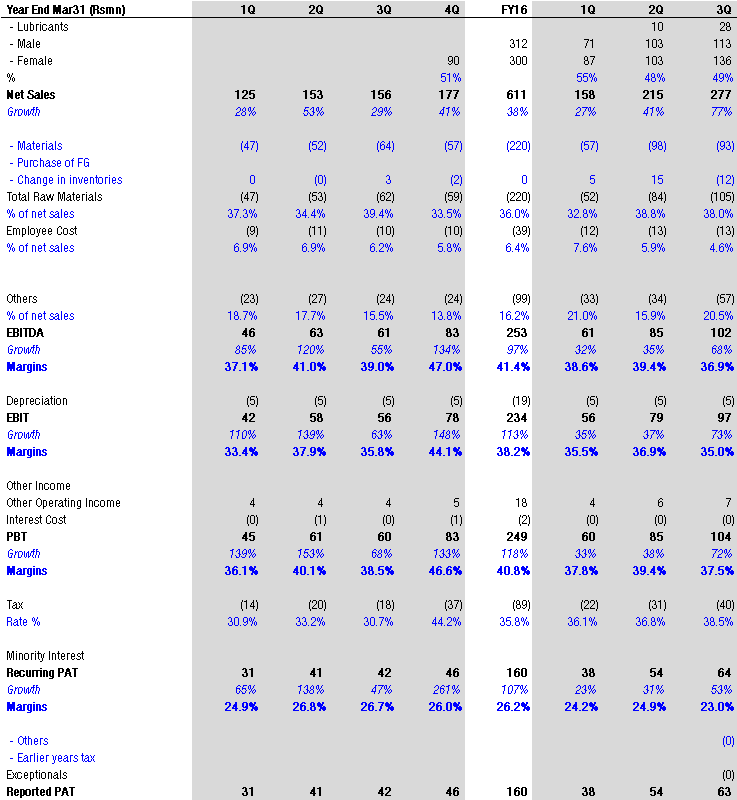

Q3FY17 Review (October 1st, 2016 to December 31st, 2016) Total Operating income was ₹283.76million (mn) for Q3FY17 as compared to ₹160.48mn in the

corresponding period of the previous year reflecting an increase of 77% EBITDA stood at ₹109.07mn as compared to ₹65.21 mn during the corresponding period of previous

year, an increase of 67% EBITDA Margin at 38.4% for Q3FY17 as against 40.6% in Q3FY16. Net profit stood at ₹64.21mn for Q3FY17 as compared to ₹41.95mn in the corresponding period of the

previous year, an increase of 53% Basic EPS stood at ₹5.78 as against ₹3.77 in the corresponding quarter of last fiscal.

Great results , however , management has a cautionary statement on future quarters in b2b side .overall great results n mgmt proactively taking griwth steps. Utilization rate more than 90 percent

Indeed, the management commentary is cautious .

However, it is notable that the lubricant jelly section is now 10% of the total executed orders for this quarter.

Would be interesting how it scales up in the future.

I just wonder what is the need to raise Rs60crs through a QIP. The gross block of the company is 36crs. So cant you double capacity in less than 40crs?

Total Operating income was ₹283.76million (mn) for Q3FY17 as compared to ₹160.48mn in the

Total Operating income was ₹283.76million (mn) for Q3FY17 as compared to ₹160.48mn in the