I think what Mr. Garg mentioned that second half sales would be at least equal to first half. So I think annual sales would be around 80 Crores

I met a senior person in the condoms business recently and he said women’s contraceptives is a fast growing market given concerns on premarital sex, one night flings etc. and he said it would take 2-3 years to get approvals and start exporting and most guys in India have missed this because of the lack of cultural understanding. He also said this is a white space globally and this could lead to acquisitions in the future. seems like cupid has a decent moat -

discl invested at an avg price of 240-250. no transactions in the last 3 months.

11 Likes

Cupid Conference call transcript of Q2 FY 2017

1 Like

Will GST have any kind of impact on Margins ?

Cupid:

Business:

Cupid, an Indian Public Limited company headquartered in Nashik (India), manufactures male, female condoms and Lubricant Jelly. It supplies condoms on contract for other brand and has its own brand.

It’s 20% of revenue come from the Contract manufacturing and 80% from the own brands. Both Male and Female condoms contribute 50% each to the revenue. Lubricant Jelly is a new product launched last year. Its customers include both Individuals and NGOs like UNFPA, WHO, NDOH (South Africa), etc.

Company is having the marketing offices in Delhi, Mumbai and New York marketing its products to 26 countries including South African and Sub-Saharan Countries where 70% of HIV population lives. Exports contribute to 77% of revenue out of which South Africa and sub-Saharan countries have a major share. Female Condoms biggest customers are Institutional customers & Female Condoms have higher margin than Male condoms. Cupid is the first company in India and the second one in the World to have been prequalified by WHO/UNFPA for worldwide public distribution of female condoms

Past Numbers:

- Growth in Op. Earnings/ Diluted Shares - 46%

- ROIC (Op. Income/ Avg. IC) - 69%

- Growth in FCF/ Diluted Shares - 45%

- FCF/IC - 37%

- Growth in Book value/ Diluted Shares - 38%

- Liabilities/ Equity - 34%

- Growth in Tangible Book/ Diluted Shares - 37%

- Debt/ Equity - 2%

Strategic Analysis of Future Performance:

1. Four Forces:

1. Threat of new entrant - Medium - It is difficult for new entrants to develop their own products and to get it qualified by Local and International bodies. Moreover, female condom is a patented product.

2. Bargain power of buyers - Low - Since the company manufactures niche products and people would get used to the product (habit forming demand side moat), they would pay an extra cent for the product they like. (Especially for female condoms). But for the past two years, the receivables are on increasing trend; probably to establish and strengthen the institutional customer’s relationship, they might have increased the sales in credit. Anyways the institutional customers are renowned organizations. However, they have balanced that increase in receivables with reduction in the inventory to stabilize the net trade cycle.

3. Threat of substitutes - Low - Unlikely to dislodge these products from the market. Although other methods of contraceptive methods have come, condoms will continue to be the prime choice for the customers to prevent unintended pregnancies or Sexually transmitted disease.

4. Bargain power of Suppliers - Low - Company might get many suppliers to supply the raw materials for their products. Days Payables is on increasing trend (always greater than the inventory), suggests that the company can delay the payment to the suppliers, thereby maintaining a negative net trade cycle. This prevents the company from borrowing for working capital, which results in high ROIC.

2. Breadth Analysis:

The Customer/Supplier Base is unlikely to consolidate. Moreover the company is expanding its geographical areas.

3. Moat Identification:

Sources of Moat:

Ingrainedness - Female Condom is manufactured by only 4 companies worldwide. This company has become an integral part of value chain when it comes to female condoms.

Supply side moat - Female condom is patented (pending) and pre-qualified by the UNFPA and WHO.

Capacity Utilization improved from 52% in FY14-15 to 64% in FY15-16. This increases the asset turnover too. There will not be Capex requirement in the near future.

Cupid plans to enter new Geographies: South America, Eastern Europe and CIS countries and add new products and increase the Brand promotion. This could probably contribute to the topline.

Market Growth Assessment:

Global contraceptives market size is poised to touch USD 33.6 billion in revenue by 2023. Market is currently estimated at USD 19.8 billion and is projected to increase at 6.8% CAGR over the coming years. It is estimated that the global market for male condoms would touch USD 9.3 billion by the year 2020. While the male condoms market would demonstrate a growth from annual 27 billion units to 42 billion units, the female condom market would also expand from the current annual 100 million units to about 340 million units by 2020.

Shareholder Friendly:

- Dividends - 20% healthy dividend payout

- Buybacks - No

- Reasonable Compensation to management

1. Chairman & Managing Director - INR 6 Million per year + Commission of 1% Net profit of the Company

2. Other Directors - INR 0.3 Million

3. Other key Personnel other than Managing Director = INR 0.78 Million

All these remunerations are below the ceiling set by the Companies Act, 2013. This is the first year Chairman is getting remuneration, until previous year he didn’t get any remuneration.

4. Avoiding Related party Transactions within the Management. - Loans with promoter group.

Points of concern:

-

Too much dependence on the institutional orders like Government of India, UNFPA, NDOH South Africa etc. We cannot assume that the company will get same revenue (or repeated orders) from these clients. In FY 2013-14, revenue reduced because it didn’t receive the orders from GOI, New Delhi.

-

Company formed a subsidiary “Cupid Medical” in 2013 and ceased in 2015. No big revenue push from this subsidiary. Why this was formed?

-

Company lends Loans to too many people in the promoter group in the past.

-

Company invested in Arihantsidh Properties pvt Ltd as Non-Current Investment for Rs 24 Lakhs. Also it mentioned the investment value got diminished by Rs 18 Lakhs, leaving the net investment to Rs 6 Lakhs. What is this investment? Why is it reducing in the value?

-

In the past, company issued warrants to fund its working capital, till the introduction of Female condoms.

-

Till the introduction of the female condoms in 2012-13, company was struggling without any significant movements. Female condom was the savior of the company. But still the company supplies the female condoms predominantly to the institutional customers like NGOs. How long the company can depend on the business with the NGOs is the question, an investor must try to figure out. (Note: Female condoms contribute to half of the revenue with good margins)

Disc: Not Invested

1 Like

Cupid looking for licensing of design patents from a third party.

Probably, it hopes to gather more footprint by using better accepted / hybrid products in the global market.

Its high time now the company gets some substantial orders for FC., before more competition steps in.

4 Likes

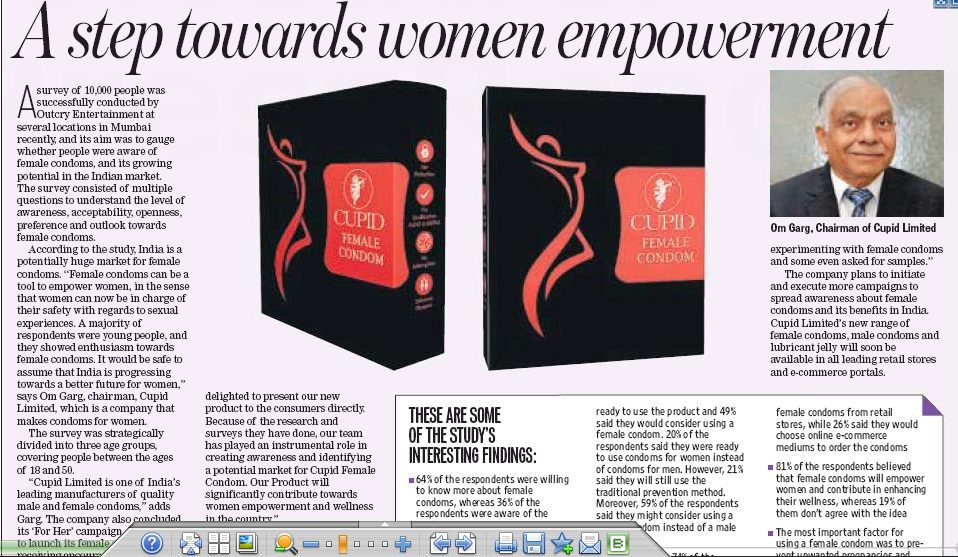

Cupid planing for a retail launch of their products in India.Good to see that the company is educating and expanding market with their campaign.

Disclosure: holding a tracking position

1 Like

I saw half page ads of “For Her” campaign in mid-day english (mumbai) and hindustan times HT cafe supplement.

5 Likes

Cupid’s stated intention for foraying into the retail segment , along with fund raising via issue of securities, seems a bullish signal from the management.

Might this be a strategic shift away from government tenders ?

Or is the company gearing up for some acquisitions ?

[http://www.bseindia.com/corporates/anndet_new.aspx?newsid=92cc0e30-8daa-4cf7-a8ab-355105c4b830](http://www.bseindia.com/corporates/anndet_new.aspx?newsid=92cc0e30-8daa-4cf7-a8ab-355105c4b830)

1 Like

Your guess is as good as mine.let’s wait and see.

how should one look in to the announcement , may there could be equity dilution, dont understand y they are going that root , as it FCF BUSINESS generating 20cr

In response to some query, Management had mentioned sometime back that they may go for an acquisition…if they don’t find any worthy one, they would increase dividend out of Rs 20/- earned(currently Rs 4/- approx. is dividend). from the latest happening, it could be that they have decided to go on for acquisition.

what about dilution, and i also feel right now its a one trick pony company , as female condom saving grace for the company

Retail condoms business is very competitive and not really value accretive. We recently met ttk management and they are losing money for last three years. Durex took away the contract and they had huge capacities and they have lots of losses due to high op leverage.

They said that even manforce is losing money and it is because of two reasons, manforce gets its products from china and just distributes it. But the cost of advertising using Sunny Leone is too much.

Manforce is one of the best at distribution and you can find the condoms i every corner of the country because of the expert distribution of mankind.

The retail confom business is not value accretive unless you are at the premium end or you have the volumes at the mass market end. Cupid has neither which even cupid management agreed. I am surprised they are really foraying into retail at this moment

8 Likes

@Rahulj I think this is valid for male condoms where as cupid is launching female condoms in retain market. Are you sure the above statement is valid for B2C female condoms too?

B2C retail female condoms is yet to see much traction because it is a very new product. My view is that there is no clear cut target market here. Who will use it? A typical housewive uses pills. Youngsters use male condoms.

Why would a girl or a woman use female condom? From our discussion with management a typical male in africa is not always happy to wear condoms. Females and sex workers insist on using a female condom to safeguard themselves.

Will a typical india sex worker use it at say 25 bucks a piece, i have my doubts. Will other kids use it again i have my doubts,. So i dont think it is going to be a big game changer

2 Likes

@Cupid shareholders,

Considering the fact karex is making 5bn pieces, cupid is way behind.

Any idea why they haven’t yet ventured into other geographies (US, UK) with their own brand (or) through contract manufacturing for male condom ?

Agree with you. I had spoken to few doctor friends about adaptability of female condoms cand they said it’s not as easy as using male condom n hence adaptability is a problem .currently , do not see potential beyond red light markets n tes their pricing can’t be premium but a change in technology leading to ease of use can do wonders

Much safer than pills. Males reluctant to wear condoms. Female condom is hidden, does not involve male partner’s wish. Educated girls will easily adapt once they come to know about female condoms. Right now even doctors don’t know about it. Need to create awareness both by cupid & government agencies

female condoms are not hidden…

Link

Admin: If the link is against the forum rules, kindly remove.

Disc: Invested