Some insight into the prospects of “pleasure industry” in India.

Disc: Interested but not invested.

Some insight into the prospects of “pleasure industry” in India.

Disc: Interested but not invested.

Great effort & post @Marathondreams

On the capacity utilisation bit, is the plant running at 3 shifts per day and still is at 100% utilisation, or is it 100% for the shifts (1 or 2) it is running?

when asked specifically about no. of shifts, I was told they are running 3 shifts… so that is 100%. But every manufacturing plant can go beyond “so called” 100% by doing tricks like working on weekend, running bottleneck operations not stop etc.

No , i did not ask the question about lubricant jelly.

Lubricant jelly is a very small business. We recently met Cupid and also visited their plant.

Jelly is ready to ship but some approval issues. Samples being tested or something. Said they expect dispatch in oct. Finished products are lying all over the place. Soon cupid will run out of storage space.

From the rough calculations, jelly price is 1.25-1.30 rupees per unit while cost around 65-70 paise. The jelly capacity is about 200 million units and they hope to see 85-90% utilization by Fy19.

They briefly told that they have th highest capacity in the world. Two machines, only one was operational.

The Navratri festival is being used by Cupid to promote the female condom. The Co. seems to have chosen the right target audience!!

Waiting patiently for a new order… it’s a raging bull market out there with so many stocks doubling. Will be perfect timing if Cupid can pull off a big order win.

In the last few months there has been only one order (which HLL bagged) quite contrary to expectations after the budgets have been approved.

This is my first post on this forum, so please excuse any amateurishness or mistakes. I have been reading this thread and looking into this company over the last few weeks. I had a few questions which have come up earlier in this thread, but wanted to ask once more to the senior investors on this forum to improve my knowledge and skills.

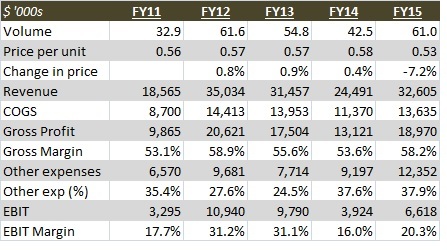

This is an industry which seems to be quite lumpy and growth is not smooth. See FHC numbers below - significant volatility over the last five years.

In addition, even the total volumes (ex-Brazil and USA) - I have approximated these by adding FHC volumes and Cupid volumes (interpolated to match the fiscal years) are flat to slightly declining.

How do we gain confidence on the UN projection of 3x volumes on FCs in 4 years, which is what we are basing all our forecasts on?

Given this lumpiness and variability yoy, shouldn’t the steady state multiple of this business be closer to 15x P/E rather than 20 or 25? This is almost like an EPC business after all, with order book being quite volatile.

Given the steady state margin projection of 35-43%, it will require FC sales of ~50 mm units to achieve a 3x increase in market cap over 5 years. Even if we were to assume the non-Brazil and USA market to triple, that assumes a 45% share for Cupid in these markets five years out. Can we confidently assume this?

4.Given that these are govt/multilateral aid agency tenders, one can assume that price increases would generally lead to volume declines. As a result, isn’t Cupid completely exposed to variations in latex prices?

As I said, please excuse any naive questions. Hoping to gain from the valuable experience of senior investors on this forum.

As far as industry volumes are concerned yes they are lumpy as sale is dependent on international aid and foreign governments. However, I don’t think the volumes are accurate as there are other players like HLL.

Cupid should still achieve 20% growth rates by entering new markets such as South America and USA. It has better margins than FHC and could capture a greater market share in the industry. It is also planning a B2C foray into India which could be a possible future growth driver.

Following is an excerpt from FHC’s Annual report

“The Cupid female condom became the second female condom design to successfully complete the WHO prequalification process in July 2012 and be cleared for purchase by U.N. agencies. FC2 has also been competing with other female condoms in markets that do not require either FDA approval or WHO prequalification. We have experienced increasing competition in the global public sector, and competitors

including Cupid received part of the last two South African tenders. Increasing competition in FC2’s markets may put pressure on pricing for FC2 or adversely affect sales of FC2, and some customers, particularly in the global public sector, may prioritize price over other features where FC2 may have an advantage. It is also possible that other female condoms may receive FDA approval or

complete the WHO prequalification process, which would increase competition from other female condoms in FC2’s markets.”

Information about “For Her” campaign

Cupid has come out with a great set of numbers for Q2. It is by far the best ever quarter, both in terms of Sales as well as profits. Great going!!

From growth in sales & profit perspective the quarterly numbers are outstanding.

However from order book position perspective concern remains. From 56cr order book, currently it is at 46cr which is after 22cr sales this quarter, implying just 12cr incremental addition this quarter. It will be interesting to understand management comments on this. Conf call today at 3 pm

HLL life care is a govt entity in kerala. It was among two companies to get unfpa approval for female condom few months back. It won its first international tender at INR 19 per female condom against realization of INR 25 for cupid. A sign of price war in future tenders and sizeable margin compression.

If it is true then with just 2 quarters orders in hand, the new orders run the risk of substantially low profits!

Hi @Ishank,

I think the management is just conservative about the order book. During last quarter conf call, I remember him hinting that there is a high probability of the previous large orders getting repeated.

So concluding that cupid has a low order book may not be fully right.

Regarding future competition & downward pressure on margins due to HLL, only time will tell…

Cupid is coming out with “Cupid-2” , which has better features( hopefully with higher margins).

order book as per recent release. if competition is selling at INR 6 lower, that takes away 1/3rd of Profits (as per my calculations). if the company has to win new orders, it will hv to bid at <19. large orders can come to it but at reduced profits.

cupid-2 is nothing but shorter in length than existing one, as populations in some parts of the world dont require existing size of condoms, as these are mainly for African market. Cupid-2 as mentioned by management in the last concall will be priced lower than cupid. so cant have higher margins.

Does any body have any idea abt the concall for Q2? Please share the details with us, if any.

The company will conduct a 60 minutes Earnings call at 3:00 PM IST today where

Mr. Om Garg(CMD) will discuss the company’s performance and answer

questions from participants. To participate in this conference call,

please dial the numbers provided below ten minutes ahead of the

scheduled start time. The dial-in number for this call is +91 22 3960 0644/+91 22 6746 4144.

Update from earnings call

All along company was publishing/disclosing only current FY order book numbers. Good to know long term details as well. However, would like to see how this multi year order book builds further to address full year capacity and sales run rate.

Other encouraging developments/plans/points from concall

Adding some more inputs from today’s call:

a) Out of 80cr govt of India tender they have done bid for 15 crore .They are expecting the approval/rejection of this bid within two weeks .Based on company current FY17 commitment for booked order they can only bid for 15 crore amount .

b) With existing cash of close to 17 crore they are looking for acquisition(ticket size 15 to 20 crore) or some organic growth by introducing new products .Mr Garg clearly told that he is not in favor of taking loan and doing big ticket size acquisition .He wants company to be debt free .

c) There are many orders which will auto renew in next financial year and will add to the existing order book of 40 crore .South African tender when they come for renewal in next financial year ,order book size will be 50% more than the order which they received last time .He seems quite confident of order renewal from south Africa .

d) New Lubricant jelly can contribute 7 crore to topline of Fy18 if they get enough order for it .For FY17 second half out of 46 crore pending order to execute, 2 crore contribution is from Lubricant jelly .

e) Q3 and Q4 result will be close to or better than what company delivered in Q2.

f) Many International NGOs tender bidding will happen in Q4 .

g) Currently they are at 90% capacity utilization .Capacity for female condoms can be increased from 20 million to 30 million in span of 2 months and from 20 to 40 million in span of 4 to 6 months .They will need capex of 3 crore to double there capacity .

h) They are also actively looking for outsourcing there male condom production if demand for it spikes .

Overall quite positive vibe came out from management commentary …I expect FY17 topline in between 85-90cr and EPS of entire year somewhere around 19 .