Dear @jitenp would like to know your thoughts on the Pharma Stocks. Seems a lot of effort has gone into addressing the ANDA issues. Also, many pharma cos are actively training their personnel on regulatory issues. Attaching a study by HDFC Sec. on the Pharma sctor.HDFCSec-Pharma.pdf (354.8 KB)

@jitenp, thanks a lot for your inputs. Do you track Causitc Soda cycle as well? If so, where is the current cycle at present? I see that the price of Caustic Soda is increasing. I’m holding Guj. Alaklies at higher price level and would like to seek your opinion as well to review how the cycle is playing?

Pharma as a sector is looked at more as a defensive, not a cyclical imho.

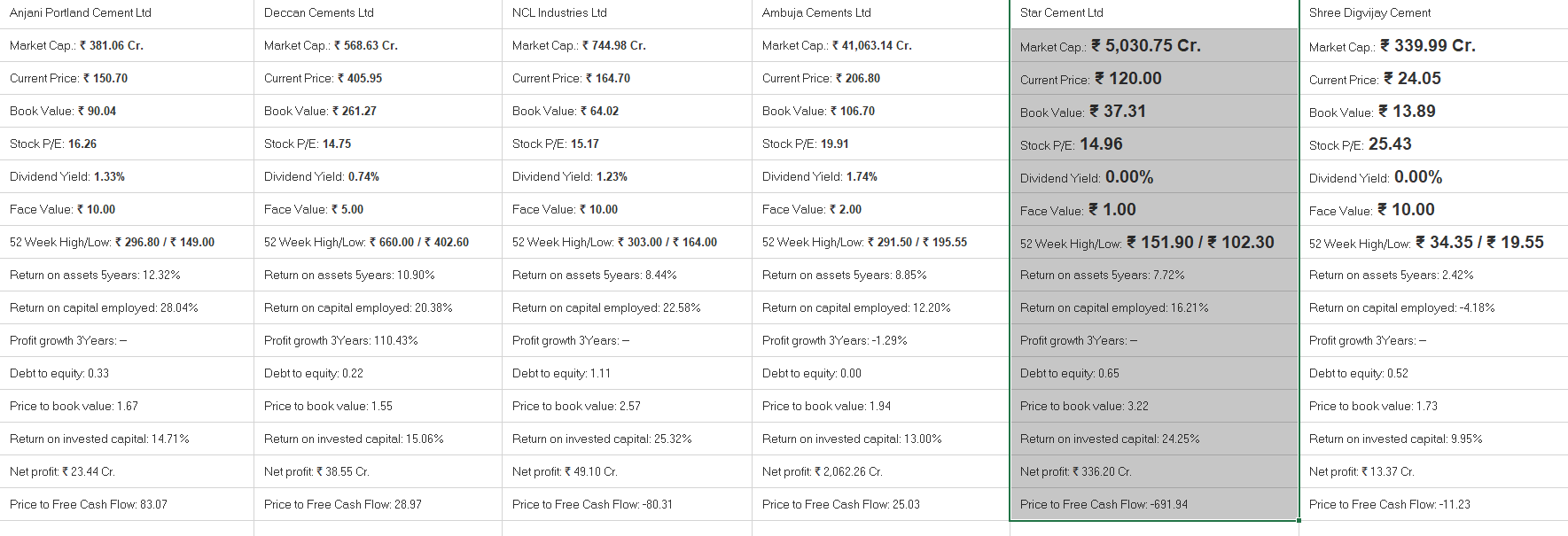

Cement cycle has it started ??? i don’t know

When it will be starting i don’t know ?

What will be the returns i don’t know …

but do i know what can be potential players may be Yes or NO pleaes advice in ref to the data below

My bets will be Anjani portland and Deccan Cements Ltd … need your valuable suggetion

Disc not started investin in cement stocks yet this is not any recomendation data source: screener

Bit baffled by what’s happening with Nalco.

Current price levels are at FY12 levels and also the tops of FY15 so its a very familiar, congested zone. A further breakdown from here should point to Aluminium cycle ending prematurely. Other than the Rusal drama and Trump trade war in general, nothing much has changed with the Aluminium cycle other than maybe a fear of global growth and/or fear of Chinese capacities dumping Aluminium in places other than US. This is reflected in the Aluminium prices which are down 12% from the top made during Rusal sanctions.

Coming to Nalco, its divergence with Hindalco is interesting. Today Hindalco was up 2% while Nalco was down 4%. This is pointing to expiry week volatility more than drastic deterioration in fundamentals.

Exports data for May is very positive (87% growth) with Aluminium exports at all-time high and so is the price realisation which is at all-time high.

So at these prices, Nalco seems to offer decent Risk-Reward for long-term bets on Aluminium. The current book value is close to Rs.55 and of a EV of 11,500 Cr it is backed by about 9700 Cr in Plant and Machinery (7000 Cr) and Bank Balance of 2700 Cr so downside should be limited.

Trade war is definitely a real risk but its yet to play out while the price is already perhaps reflecting the worst outcomes. Another thing which is a big risk is input costs - i.e price of energy, be it crude or electricity. This could put a spanner in the works if Crude heads higher than $80.

6 Likes

hi @yourraj can you please highlight the parameters that are important to consider in a cement play.

Had invested in a couple of them without knowing where the cement cycle was.

Disclaimer : Invested in KCP, Kesoram

Which tool did you use for comparison that is seen in your screenshot? Looks good.

Cement is in a near term correction. I think one can build a good basket over the next 1 year. Just make sure, you don’t buy all from same market. As geographical spread is important. Cement is a very regional market.

4 Likes

@jitenp Could you please provide your view on textile sector ?

I use simple excel after featching the ratios from the screener I haven’t use any tool but I thing Kumar Saurabh has developed a the tool by which you can compare the 5 companies you can find it below

1 Like

Hi dear @hitesh Bhai has very clearly defined the strategy regarding cement cycle play @ CYCLICALS-- When and Where to Bet?

Mostly southern Indian has lots of cement industry north eastern side there are less geographic locations plays a great role that’s why Amrit culcutta based small company is starting its operation in north east side even Shree cement has started building capacity focusing on Northeast India . Latest mergers among cements industries will give them pricing power in their territory of operations. In Feb there were news that ACC will merge with Ambuja but that is called off … at last One must closely watch the sectoral news … and new infrastructure schemes will create a huge opportunity… residential and commercial cements has different curing time e.g. They are of high strength but low marginal some companies has started giving end to end solution they are providing redimixs which is higher value margin product …

5 Likes

@jitenp Congrats Jiten on featuring in ET .

Your Cyclical know how and thoughts imparted are most valuable.

15 Likes

Both the Integrated ferro chrome players are facing issues including Fines for excess mining, Agitation, etc.

The prices have corrected significantly. In your view is it worth taking position at these levels or better to wait for clarity.

regards

Disc: Not invested yet.

1 Like

I think lot of negatives are built into the price.

Another commodity upcycle being played out

https://forum.valuepickr.com/t/sterlite-technologies-digital-india-play/3473/115a

Number wise FerroChrome companies look very attractive, but I want to know about its supply side information, as you have mentioned in your interviews that, supply side tracking is very important in commodities. What all sources can I use to find the supply side information. What will be the triggers for FeCr upmove.

As I see currently pressure is from both the sides, cost wise coke and electricity, and international prices of FeCr were low, though the benchmark price have improved for this quarter.

This question is specifically for FerroChromes and commodity in general for educational purpose.

Disclosure: Small positions in two FerroChrome companies

is maithan alloy one of them?

Indsil Hydro has Ferro Allyos.

JSPL Records Domestic Steel Production of 1.23 Million Tonnes in Q1 FY2019

Achieves 46% y-o-y growth in Steel Sales and 36% y-o-y growth in Steel Production

Highest Ever First Quarter Domestic Steel Production

Highest Ever Monthly Pellet Production at JSPL’s 9 MTPA Pellet Plant at Barbil

1 Like

A question to @jitenp and all other cyclical veterans here.

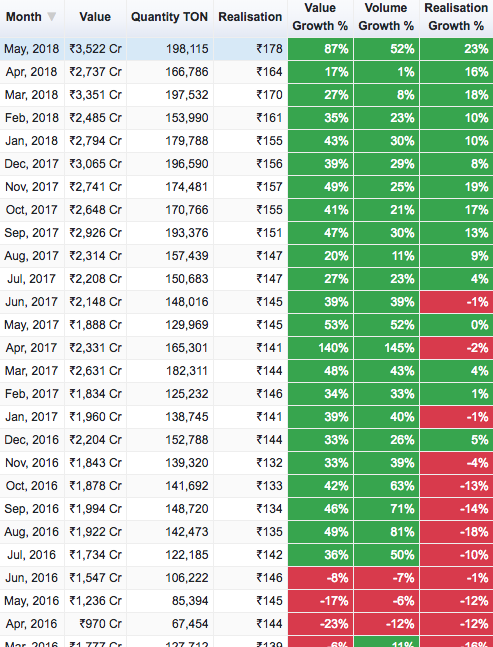

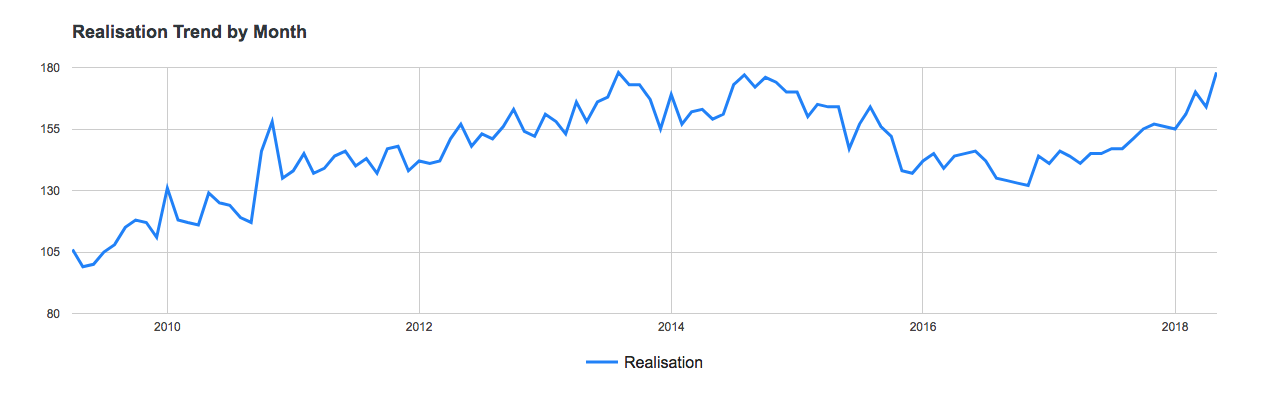

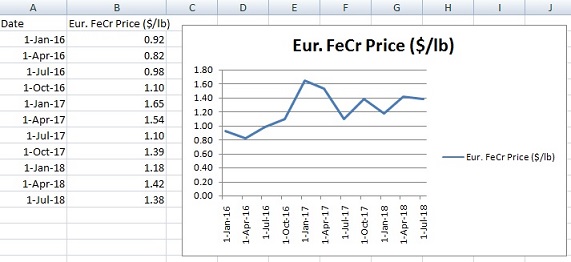

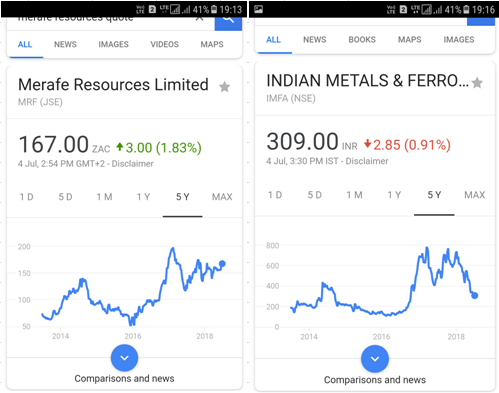

Ferrochrome prices are in a cyclical uptrend (chart attached) and moreover, discount in long term contacts over European Benchmark Ferrochrome price has settled at 10-15% over 30-35% earlier (Source:MetalBulletin.com).

Globally Ferrochrome plays have already crossed their October 2017 highs. Rupee has depreciated and South African Rand has appreciated which may be considered positive for these export oriented plays. Local unrest was also in just one player and not an industry issue.

So, the million dollar question is what is the reason for this divergence? What does the market know and pricing it in that I don’t know or can’t understand?

5 Likes